Торговая стратегия Bitcoin на основе количественных индикаторов

Обзор

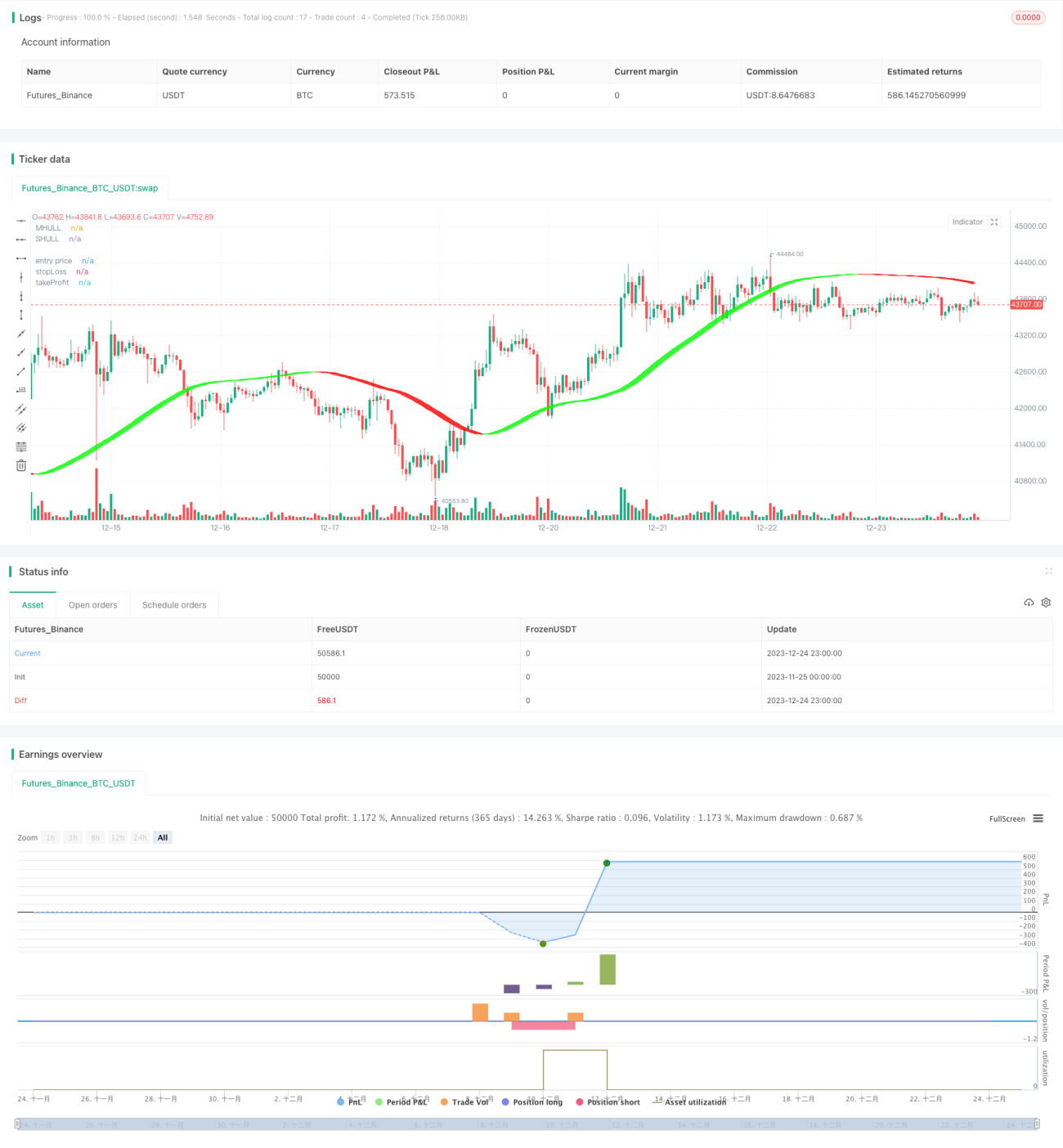

Данная стратегия использует несколько количественных индикаторов для определения моментов покупки и продажи биткоина, обеспечивая автоматизированную торговлю. Включает индикатор Халла (Hull), относительную силу (RSI), полосы Боллинджера (BB) и осциллятор объема (VO).

Принцип стратегии

-

Используется модифицированная скользящая средняя Халла для определения основного тренда рынка в сочетании с полосами Боллинджера для вспомогательного определения точек пробоя для покупки/продажи.

-

Индикатор RSI в сочетании с адаптивным диапазоном волатильности определяет зоны перекупленности/перепроданности, генерируя торговые сигналы. При этом установлены две группы параметров для верификации сигналов-дубликатов.

-

Осциллятор объема оценивает силу покупок/продаж, помогая избежать ложных пробоев.

-

Используются параметры соотношения стоп-лосс/тейк-профит для предустановки уровней стоп-лосса и тейк-профита, обеспечивая управление рисками.

Преимущества

-

Кривая Халла быстрее улавливает смену тренда, а полосы Боллинджера помогают уменьшить ложные сигналы.

-

Оптимизация параметров RSI и верификация дублирующими сигналами повышают надежность.

-

Осциллятор объема в сочетании с трендовыми и индикаторными сигналами предотвращает неточные сделки.

-

Предустановленные стоп-лосс и тейк-профит позволяют автоматически контролировать убытки/прибыль по каждой сделке, эффективно управляя общим риском.

Анализ рисков

-

Неправильная настройка параметров может привести к чрезмерной частоте сделок или ухудшению качества сигналов.

-

При резких рыночных движениях из-за неожиданных событий стоп-лосс может быть пробит, что приведет к значительным потерям.

-

При смене торгового инструмента на другую криптовалюту необходимо заново тестировать и оптимизировать параметры.

-

При отсутствии данных об объеме осциллятор объема становится неработоспособным.

Направления оптимизации

-

Провести больше комбинаций тестов параметров RSI для поиска оптимальных значений.

-

Попробовать комбинировать с другими индикаторами, такими как MACD, KD и т.д., для повышения точности сигналов.

-

Добавить модуль прогнозирования на основе моделей машинного обучения для определения рыночного направления.

-

Протестировать эффективность параметров при смене торгового инструмента.

-

Оптимизировать алгоритмы стоп-лосса и тейк-профита для максимизации прибыли.

Заключение

Данная стратегия комплексно использует несколько количественных технических индикаторов для определения моментов покупки/продажи. Благодаря оптимизации параметров, управлению рисками и другим методам, реализована автоматизированная торговля биткоином. Стратегия показывает хорошие результаты, однако требует постоянного тестирования и оптимизации для адаптации к рыночным изменениям. Может служить ориентиром для инвесторов, помогая в принятии торговых решений.

- 1