Стратегия следования за трендом на основе скользящих средних SSL

Обзор

Данная стратегия использует индикатор канала SSL для определения направления рыночного тренда и следует за трендом на основе скользящей средней. Она подходит для среднесрочных и долгосрочных 4-часовых и дневных графиков.

Принципы стратегии

-

Канал SSL состоит из скользящей средней Келтнера и истинного диапазона (ATR). Он позволяет определить направление рыночного тренда. Пробой цены выше верхней границы является бычьим сигналом, пробой ниже нижней границы – медвежьим сигналом.

-

Стратегия использует скользящие средние, такие как EMA, для расчета базовой скользящей средней. Эта линия помогает отфильтровать часть ложных пробоев.

-

Стратегия открывает длинную позицию при пробое цены вверх через верхнюю границу SSL и короткую позицию при пробое вниз через нижнюю границу SSL. В восходящем тренде она следует за ростом и продаёт при падении, в нисходящем – пытается поймать дно, покупая на падении.

-

Способы стоп-лосса: процентный стоп-лосс, стоп-лосс на основе ATR и стоп-лосс по последним минимумам/максимумам. Тейк-профит задаётся как N-кратная величина стоп-лосса. Конкретные параметры определяются пользователем.

Анализ преимуществ

-

Канал SSL точно определяет направление тренда, снижая количество ложных сигналов. Комбинация со скользящей средней в качестве основы для входа в рынок позволяет избегать покупок на вершинах и продаж на минимумах.

-

Гибкий выбор различных типов скользящих средних позволяет адаптироваться к широкому спектру рыночных условий.

-

Разнообразные способы установки стоп-лосса обеспечивают контроль над риском. Коэффициент тейк-профита также можно гибко настраивать в соответствии с разными предпочтениями.

-

Возможность одновременного открытия как длинных, так и коротких позиций позволяет в полной мере использовать двусторонние возможности рынка.

Анализ рисков

-

Индикаторы скользящих средних обладают запаздыванием, что может привести к накоплению убытков.

-

В условиях бокового тренда после пробоя верхней или нижней границы может произойти разворот, что приведёт к попаданию в ловушку.

-

Стоп-лоссы на основе ATR и по последним минимумам/максимумам могут оказаться слишком широкими при экстремальных пробоях, что увеличивает убытки.

Меры по снижению рисков:

- Соответствующая настройка параметров скользящей средней или выбор другого её типа.

- Увеличение размера стоп-лосса и своевременное закрытие убыточных позиций.

- Добавление множителя к ATR или корректировка периода ретроспективного анализа.

Направления оптимизации

- Тестирование большего числа типов скользящих средних для нахождения оптимальных параметров.

- Оптимизация параметра периода ATR для стоп-лосса.

- Тестирование различных значений множителя стоп-лосса.

- Тестирование различных коэффициентов риска для тейк-профита.

Заключение

Данная стратегия комплексно использует канал SSL для определения тренда и скользящие средние для подтверждения входа в рынок, что позволяет эффективно следовать за трендом. Она предлагает гибкие способы установки стоп-лосса и тейк-профита, обеспечивая получение более высокой доходности при контроле рисков. Путем постоянного тестирования и оптимизации параметров можно добиться лучших торговых результатов. Это эффективная стратегия, заслуживающая долгосрочного отслеживания и практического применения.

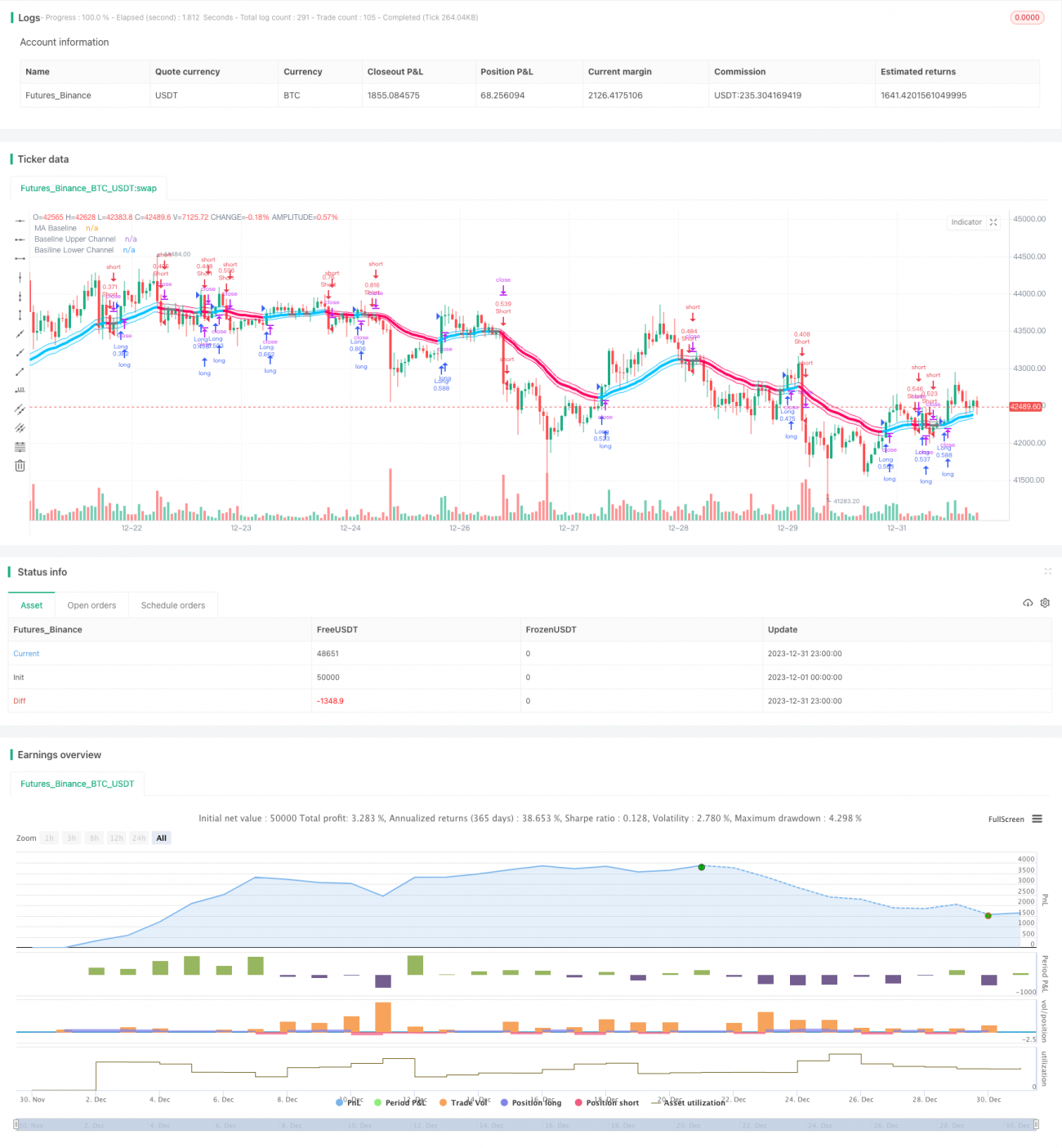

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1