Гибридная стратегия количественной торговли с двойными индикаторами

Обзор

Данная стратегия определяет направление тренда и совершает сделки, комбинируя два набора индикаторов. Во-первых, она использует пересечение двух скользящих средних (быстрой и средней) для оценки краткосрочного тренда. Во-вторых, она использует диапазон канала и долгосрочную скользящую среднюю для определения основного направления тренда. Торговый сигнал генерируется только тогда, когда оба набора оценок совпадают. Такое смешанное использование нескольких индикаторов позволяет эффективно отфильтровывать ложные сигналы и повышать стабильность.

Принцип стратегии

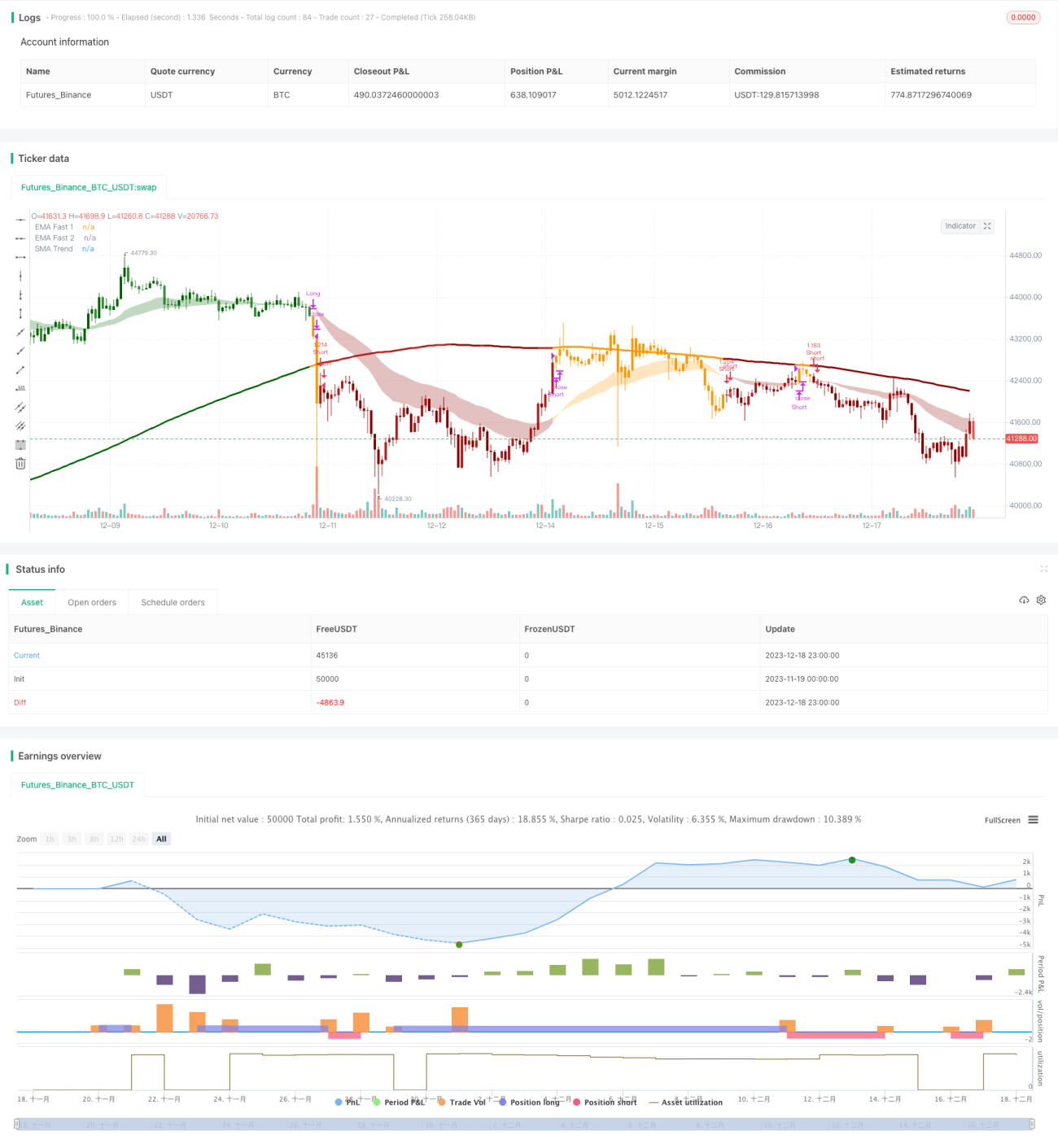

Стратегия использует три группы индикаторов для оценки. Во-первых, пересечение быстрой EMA (26 периодов) и средней EMA (50 периодов) — «золотое пересечение» (бычье) и «смертельное пересечение» (медвежье) — определяет краткосрочный тренд. Во-вторых, рассчитывается диапазон канала: если цена выходит за его пределы, это указывает на среднесрочное направление (бычье или медвежье). В-третьих, вычисляется долгосрочная SMA (200 периодов) и сравнивается с ценой для определения основного тренда. Сигнал к сделке подаётся только если все три оценки совпадают.

Конкретная логика оценки:

- Пересечение быстрой и средней скользящих средних (золотое пересечение — бычий сигнал, смертельное — медвежий) определяет краткосрочное направление.

- Выход цены за границы канала определяет среднесрочное направление. Диапазон канала строится как долгосрочная скользящая средняя плюс/минус ATR, умноженный на коэффициент. Если цена пробивает верхнюю границу — бычий сигнал, если нижнюю — медвежий.

- Сравнение цены и долгосрочной скользящей средней определяет основное направление тренда.

В итоге сигнал генерируется, только когда все три оценки (краткосрочная, среднесрочная, долгосрочная) совпадают. Такая комбинированная оценка эффективно отсеивает ложные сигналы и повышает стабильность.

Преимущества стратегии

Стратегия с двойными индикаторами имеет несколько преимуществ:

- Эффективное отсеивание ложных сигналов и повышенная стабильность. Поскольку для открытия сделки требуется подтверждение от нескольких индикаторов разного временного горизонта, это позволяет избежать ошибок одного индикатора.

- Высокая гибкость — параметры индикаторов (быстрые и медленные скользящие средние, параметры канала) можно настраивать под разные рыночные условия.

