Быстрая торговая стратегия с низкой задержкой на основе трёх скользящих средних

Принцип стратегии

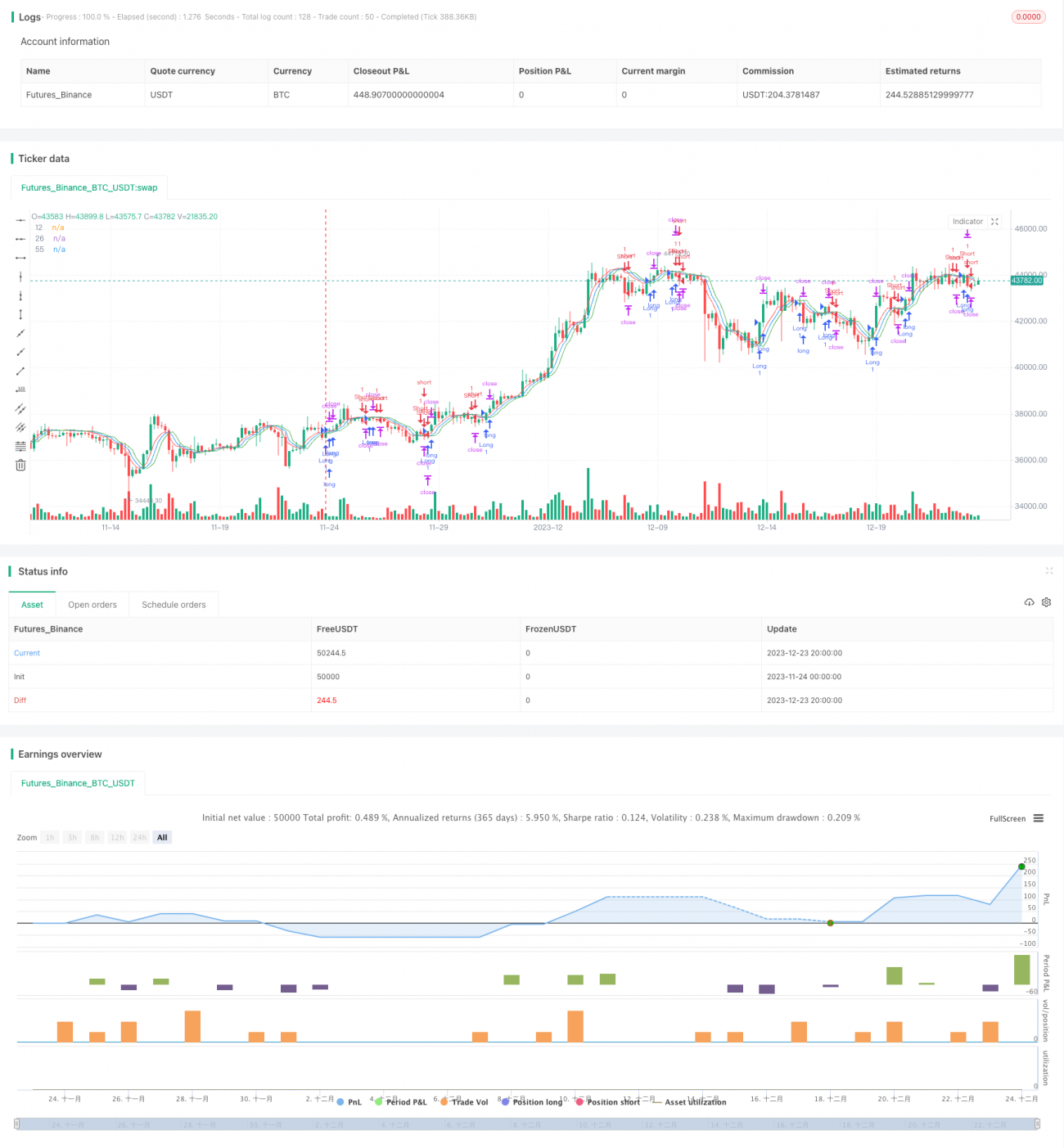

Данная стратегия использует три скользящие средние с низкой задержкой, включая 12-, 26- и 55-периодные TEMA с низкой задержкой. Эти три скользящие средние представляют: быструю, среднюю и медленную скользящие средние. Когда быстрая скользящая средняя пересекает среднюю снизу вверх, генерируется сигнал на покупку; когда быстрая скользящая средняя пересекает среднюю сверху вниз, генерируется сигнал на продажу. Таким образом, с помощью пересечения трёх скользящих средних определяются точки входа и выхода с рынка для реализации высокочастотной торговли.

