Межтаймфреймовая стратегия отслеживания моментума

Обзор

Данная стратегия реализует отслеживание импульса на нескольких таймфреймах путём комбинирования индикаторов «123 разворота» и MACD. «123 разворота» определяет точки краткосрочного разворота тренда, а MACD — средне- и долгосрочный тренд. Сочетание позволяет получать сигналы на покупку или продажу, фиксируя долгосрочный тренд при краткосрочном развороте.

Принцип стратегии

Стратегия состоит из двух частей:

-

Часть «123 разворота»: когда последние две свечи формируют более высокий максимум / более низкий минимум, а стохастический осциллятор находится ниже/выше 50, генерируется сигнал на покупку/продажу.

-

Часть MACD: когда быстрая линия пересекает медленную линию сверху вниз — сигнал на покупку, когда быстрая линия пересекает медленную снизу вверх — сигнал на продажу.

В итоге два сигнала объединяются: финальный сигнал подаётся, когда «123 разворота» и MACD одновременно дают однонаправленные сигналы.

Преимущества

Стратегия сочетает краткосрочный разворот и средне-/долгосрочный тренд, позволяя фиксировать долгосрочный тренд при краткосрочных колебаниях, что повышает процент выигрышных сделок. Особенно на боковом рынке можно отфильтровать часть шума с помощью «123 разворота», повысив стабильность.

Кроме того, настройка параметров позволяет сбалансировать соотношение сигналов разворота и тренда, адаптируясь к различным рыночным условиям.

Риски

Стратегия имеет некоторую временную задержку, особенно при использовании длинных периодов MACD, что может привести к упущению краткосрочных движений. Кроме того, сигналы разворота сами по себе содержат элемент случайности, что может привести к ложному входу.

Для контроля риска можно сократить период MACD или добавить стоп-лосс.

Направления оптимизации

Стратегию можно оптимизировать в следующих направлениях:

- Настройка параметров «123 разворота» для улучшения разворотных сигналов.

- Настройка параметров MACD для улучшения определения тренда.

- Добавление дополнительных фильтрующих индикаторов для повышения эффективности.

- Внедрение стратегии стоп-лосса для контроля рисков.

Заключение

Данная стратегия объединяет технические индикаторы с разными параметрами и таймфреймами, используя кросс-таймфреймовое отслеживание импульса для балансирования преимуществ разворотной и трендовой торговли. Эффект можно регулировать через настройку параметров, а также добавлять дополнительные индикаторы или стоп-лосс для оптимизации. Это многообещающая концепция стратегии.

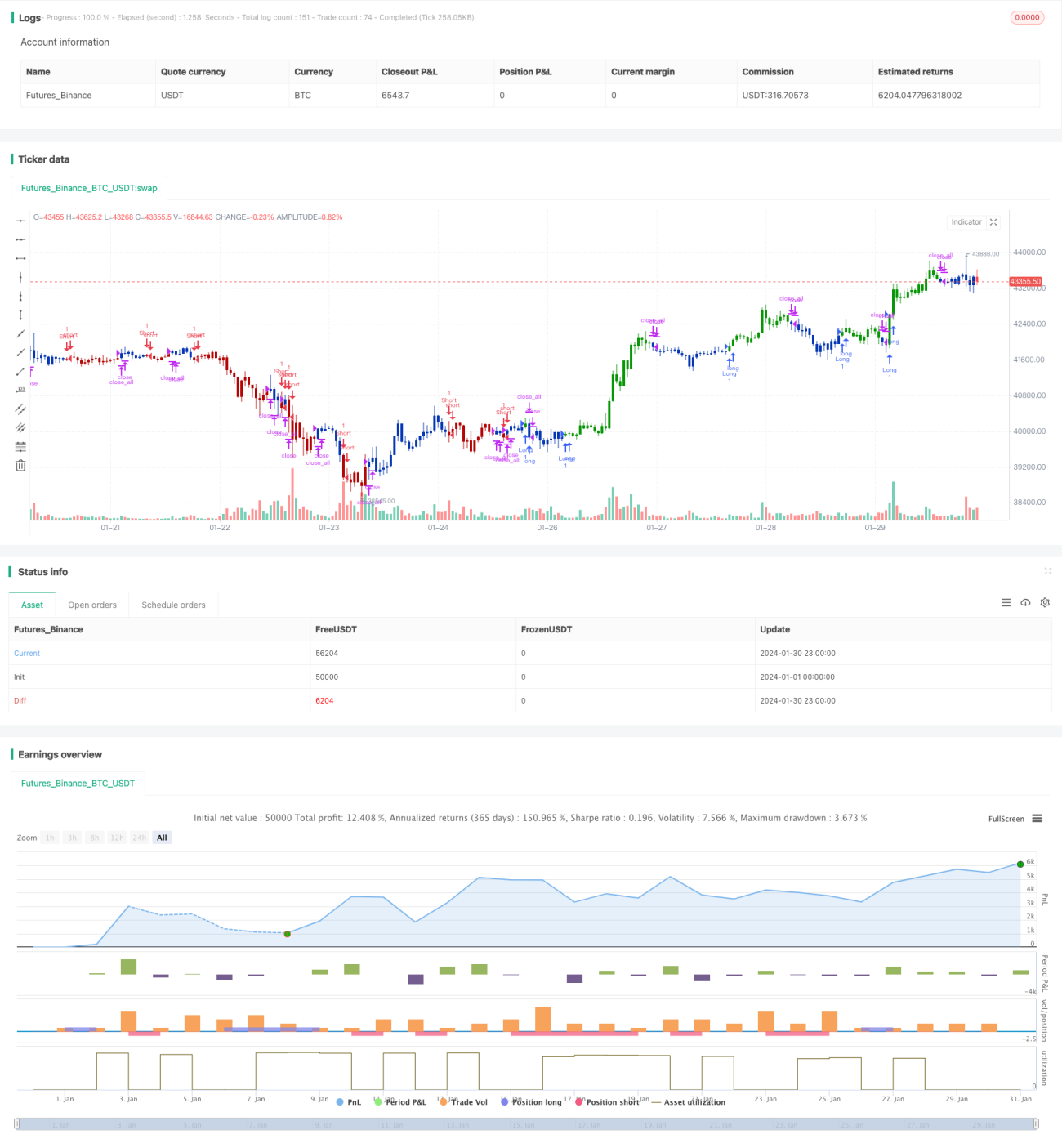

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1