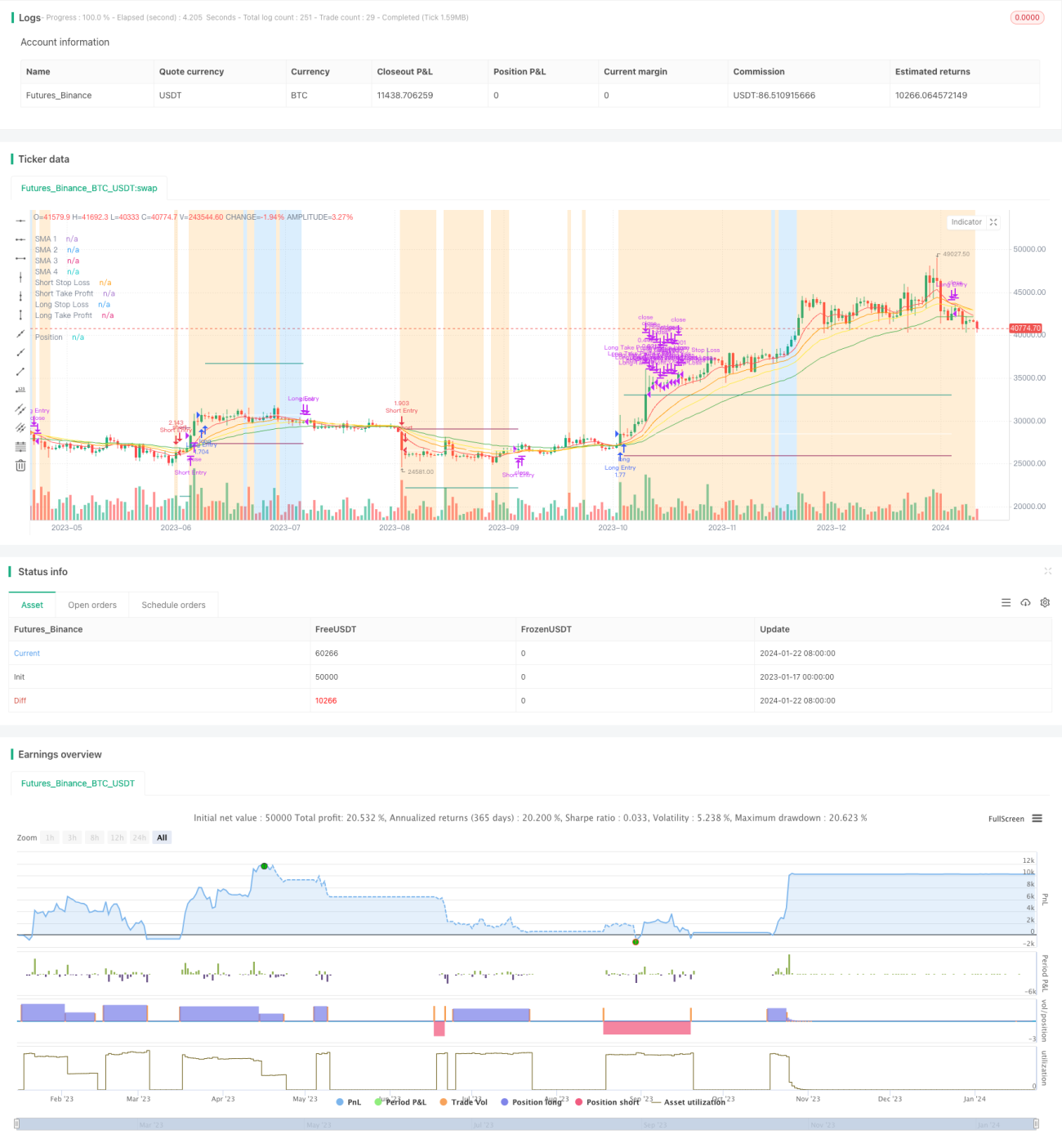

Стратегия следования за трендом на основе скользящих средних

Обзор

Данная стратегия представляет собой простую стратегию следования за трендом на основе скользящих средних. Она сравнивает значения скользящих средних с разными периодами для определения текущего направления тренда и его продолжительности. Когда краткосрочная скользящая средняя пересекает долгосрочную снизу вверх, открывается длинная позиция; когда краткосрочная скользящая средняя пересекает долгосрочную сверху вниз, открывается короткая позиция. Кроме того, в стратегии предусмотрены стоп-лосс и тейк-профит для контроля риска.

Принцип стратегии

В стратегии используются 4 скользящие средние с разными периодами: 5-дневная, 10-дневная, 15-дневная и 25-дневная. Эти четыре скользящие средние обозначаются как MA1, MA2, MA3 и MA4. MA1 – самая короткая, MA4 – самая длинная.

Когда MA1 > MA2 > MA3 > MA4, это указывает на восходящий тренд, открывается длинная позиция. Когда MA1 < MA2 < MA3 < MA4, это указывает на нисходящий тренд, открывается короткая позиция.

Условия открытия длинной и короткой позиций также должны удовлетворять фильтру ATR-стопа, а именно значение ATR должно быть больше 40-периодного простого скользящего среднего ATR. Это позволяет избежать ложных сигналов при слишком малых колебаниях цены.

Преимущества стратегии

Стратегия имеет следующие преимущества:

- Простая и понятная логика, легко реализуется.

- Использование нескольких групп скользящих средних для определения направления тренда является надежным.

- Установка тейк-профита и стоп-лосса позволяет эффективно контролировать максимальные потери по каждой сделке.

- Фильтр ATR-стопа позволяет избежать ложных сигналов при слишком малых колебаниях цены.

Анализ рисков

Стратегия также имеет следующие риски:

- На сильно колеблющемся рынке могут возникать ложные сигналы.

- Неправильная настройка параметров (периоды скользящих средних и т.д.) может привести к низкой эффективности стратегии.

- Не учитывается влияние фундаментальных факторов и важных новостей на цену.

Для снижения этих рисков можно оптимизировать параметры или добавить дополнительные фильтры для повышения стабильности стратегии.

Направления оптимизации

Направления оптимизации данной стратегии:

- Тестирование различных комбинаций периодов скользящих средних для поиска оптимальных параметров.

- Добавление фильтров по другим техническим индикаторам, таким как MACD, KDJ и т.д., для оценки надежности сигналов.

- Добавление фильтра по объему торгов – совершать сделки только при увеличении объема.

- Проведение детальной оптимизации параметров для каждого инструмента с учетом их различий.

- Внедрение алгоритмов машинного обучения для оценки сигналов.

Заключение

В целом данная стратегия представляет собой относительно простую стратегию следования за трендом. Она определяет направление тренда с помощью скользящих средних и устанавливает разумные уровни тейк-профита и стоп-лосса для контроля риска. Стратегия имеет большой потенциал для оптимизации: настройка параметров, добавление фильтров и другие меры могут еще больше повысить ее стабильность и прибыльность.

- 1