В коде определена шаблонная функция tema() для расчёта TEMA с низкой задержкой. Формула расчёта: TEMA = 2*EMA - EMA(EMA), при этом используется двойная экспоненциальная скользящая средняя (EWMA). По сути, это дважды сглаженная экспоненциальная скользящая средняя, главное преимущество которой — значительное снижение запаздывания. Это позволяет быстрее реагировать на изменения цены и повышает своевременность определения торговых сигналов.

Конкретно, правила входа в позицию по данной стратегии: сигнал на покупку генерируется, когда быстрая скользящая средняя пересекает среднюю снизу вверх и находится выше медленной скользящей средней; сигнал на продажу генерируется, когда быстрая скользящая средняя пересекает среднюю сверху вниз и находится ниже медленной скользящей средней.

Анализ преимуществ

Главное преимущество данной стратегии — быстрое и точное определение моментов входа и выхода. Конструкция трёх скользящих средних с низкой задержкой значительно уменьшает запаздывание, позволяя быстро реагировать на изменения цены. Кроме того, использование пересечения трёх скользящих средних для определения сигналов позволяет избежать ложных срабатываний.

Также данная стратегия подходит для высокочастотной торговли, позволяя извлекать прибыль из краткосрочных колебаний цен. Благодаря быстрому входу и выходу, можно получать прибыль на рынках с высокой волатильностью.

Анализ рисков

Самый большой риск данной стратегии — возможность возникновения сверхкраткосрочных «ловушек». Конструкция трёх скользящих средних с низкой задержкой делает их чрезвычайно чувствительными к изменениям цены, что на некоторых рынках может приводить к высокочастотным колебаниям. В таких случаях легко попасть в ловушку.

Кроме того, высокочастотная торговля требует уплаты значительных комиссий и проскальзывания цены. Если прибыльность недостаточна, торговые издержки могут легко свести на нет доход.

Также данная стратегия предъявляет высокие требования к способности трейдера отслеживать ситуацию в реальном времени, необходимо своевременно обновлять уровни стоп-лосса и тейк-профита.

Направления оптимизации

Данную стратегию можно оптимизировать по следующим направлениям:

-

Оптимизировать периоды трёх скользящих средних для лучшей адаптации к особенностям различных рынков;

-

Добавить индикаторы волатильности или объёма для подтверждения сигналов, чтобы избежать попадания в ловушки во время флэтовых движений;

-

Интегрировать больше факторов для установки механизма стоп-лосса и тейк-профита с динамическим отслеживанием;

-

Оптимизировать управление размером позиции, контролируя риск отдельной сделки с помощью методов управления капиталом;

-

Внедрить алгоритмы машинного обучения для динамической оптимизации параметров стратегии.

Заключение

Данная стратегия представляет собой быструю торговую стратегию на основе трёх скользящих средних с низкой задержкой. Благодаря низкому запаздыванию она обеспечивает быстрый вход и выход, что делает её подходящей для высокочастотной торговли и захвата краткосрочных возможностей. Главное преимущество — быстрое и точное определение сигналов, главный недостаток — подверженность попаданию в ловушки при флэтовых движениях. В данной статье подробно описывается стратегия: принцип действия, анализ преимуществ, анализ рисков и пути оптимизации.

Заключение

Это быстрая торговая стратегия на основе тройной скользящей средней с низким запаздыванием. Благодаря низколаговой конструкции она позволяет осуществлять быстрые входы и выходы, что подходит для высокочастотной торговли для захвата краткосрочных возможностей. Главное преимущество данной стратегии – быстрое и точное определение сигналов. Основной недостаток – высокая подверженность ложным сигналам (whipsaw) на боковых рынках. В данной статье представлен всесторонний обзор этой торговой стратегии на основе детального анализа её принципов, преимуществ, рисков и направлений оптимизации.

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("scalping low lag tema etal", shorttitle="Scalping tema",initial_capital=10000, overlay=true)

mav = input(title="Moving Average Type", defval="temadelay", options=["nkclose", "ema", "emadelay", "fastema", "tema", "temadelay"])

lenb = 3- 1