Стратегия с двумя скользящими средними на основе теории Чань

Обзор

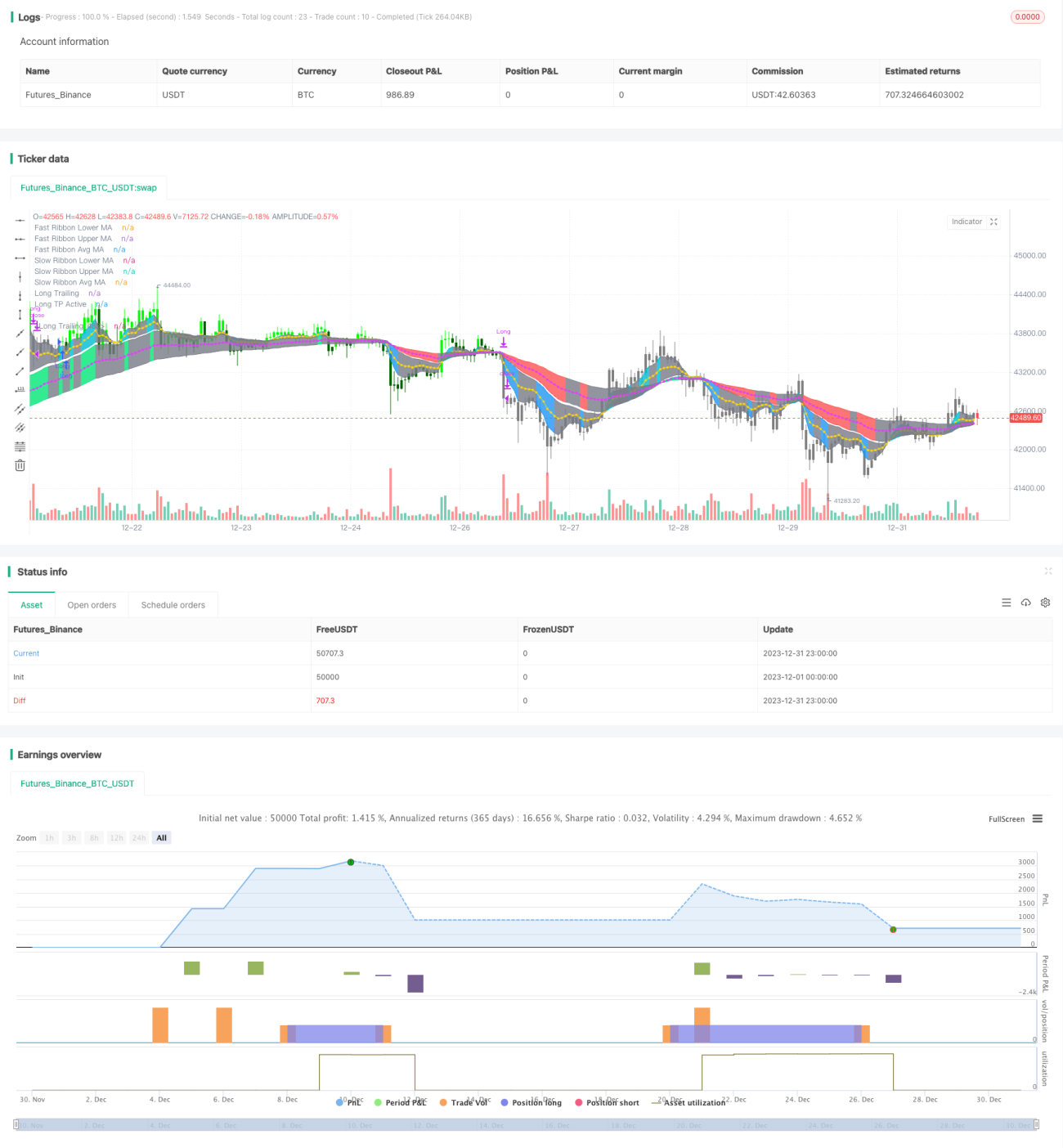

Стратегия «Двойная скользящая средняя по теории Чань» (Double Moving Average Chan Theory) — это стратегия следования за трендом. Она вычисляет две группы скользящих средних, формируя быструю и медленную линии, и определяет направление тренда на основе соотношения цены и скользящих средних.

