Стратегия торговли на основе импульсного прорыва

Обзор

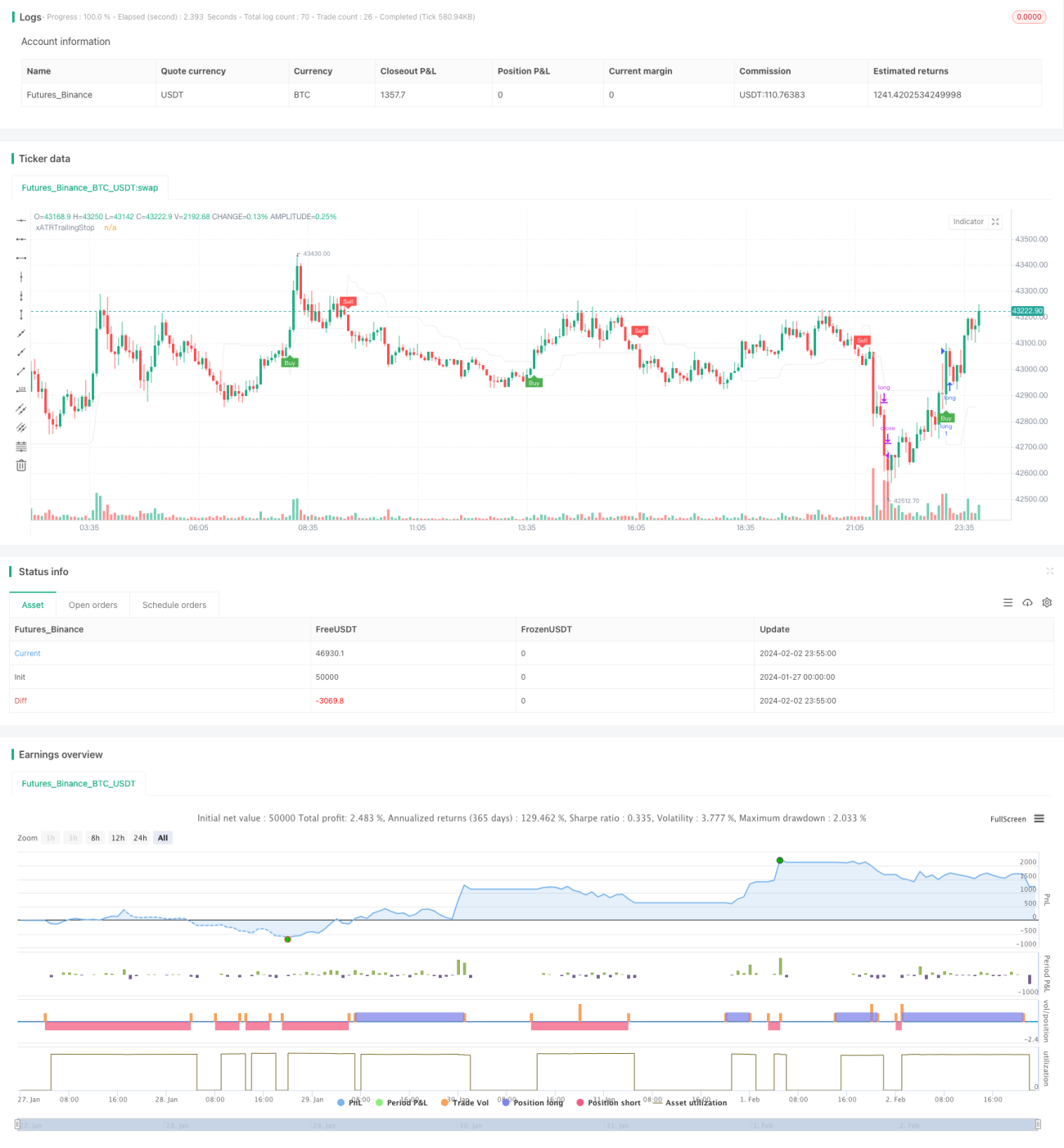

Данная стратегия представляет собой прорывную торговую стратегию, основанную на импульсных индикаторах. Она использует несколько индикаторов, таких как скользящие средние, ATR и RSI, для оценки рыночного тренда и волатильности, а также строгие правила стоп-лосса и тейк-профита для совершения сделок. Сигналы к торговле генерируются в основном при пробое ценой восходящего или нисходящего направления скользящей средней, дополненной диапазоном ATR.

