Дневная стратегия на основе скользящей средней и индикатора Вильямса

Обзор

Данная стратегия сочетает использование скользящих средних, индикатора ATR и индикатора Вильямса для торговли на дневном таймфрейме по валютной паре GBP/JPY. Сначала стратегия определяет ценовой тренд и возможные точки разворота с помощью скользящей средней, затем использует индикатор Вильямса для дополнительного подтверждения торгового сигнала, а с помощью ATR рассчитывает уровни стоп-лосса и объём сделки.

Принцип стратегии

- Используется 20-периодная скользящая средняя (базовая линия) для определения общего ценового тренда: пробой цены снизу вверх сигнализирует о покупке, пробой сверху вниз — о продаже.

- Индикатор Вильямса используется для подтверждения разворота цены. Пробой вверх уровня -35 является подтверждением покупки, пробой вниз уровня -70 — подтверждением продажи.

- ATR рассчитывает средний диапазон колебаний за последние 2 дня. Значение умножается на коэффициент и устанавливается как расстояние до стоп-лосса.

- Контроль риска осуществляется на уровне 50% от капитала счёта. Объём сделки рассчитывается исходя из расстояния до стоп-лосса и доли риска.

- При входе в длинную позицию стоп-лосс устанавливается на уровне минимума цены минус расстояние стопа. Тейк-профит — точка входа плюс 100 пунктов. Логика выхода используется для дополнительного подтверждения сигнала выхода.

- При входе в короткую позицию стоп-лосс и тейк-профит устанавливаются аналогично. Логика выхода используется для дополнительного подтверждения сигнала выхода.

Преимущества анализа

- Совместное использование скользящей средней для определения тренда и индикаторов для подтверждения входа позволяет эффективно отфильтровывать убытки от ложных пробоев.

- Динамический стоп-лосс на основе ATR позволяет устанавливать разумное расстояние до стопа в зависимости от волатильности рынка.

- Контроль риска и расчёт динамического объёма сделки позволяют максимально ограничить убыток по одной сделке.

- Логика выхода в сочетании со скользящей средней позволяет точнее определить момент выхода, избегая преждевременного фиксирования прибыли.

Анализ рисков

- Сигналы от скользящей средней могут быть ошибочными с высокой вероятностью, поэтому требуется дополнительное подтверждение от индикаторов.

- Сами индикаторы также могут генерировать ложные сигналы, полностью избежать убытков невозможно.

- Стратегия лучше подходит для трендовых инструментов и может быть менее эффективна на диапазонных рынках.

- Неправильная настройка коэффициентов контроля риска также может повлиять на доходность стратегии.

Оптимизация возможна за счёт изменения периода скользящей средней, добавления большего числа индикаторов или ручного вмешательства в торговлю.

Заключение

Данная стратегия сочетает определение тренда и фильтрацию с помощью индикаторов, разработана для дневной торговли GBP/JPY. Она использует динамический стоп-лосс, контроль риска и другие методы управления рисками. Потенциал для улучшения велик: можно корректировать параметры и комбинировать методы для повышения эффективности стратегии.

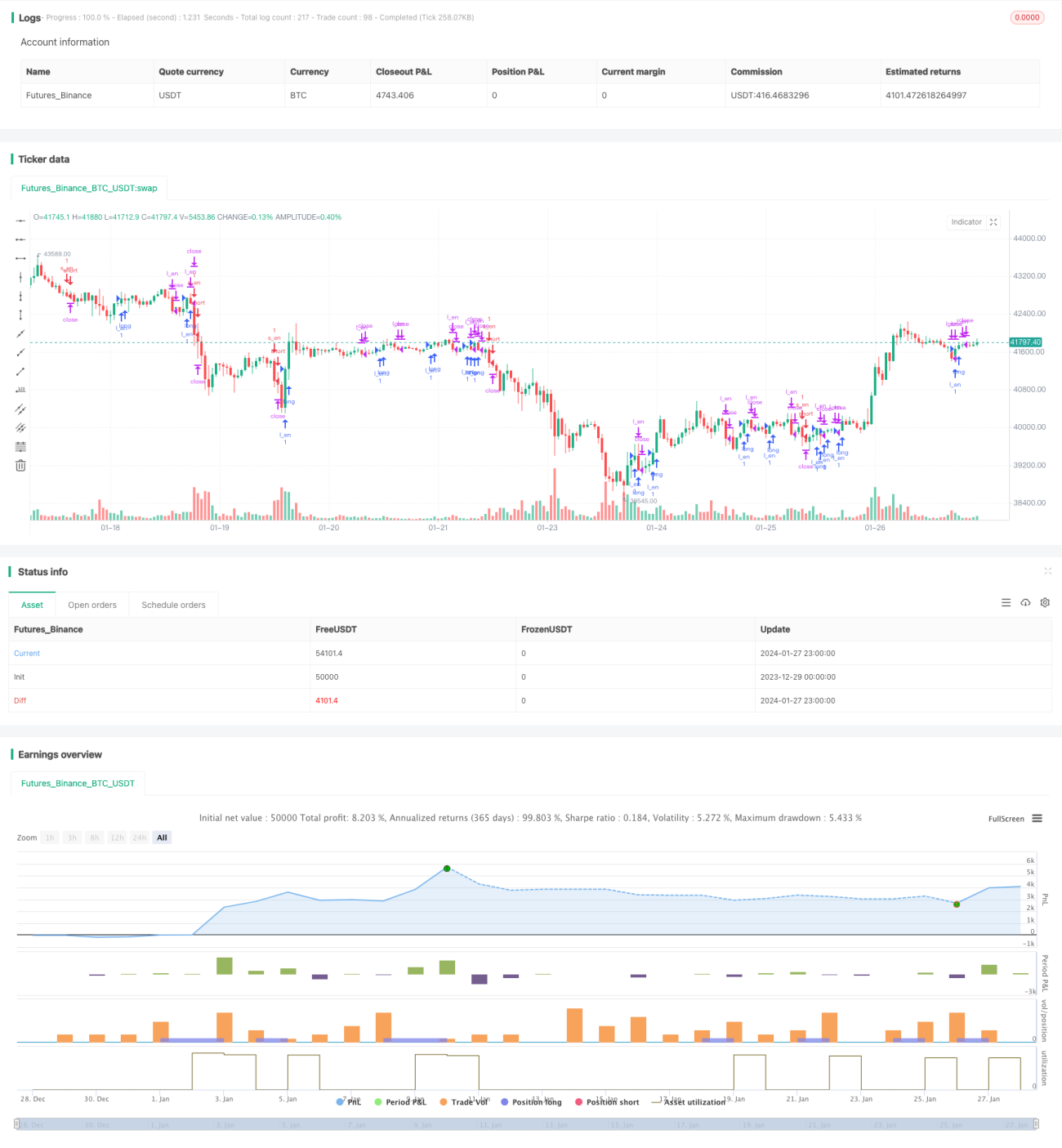

/*backtest

start: 2023-12-29 00:00:00

end: 2024-01-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("GBPJPY DAILY FX",initial_capital = 1000,currency="USD", overlay=true)

UseHAcandles = input(false, title="Use Heikin Ashi Candles in Algo Calculations")- 1