Двойная стратегия захвата разворотного тренда и динамического стоп-лосса

Обзор

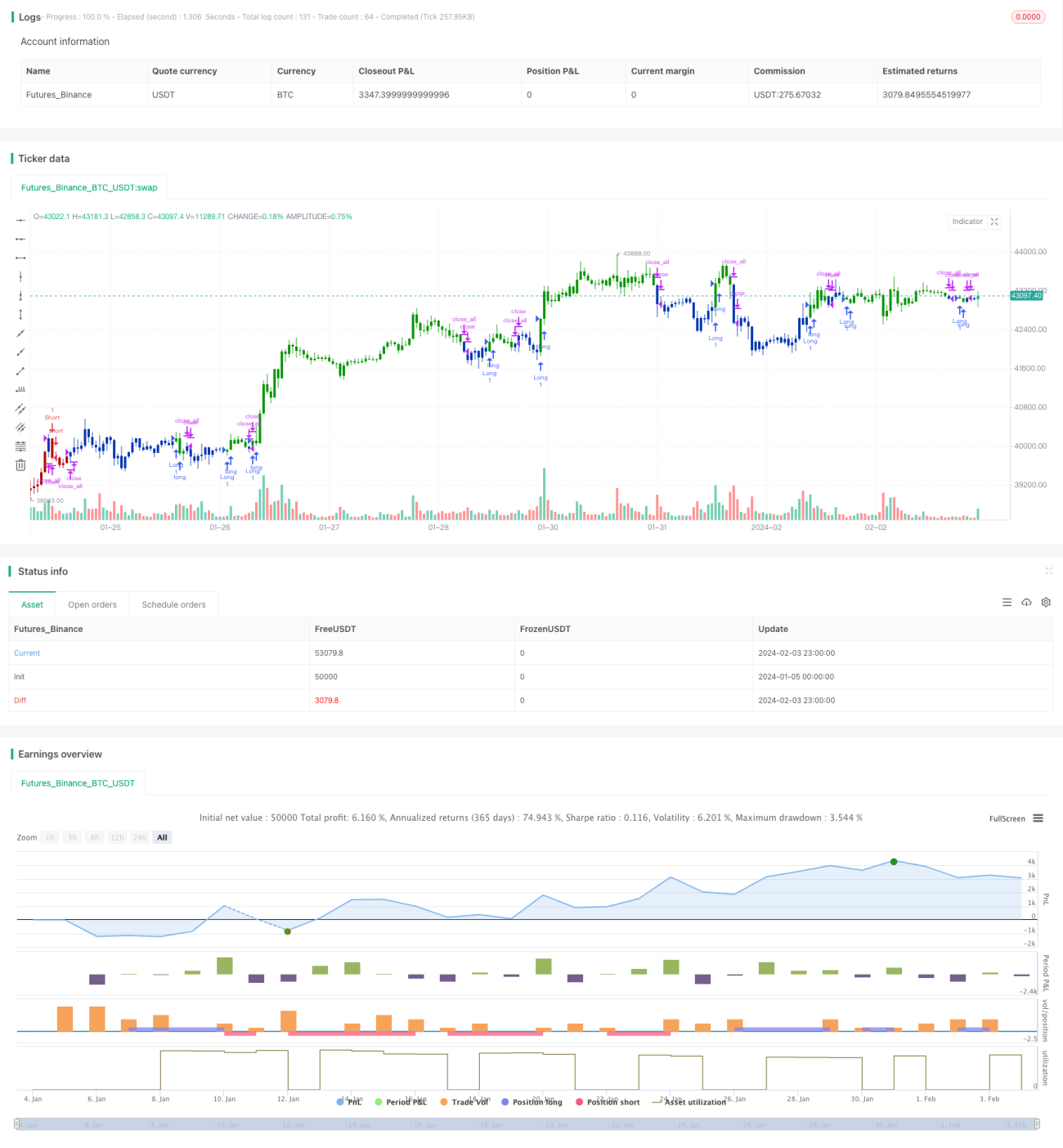

Данная стратегия представляет собой двойной подход, объединяющий стратегию захвата разворотного тренда и стратегию динамического стоп-лосса. Цель – фиксировать развороты тренда, одновременно устанавливая динамические стоп-лоссы для контроля риска.

Принцип стратегии

Стратегия захвата разворотного тренда

Стратегия основана на значениях %K и %D стохастического осциллятора. Сигнал на покупку генерируется, когда цена падает два дня подряд, а значение %K поднимается выше %D. Сигнал на продажу генерируется, когда цена растет два дня подряд, а значение %K опускается ниже %D. Это позволяет улавливать развороты цены.

Стратегия динамического стоп-лосса

Стратегия устанавливает динамический уровень стоп-лосса на основе волатильности цены и асимметрии (skewness). Она рассчитывает колебания максимумов и минимумов цены за последний период, а затем с учетом асимметрии определяет, находится ли рынок в восходящем или нисходящем канале, и динамически корректирует цену стоп-лосса. Это позволяет адаптировать стоп-лосс к рыночным условиям.

Две стратегии используются совместно: после получения сигнала на разворот устанавливается динамический стоп-лосс для контроля риска.

Преимущества

- Позволяет выявлять точки разворота цены, подходит для разворотной торговли.

- Устанавливает динамический стоп-лосс, адаптируясь к рыночным условиям.

- Двойное подтверждение сигналов уменьшает количество ложных сигналов.

- Контролирует риск и обеспечивает прибыль.

Анализ рисков

- Риск неудачного разворота: сигнал разворота может оказаться ложным.

- Риск неправильной настройки параметров: неоптимальные параметры снижают эффективность стратегии.

- Риск ликвидности: низколиквидные инструменты не позволяют исполнить стоп-лосс.

Риски можно снизить путем оптимизации параметров, строгого соблюдения стоп-лосса и выбора ликвидных инструментов.

Направления оптимизации

- Оптимизация параметров стохастического осциллятора для поиска наилучшего сочетания.

- Оптимизация параметров стоп-лосса для определения оптимального уровня.

- Добавление фильтров для избежания открытия позиций на боковом рынке (флэте).

- Внедрение модуля управления позициями для ограничения максимальных убытков.

Комплексная оптимизация позволит стратегии захватывать разворотные движения с минимальным риском.

Заключение

Данная стратегия сочетает захват разворотного тренда и динамический стоп-лосс, что позволяет одновременно фиксировать точки разворота и контролировать риск. Это относительно стабильная краткосрочная торговая стратегия. При постоянном мониторинге и оптимизации она способна приносить стабильную прибыль.

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/12/2020

// This is combo strategies for get a cumulative signal. - 1