Количественная торговая стратегия, сочетающая тренд и колебания

Обзор

Стратегия двойного трендового осциллятора — это количественная торговая стратегия, сочетающая в себе трендовый и осцилляторный подходы. Она использует комбинацию двух индикаторов для определения направления и силы тренда, а также ищет благоприятные точки входа во время колебаний рынка.

Принцип стратегии

Стратегия основана на двух публичных индикаторах: Trend Surfers и Mawreez's Trend Oscillator.

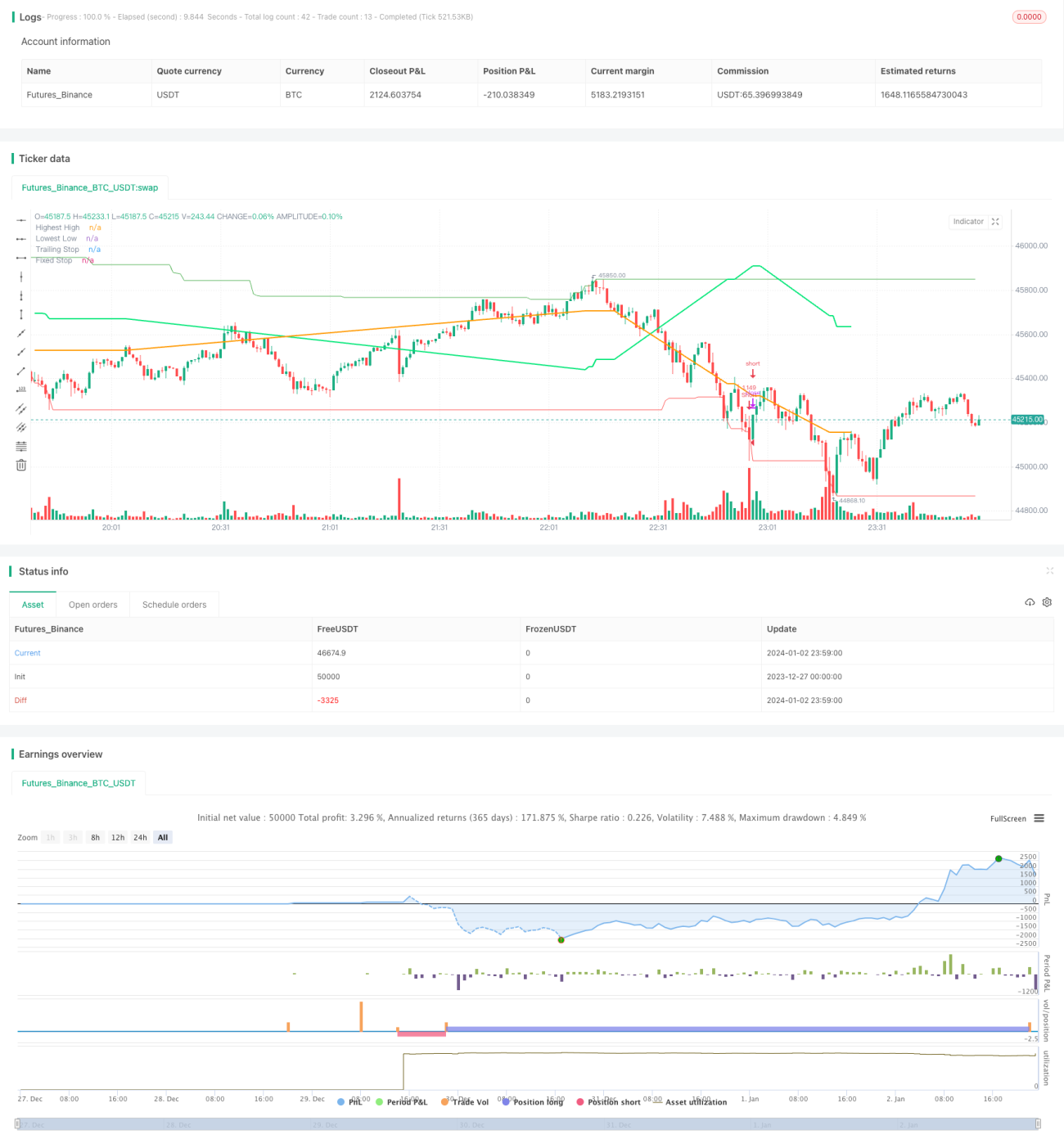

Trend Surfers — это трендовый стоп-лосс индикатор. Он рассчитывает максимумы и минимумы за определённый период, чтобы определить направление цены и предложить уровни стоп-лосса. Например, когда цена пробивает максимум за последние 168 баров, это бычий сигнал; когда цена пробивает минимум за последние 168 баров, это медвежий сигнал.

Mawreez's Trend Oscillator — это двухлинейный осциллятор, напоминающий MACD. Он использует разницу DI для оценки направления и силы тренда. Когда линия индикатора выше нулевой линии — тренд бычий, ниже — медвежий.

Правила входа по стратегии:

- Вход в длинную позицию: когда Trend Surfers пробивает верхнюю линию, а Mawreez's Trend Oscillator показывает бычий сигнал.

- Вход в короткую позицию: когда Trend Surfers пробивает нижнюю линию, а Mawreez's Trend Oscillator показывает медвежий сигнал.

Стоп-лосс представляет собой комбинацию трейлинг-стопа и фиксированного стопа.

Преимущества

Стратегия объединяет трендовые и осцилляторные индикаторы, что позволяет как ловить тренд, так и находить лучшие цены входа в боковике. Преимущества:

- Двойная фильтрация сигналов позволяет эффективно избегать ложных пробоев.

- Сочетание тренда и осциллятора облегчает поиск точек накопления на низких уровнях (или лёгкого выхода на высоких) в диапазонном движении.

- Многоуровневый стоп-лосс хорошо контролирует риски.

Анализ рисков

Стратегия также содержит некоторые риски:

- Комбинация двух индикаторов может привести к пропуску сигналов.

- Трендовый и осцилляторный индикаторы могут давать противоречивые сигналы.

- Фиксированный стоп-лосс может срабатывать слишком рано.

Для снижения этих рисков можно предпринять следующие меры:

- Несколько ослабить параметры индикаторов, снизив фильтрацию.

- Добавить дополнительные правила определения тренда, чтобы избежать конфликтов сигналов.

- Динамически корректировать уровни стоп-лосса.

Направления оптимизации

Стратегия имеет потенциал для дальнейшего улучшения:

- Тестировать различные комбинации параметров и таймфреймов для поиска оптимальных значений.

- Добавить вспомогательные правила, такие как волатильность, объём торгов и т.д.

- Применить методы машинного обучения для динамической оптимизации индикаторов и параметров.

Заключение

Стратегия двойного трендового осциллятора комплексно использует преимущества трендовых и осцилляторных инструментов, позволяя как определять направление тренда, так и использовать возможности боковика. Путём оптимизации параметров и правил можно дополнительно повысить доходность стратегии. Данная стратегия имеет хорошие перспективы для развития.

- 1