- Сочетание трендовой и диапазонной торговли. Кратко- и среднесрочные индикаторы ловят тренд, долгосрочные определяют диапазон — стратегия объединяет преимущества как следования за трендом, так и разворота.

- Высокая эффективность использования капитала — сделки открываются только при совпадении всех оценок, что позволяет избегать излишних операций и эффективно использовать средства.

Риски стратегии

Стратегия также сопряжена с некоторыми рисками:

- Риск настройки параметров. Периоды скользящих средних и параметры канала должны быть выбраны корректно; при неправильной настройке стратегия может не выявлять тренды или генерировать слишком много ложных сигналов.

- Двойные индикаторы увеличивают альтернативные издержки. По сравнению со стратегией на одном индикаторе, могут быть упущены некоторые торговые возможности, и вход/выход может происходить не в самых выгодных точках.

- Стоп-лосс требует осторожного подхода. Механизм пробоя в данной стратегии может приводить к неоправданным потерям, поэтому процент стопа должен быть тщательно подобран.

- Стратегия может быть менее эффективна на рынке с сильными флуктуациями и боковым движением. Она лучше подходит для явно выраженных трендовых рынков.

Направления оптимизации

Стратегия может быть улучшена в следующих аспектах:

- Тестирование различных комбинаций параметров для поиска оптимальных. Анализ на более широком объёме исторических данных позволит выбрать наилучшие настройки.

- Добавление адаптивного механизма стоп-лосса. Можно использовать индикатор волатильности (например, ATR) для динамической корректировки уровня стопа.

- Включение индикаторов объёма для вспомогательной оценки. На ключевых точках они помогут определить размер позиции и повысить эффективность использования капитала.

- Оптимизация логики входа. Рассмотреть стратегию усреднения цены при входе (cost-averaging), чтобы снизить риски одной сделки.

- Комбинация с моделями машинного обучения. Внедрение нейронных сетей или других моделей для оценки надёжности и качества подгонки.

Заключение

Данная стратегия, используя тройную оценку (кратко-, средне- и долгосрочную) и механизм двойного подтверждения, позволяет эффективно подавлять ложные сигналы и повышать стабильность. Одновременно она сочетает преимущества трендовой и диапазонной торговли, обеспечивая высокую эффективность использования капитала. Стратегия может быть улучшена путём оптимизации параметров, настройки стоп-лосса, добавления индикаторов объёма и т.д., что делает её перспективной гибридной количественной стратегией.

- 1