Когда быстрая линия пересекает медленную снизу вверх — это сигнал к покупке. Когда быстрая линия пересекает медленную сверху вниз — сигнал к продаже. Данная стратегия использует направление быстрых и медленных скользящих средних, количество свечей пробития цены и другие условия для определения конкретных моментов входа и выхода.

Принцип стратегии

Стратегия «Двойная скользящая средняя по теории Чань» вычисляет две группы скользящих средних, представляющих критерии оценки краткосрочного и долгосрочного тренда. В частности, в стратегии определены:

- Быстрая группа скользящих средних, включающая быструю нижнюю полосу и быструю верхнюю полосу, представляющие краткосрочный тренд.

- Медленная группа скользящих средних, включающая медленную нижнюю полосу и медленную верхнюю полосу, представляющие долгосрочный тренд.

Стратегия использует ценовое соотношение между быстрой и медленной группами скользящих средних для оценки обоснованности краткосрочного и долгосрочного трендов, а также конкретных моментов входа и выхода.

Условия входа следующие:

- Когда быстрая верхняя полоса пробивает медленную верхнюю полосу вверх на 2 свечи или более — вход в длинную позицию.

- Когда быстрая нижняя полоса пробивает медленную нижнюю полосу вниз на 2 свечи или более — вход в короткую позицию.

Условия выхода следующие:

- Во время удержания длинной позиции — выход из длинной позиции, когда быстрая скользящая средняя пересекает медленную сверху вниз.

- Во время удержания короткой позиции — выход из короткой позиции, когда быстрая скользящая средняя пересекает медленную снизу вверх.

Кроме того, в стратегии предусмотрены функции тейк-профита, стоп-лосса и трейлинг-стопа для контроля рисков.

Анализ преимуществ

Основные преимущества стратегии «Двойная скользящая средняя по теории Чань»:

- Использование двойных скользящих средних позволяет эффективно отфильтровывать рыночный шум и определять направление тренда.

- Комбинация быстрых и медленных скользящих средних с ценовыми соотношениями повышает надёжность сигналов.

- Правила стратегии просты и понятны, легко реализуются, подходят для алгоритмической торговли.

- Встроенные средства контроля риска, такие как тейк-профит, стоп-лосс и трейлинг-стоп, позволяют эффективно управлять торговыми рисками.

Анализ рисков

Стратегия «Двойная скользящая средняя по теории Чань» также имеет определённые риски, в основном:

- На боковом рынке могут возникать ложные сигналы, приводящие к ненужным сделкам.

- Система скользящих средних медленно реагирует на внезапные события (например, выход значительных негативных/позитивных новостей), что может привести к большим убыткам.

- Трейлинг-стоп может быть пробит при определённых рыночных условиях, увеличивая убытки.

Для контроля указанных рисков можно оптимизировать параметры скользящих средних или комбинировать с другими индикаторами для фильтрации.

Направления оптимизации

Стратегию «Двойная скользящая средняя по теории Чань» можно оптимизировать по следующим направлениям:

- Оптимизировать параметры скользящих средних, настроить периоды скользящих средних для адаптации к различным рыночным циклам.

- Добавить фильтры других индикаторов, сформировать комбинированную стратегию из нескольких индикаторов для повышения точности сигналов.

- Оптимизировать настройки стоп-лосса и тейк-профита, установить пороги просадки для контроля максимальных убытков.

- Внедрить модели машинного обучения для прогнозирования тренда, чтобы помочь определить момент входа.

Заключение

В целом, стратегия «Двойная скользящая средняя по теории Чань» является весьма практичной стратегией следования за трендом. Её правила принятия решений просты, логика ясна, риски контролируются с помощью системы двойных скользящих средних, теоретическая основа прочна. В дальнейшем её можно улучшать за счёт оптимизации параметров, управления рисками и других аспектов, чтобы повысить доходность и стабильность стратегии.

- 1