Стратегия отката импульса

Обзор

Стратегия импульсного отката (Momentum Pullback Strategy) — это стратегия длинных и коротких позиций, которая использует экстремальные значения RSI в качестве сигнала импульса. В отличие от большинства стратегий RSI, данная стратегия ищет первый откат в направлении экстремального показания RSI для входа.

Она открывает длинную/короткую позицию на первом откате к 5-дневной EMA (минимум цены) / 5-дневной EMA (максимум цены) и закрывает её на максимуме/минимуме за последние 12 свечей. Механизм скользящего максимума/минимума означает, что если цена входит в длительную консолидацию, цель по прибыли снижается с появлением каждой новой свечи. Лучшие сделки обычно завершаются в течение 2–6 свечей.

Рекомендуемый стоп-лосс составляет X множителей ATR от цены входа (настраивается в параметрах ввода пользователя).

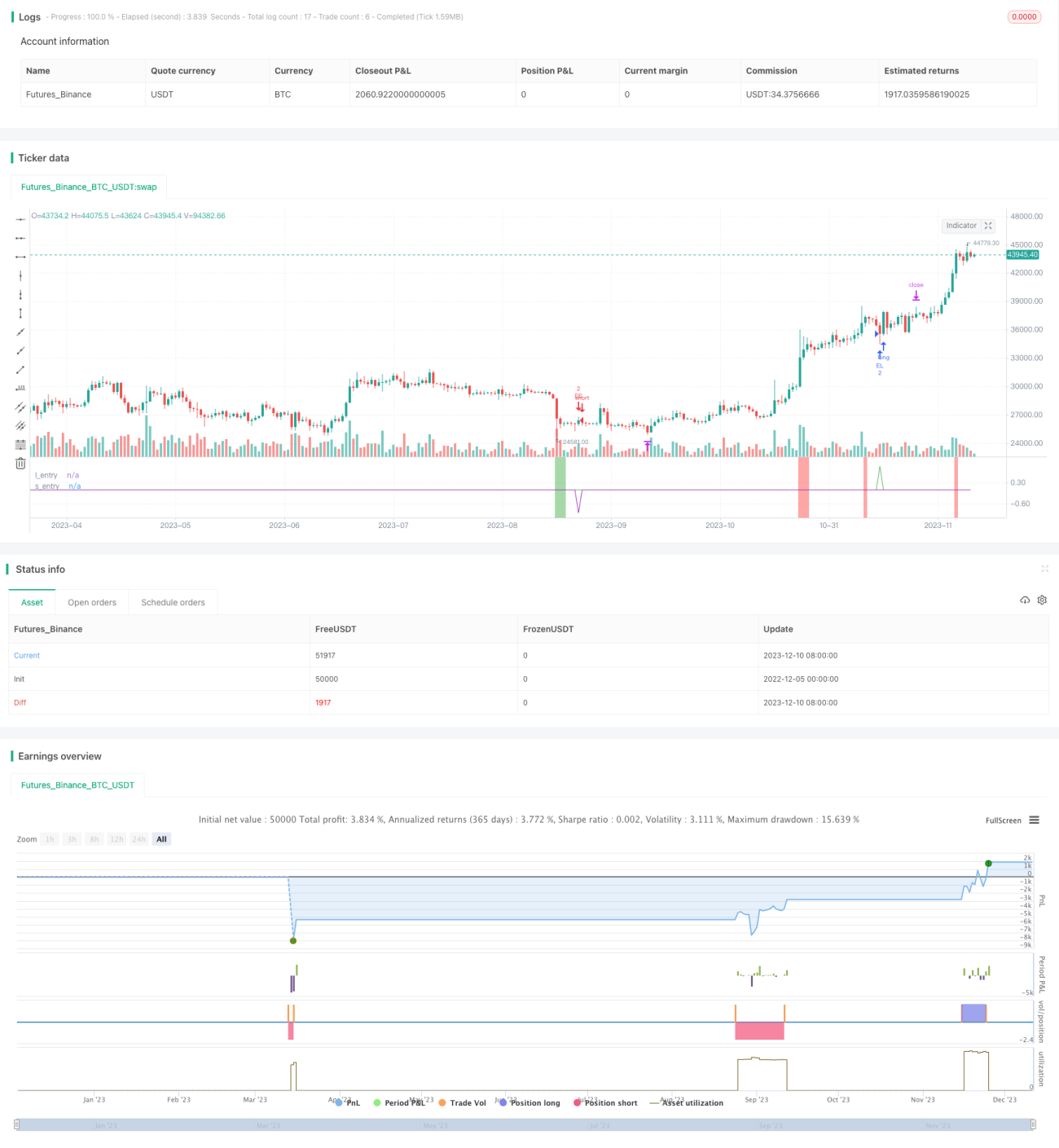

Стратегия демонстрирует хорошую устойчивость на различных таймфреймах и рынках, уровень выигрышей составляет 60%–70%, а размер прибыльных сделок значителен. Следует избегать сигналов, возникающих во время волатильности, вызванной важными экономическими новостями.

Принцип стратегии

-

Рассчитать 6-дневное значение RSI, искать экстремальные точки выше 90 (перекупленность) и ниже 10 (перепроданность).

-

Когда RSI перекуплен, в течение 6 свечей происходит откат к 5-дневной EMA (линия минимума) для входа в длинную позицию.

-

Когда RSI перепродан, в течение 6 свечей происходит откат к 5-дневной EMA (линия максимума) для входа в короткую позицию.

-

Выход осуществляется по скользящему тейк-профиту: для длинных позиций первая цель — максимум за последние 12 свечей, затем, с появлением новых свечей, цель обновляется до нового максимума за 12 свечей, что обеспечивает скользящий выход. Для коротких позиций наоборот — используется скользящий минимум за 12 свечей.

-

