Двухиндикаторная количественная стратегия

Обзор

Эта стратегия генерирует торговые сигналы путем комбинирования индикатора разворота 123 и индикатора RAVI. Индикатор 123 является стратегией разворота, использующей движение цены акции в течение двух последовательных дней для прогнозирования будущего движения цены. Индикатор RAVI определяет, входит ли цена в зону перекупленности или перепроданности. Стратегия принимает решение о покупке или продаже на основе комплексной оценки сигналов обоих индикаторов.

Принцип стратегии

Разворот 123

Этот индикатор основан на значении %K стохастика. Конкретно: если текущая цена закрытия ниже, чем два дня назад, и 9-периодная медленная стохастическая линия ниже 50, то открывается длинная позиция. Если текущая цена закрытия выше, чем два дня назад, и 9-периодная быстрая стохастическая линия выше 50, то открывается короткая позиция. Таким образом, точка входа подтверждается через разворот.

Индикатор RAVI

Этот индикатор использует расхождение быстрой и медленной скользящих средних для определения покупки/продажи. А именно, расхождение между 7-дневной скользящей средней и 65-дневной скользящей средней. Когда оно превышает определенный параметр, открывается длинная позиция; когда ниже определенного параметра — короткая. Пересечение быстрой и медленной линий используется для определения зон перекупленности/перепроданности.

Сигналы стратегии

Сигнал генерируется, когда индикатор 123 и RAVI дают однонаправленные сигналы на покупку или продажу. Сигнал на покупку возникает, когда оба индикатора равны 1, сигнал на продажу — когда оба равны -1. Таким образом, двойное подтверждение позволяет избежать ложных сигналов одного индикатора.

Преимущества

- Комбинирование двух индикаторов повышает точность сигналов, избегая ложных.

- 123 использует информацию свечей, RAVI — скользящих средних, что позволяет оценивать рынок с разных углов.

- Параметры RAVI настраиваемы, возможна оптимизация под различные инструменты и рыночные условия.

- Разворот плюс тренд позволяет ловить как развороты, так и следовать тренду.

Риски и оптимизация

- Комбинация двух индикаторов может приводить к несовпадению сигналов. Можно рассмотреть использование параметров спреда, при котором сигнал генерируется также при расхождении индикаторов в определенном диапазоне.

- 123 — высокочастотная стратегия, требует комбинирования с другими низкочастотными стратегиями для снижения частоты торговли.

- RAVI хорошо ловит среднесрочные/долгосрочные тренды, комбинация с краткосрочным индикатором повышает устойчивость стратегии к рискам.

Заключение

Стратегия комплексно учитывает факторы разворота и тренда, использует двойное подтверждение индикаторов для уменьшения вероятности ложных сигналов. На следующем этапе можно внедрить алгоритмы машинного обучения для адаптивной оптимизации параметров. Или рассмотреть формирование портфеля стратегий, объединив с другими типами стратегий для сохранения доходности при снижении максимальной просадки.

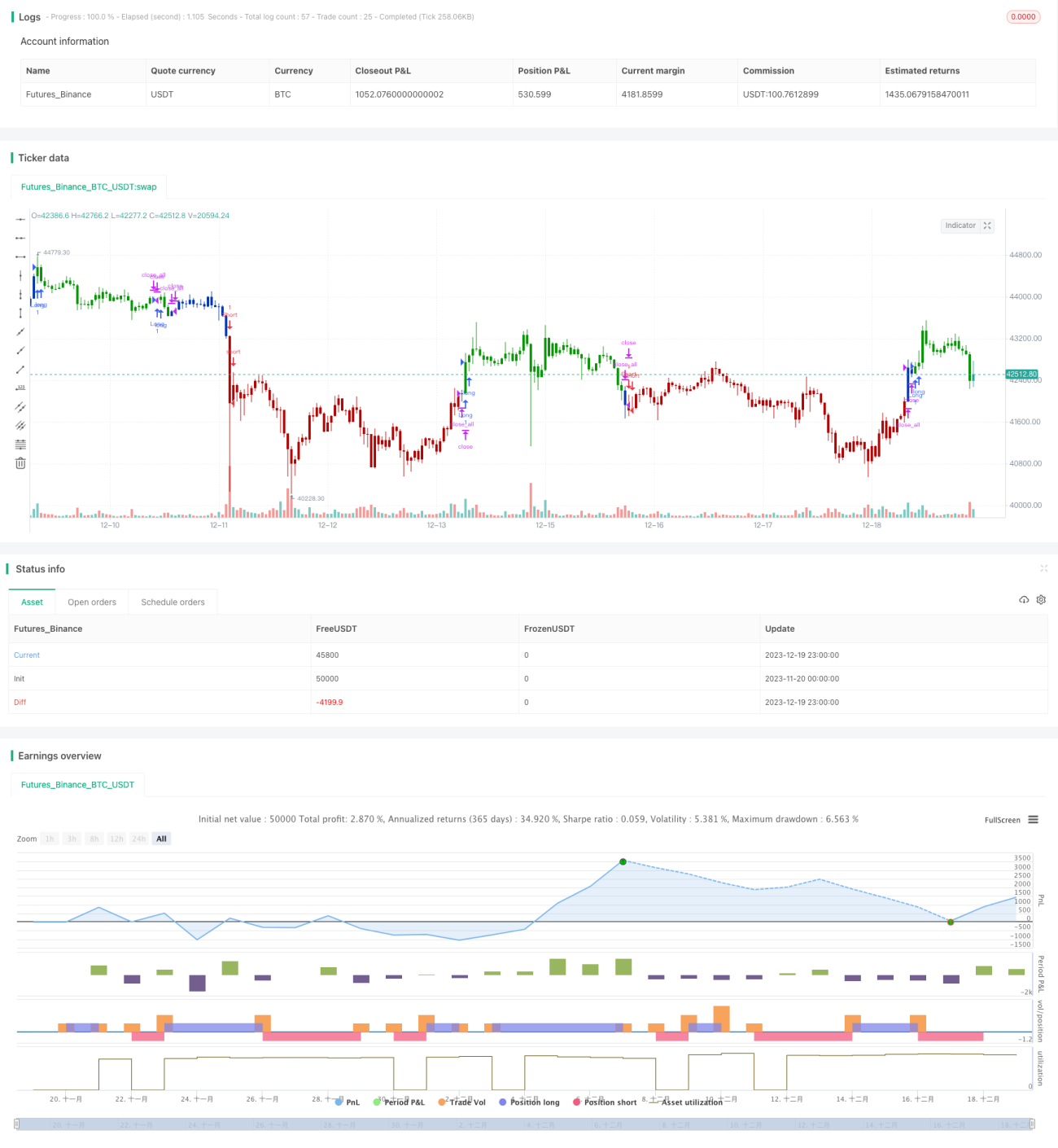

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 31/05/2021

// This is combo strategies for get a cumulative signal. - 1