Принципы стратегии

Стратегия основана на следующих ключевых моментах:

-

Использование EMA для определения направления тренда. Пробой цены вверх скользящей средней — бычий сигнал, вниз — медвежий.

-

Индикатор ATR помогает оценить рыночную волатильность. ATR, умноженный на коэффициент, задает диапазон стоп-лосса, что позволяет эффективно контролировать убыток по одной сделке.

-

Индикатор RSI определяет зоны перекупленности и перепроданности. Сделки по пробою на основе ATR и скользящей средней должны совершаться только при отсутствии условий перекупленности/перепроданности по RSI, что помогает избежать ложных пробоев.

-

В качестве ориентира для тейк-профита используются предыдущие максимумы или минимумы. Трейлинг-стоп для фиксации прибыли позволяет захватить больше прибыли.

-

Строгие правила стоп-лосса и тейк-профита. Стоп-лосс на основе ATR контролирует риск, а тейк-профит фиксирует прибыль.

Сигнал на вход возникает при пробое ценой уровня, равного скользящей средней плюс диапазон ATR (для бычьего сигнала цена должна пробить этот максимум; для медвежьего — минимальный уровень).

Анализ преимуществ

Стратегия обладает следующими преимуществами:

-

Использование нескольких индикаторов позволяет избежать ложных пробоев и повышает точность сигналов.

-

Установка стоп-лосса на основе ATR удерживает убытки на разумном уровне.

-

Динамический трейлинг-стоп позволяет максимизировать прибыль.

-

Жесткие правила стоп-лосса и тейк-профита способствуют контролю рисков.

-

Высокая степень гибкости в оптимизации индикаторов и параметров под различные рынки.

Анализ рисков

Стратегия также сопряжена со следующими рисками:

-

Доходность связана с рыночной волатильностью. При неясном тренде или длительном боковике потенциал прибыли ограничен.

-

Возможна ситуация, когда цена, отскочив от стоп-лосса, снова пробивает уровень. Это приводит к невозможности своевременно войти в сделку и следовать тренду. Можно немного ослабить стоп-лосс.

-

chasing.

Направления оптимизации

Данную стратегию можно оптимизировать по следующим направлениям:

-

Адаптация параметров скользящих средних, ATR и т.д. под различные инструменты и таймфреймы.

-

Внедрение дополнительных индикаторов, таких как MACD, KDJ для оценки перекупленности/перепроданности.

-

Корректировка коэффициента стоп-лосса в реальном времени на основе текущего значения ATR, чтобы стоп-лосс лучше соответствовал волатильности.

-

Создание комбинаций из нескольких таймфреймов. Совокупность сигналов с разных периодов повышает качество сигналов.

-

Применение методов машинного обучения для тестирования и оптимизации индикаторов и параметров с целью достижения наилучших значений.

Заключение

В целом данная стратегия — это прорывная стратегия с использованием индикаторов, строгими стоп-лоссом и тейк-профитом. Она эффективно использует преимущества скользящих средних, ATR и RSI, позволяя верно оценивать направление тренда. В сочетании с жесткими правилами стоп-лосса и тейк-профита она помогает получать прибыль от тренда, одновременно контролируя риски. После оптимизации параметров и правил эта стратегия может стать достойной долгосрочного использования количественной торговой стратегией.

/*backtest

start: 2024-01-27 00:00:00

end: 2024-02-03 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="UT Bot Strategy", overlay = true)

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

// Inputs- 1