Стратегия отката при золотом пересечении EMA

Обзор

Стратегия отката после золотого креста EMA — это количественная торговая стратегия на основе индикатора EMA. В данной стратегии используются три линии EMA с различными периодами для формирования торговых сигналов, а также механизм ценового отката для установки стоп-лосса и тейк-профита, что позволяет реализовать автоматическую торговлю.

Принцип стратегии

В стратегии используются три линии EMA:

- EMA1: используется для определения уровней поддержки/сопротивления при откате цены, имеет более короткий период, по умолчанию 33.

- EMA2: используется для фильтрации части ложных разворотных сигналов, период равен 5-кратному периоду EMA1, по умолчанию 165.

- EMA3: используется для определения общего направления тренда, период равен 11-кратному периоду EMA1, по умолчанию 365.

Генерация торговых сигналов следует следующей логике:

Длинный сигнал: цена пробивает EMA1 вверх, затем происходит откат, формируя более высокий минимум над EMA1, при этом величина отката не достигает EMA2. После выполнения условий открывается длинная позиция при повторном пробое EMA1 вверх.

Короткий сигнал: цена пробивает EMA1 вниз, затем происходит откат, формируя более низкий максимум под EMA1, при этом величина отката не достигает EMA2. После выполнения условий открывается короткая позиция при повторном пробое EMA1 вниз.

Стоп-лосс устанавливается на уровне минимальной/максимальной цены отката. Тейк-профит устанавливается как двукратный размер стоп-лосса.

Преимущества стратегии

Данная стратегия обладает следующими преимуществами:

- Использование индикатора EMA для формирования торговых сигналов обеспечивает относительно высокую надежность.

- Сочетание с механизмом ценового отката позволяет эффективно избежать попадания в ловушку.

- Стоп-лосс устанавливается на предыдущих максимумах/минимумах, что эффективно контролирует риск.

- Тейк-профит устанавливается в соответствии с соотношением стоп-лосса и тейк-профита, удовлетворяя требованиям соотношения прибыли и убытка.

- Возможность настройки параметров EMA в зависимости от рынка для адаптации к различным периодам.

Риски стратегии

Данная стратегия также имеет определенные риски:

- Индикатор EMA обладает запаздыванием, что может привести к пропуску точек разворота тренда.

- Слишком большой диапазон отката, превышающий EMA2, может генерировать ложные сигналы.

- В трендовом рынке стоп-лосс может быть пробит.

- Неправильная настройка параметров может привести к слишком частым сделкам или упущению возможностей.

Оптимизацию параметров можно проводить путем корректировки периодов EMA, ограничения диапазона отката и других методов. Также можно комбинировать с другими индикаторами для фильтрации сигналов.

Направления оптимизации

Стратегию также можно оптимизировать по следующим направлениям:

- Добавление трендовых индикаторов для избежания контртрендовой торговли. Например, добавление MACD.

- Добавление индикаторов объема для избежания ложных пробоев. Например, добавление OBV.

- Оптимизация параметров периодов EMA или использование адаптивных EMA.

- Применение методов машинного обучения, таких как мешок слов, для динамической оптимизации параметров.

- Добавление прогнозных моделей и настройка адаптивных стоп-лосса и тейк-профита.

Заключение

Стратегия отката после золотого креста EMA реализует автоматическую торговлю путем построения трехлинейной системы EMA в сочетании с характеристиками ценового отката для установки стоп-лосса и тейк-профита. Стратегия эффективно контролирует торговые риски и может быть оптимизирована путем настройки параметров в зависимости от рынка. В целом, логика стратегии разумна и применима на практике. В будущем возможна дальнейшая оптимизация в таких аспектах, как определение тренда, оптимизация параметров и управление рисками.

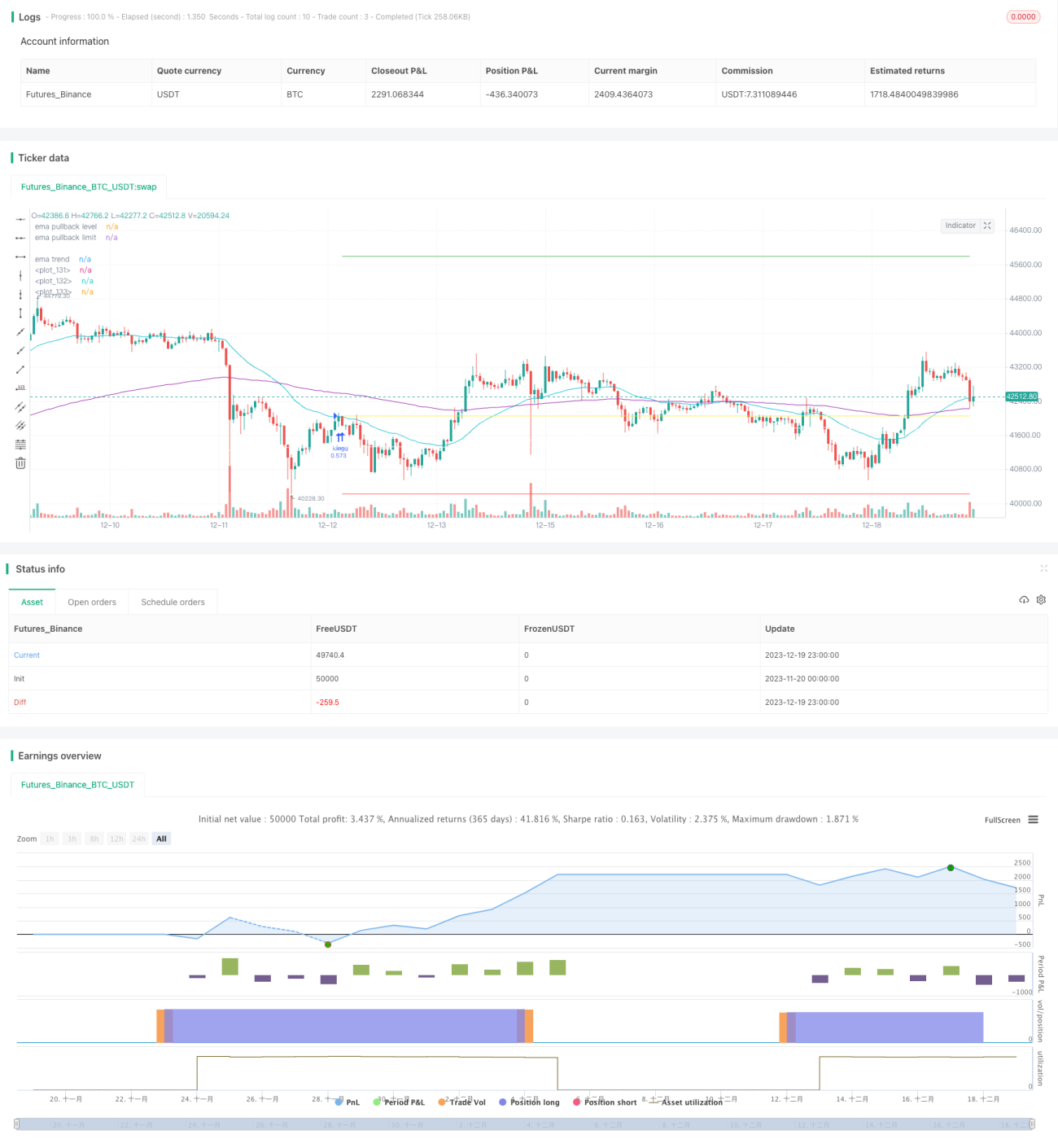

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// created by Space Jellyfish

//@version=4

- 1