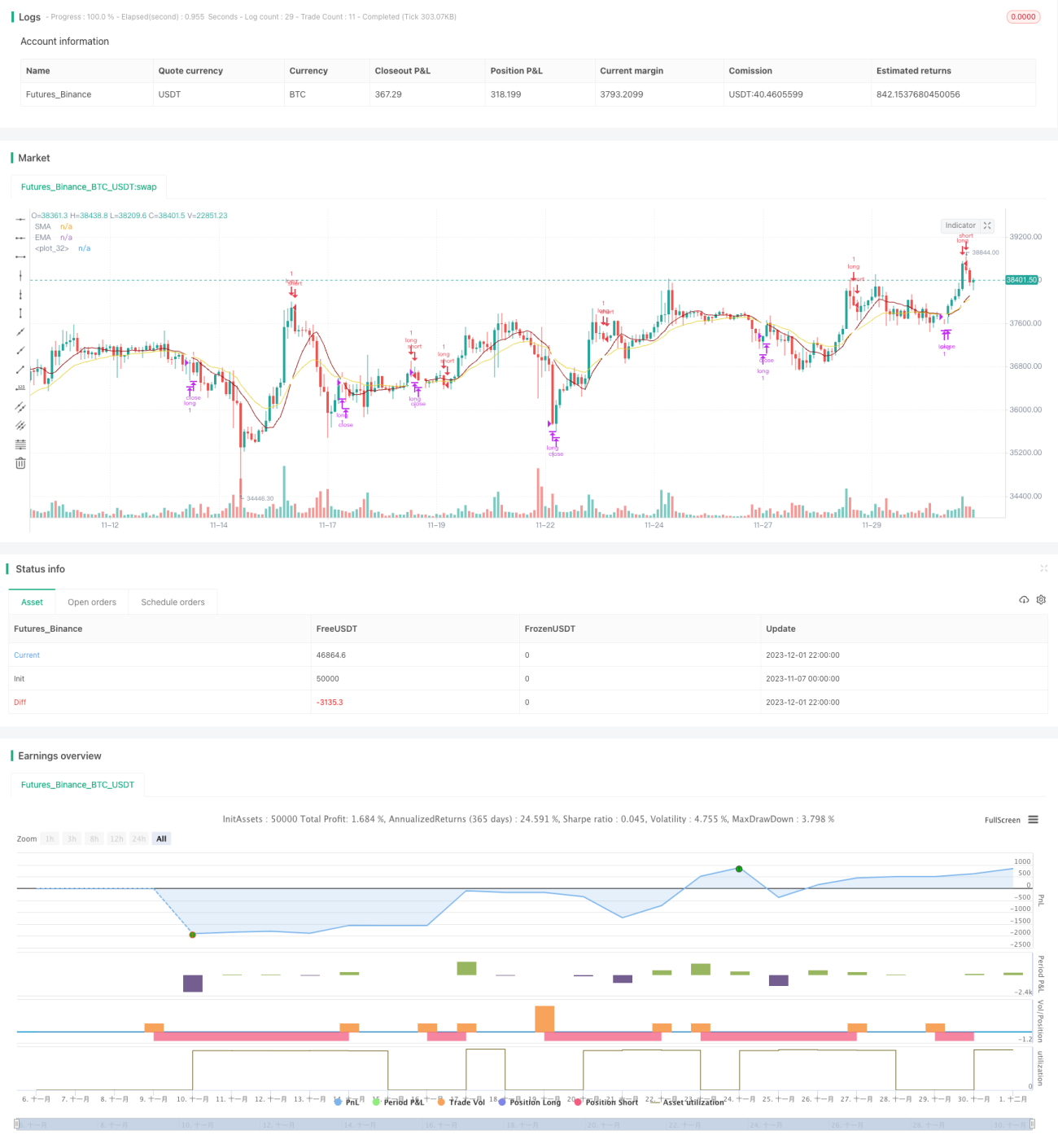

Простая импульсная стратегия на основе SMA, EMA и объема торгов

Обзор

Данная стратегия представляет собой простую внутридневную импульсную стратегию, ориентированную только на длинные позиции (без коротких). Она использует индикаторы SMA, EMA и объем, чтобы попытаться войти в рынок в оптимальный момент (когда цена и импульс одновременно растут). Ее преимущество — простота реализации и определенная способность распознавать тренды.

Принцип стратегии

Логика генерации сигнала Entry в этой стратегии следующая: одновременно выполняется условие, когда индикатор SMA выше EMA, и формируется восходящий тренд на протяжении 3 или 4 последовательных свечей, причем минимальная цена промежуточных свечей выше цены открытия начальной растущей свечи. В этом случае генерируется сигнал Entry.

Логика генерации сигнала Exit: сигнал Exit возникает, когда SMA пересекает EMA сверху вниз.

Стратегия работает только по длинным позициям, без коротких. Ее логика входа и выхода обладает определенной способностью распознавать устойчивые восходящие тренды.

Анализ преимуществ

Стратегия имеет следующие преимущества:

- Простая логика, легко понять и реализовать;

- Использует распространенные технические индикаторы, такие как SMA, EMA и объем, с гибкой настройкой параметров;

- Обладает определенной способностью распознавать устойчивые восходящие тренды, позволяя улавливать часть возможностей в рамках тренда.

Анализ рисков

Стратегия также несет следующие риски:

- Неспособность распознать нисходящий или боковой рынок, что может привести к значительным просадкам;

- Невозможность использовать короткие позиции и хеджировать снижающиеся тренды, что может привести к упущению выгодных возможностей;

- Индикатор объема может быть неэффективен для высокочастотных данных, требуется настройка параметров;

- Для контроля риска можно использовать стоп-лосс.

Направления оптимизации

Стратегию можно улучшить в следующих аспектах:

- Добавить возможности для коротких сделок, реализовав двустороннюю торговлю для использования спадов;

- Использовать более продвинутые индикаторы, такие как MACD, RSI, комбинируя стратегии для повышения точности определения тренда;

- Оптимизировать логику стоп-лосса для снижения риска просадок;

- Настроить параметры, протестировать данные на разных периодах для поиска оптимального набора параметров.

Заключение

В целом, данная стратегия представляет собой очень простую стратегию следования за трендом, которая использует индикаторы SMA, EMA и объем для определения моментов входа. Ее преимущество — простота и легкость реализации, что подходит для начального обучения. Однако она неспособна распознавать боковые и нисходящие тренды, что несет определенные риски. Улучшения могут быть достигнуты за счет введения коротких позиций, оптимизации индикаторов и стоп-лосса.

- 1