Расстояние до стоп-лосса составляет цену входа, умноженную на X множителей ATR, настраивается пользователем.

Анализ преимуществ

Стратегия сочетает экстремальные значения RSI как сигнал импульса и вход на откате, что позволяет улавливать потенциальные точки разворота в тренде с высоким процентом выигрышей.

Используется механизм скользящего тейк-профита, позволяющий фиксировать часть прибыли по мере фактического движения цены, уменьшая просадки.

Стоп-лосс на основе ATR эффективно ограничивает убытки по каждой сделке.

Высокая устойчивость: стратегия применима на разных рынках и с разными комбинациями параметров, легко воспроизводится в реальной торговле.

Анализ рисков

Если значение ATR установлено слишком большим, стоп-лосс может оказаться слишком далеко, увеличивая убыток по одной сделке.

Если происходит ██╗盘整理 (боковая консолидация), механизм скользящего тейк-профита сокращает пространство для прибыли.

Если откат происходит слишком глубоко и превышает 6 свечей, может быть упущен момент входа.

При значительных экономических событиях возможны проскальзывания или ложные пробои.

Направления оптимизации

Можно протестировать сокращение количества свечей для входа, например с 6 до 4, чтобы повысить процент успешных входов.

Можно увеличить множитель ATR для более строгого контроля стоп-лосса по каждой сделке.

Можно добавить индикатор объёма, чтобы избежать потерь при дивергенции в консолидации.

Можно входить после пробоя отката через среднюю линию 60-минутного таймфрейма, что отфильтрует часть шума.

Заключение

В целом стратегия импульсного отката — очень практичная краткосрочная ловчая стратегия. Она сочетает в себе тренд, разворот и стоп-лосс, что позволяет легко применять её в реальной торговле и при этом обладает определённой альфой. Путём настройки параметров и добавления других индикаторов можно ещё больше повысить стабильность. В итоге это большое подспорье для количественной торговли, которое стоит изучить и применять.

- 1