Количественная стратегия отслеживания тренда на основе индикаторов Hull и LSMA

Обзор

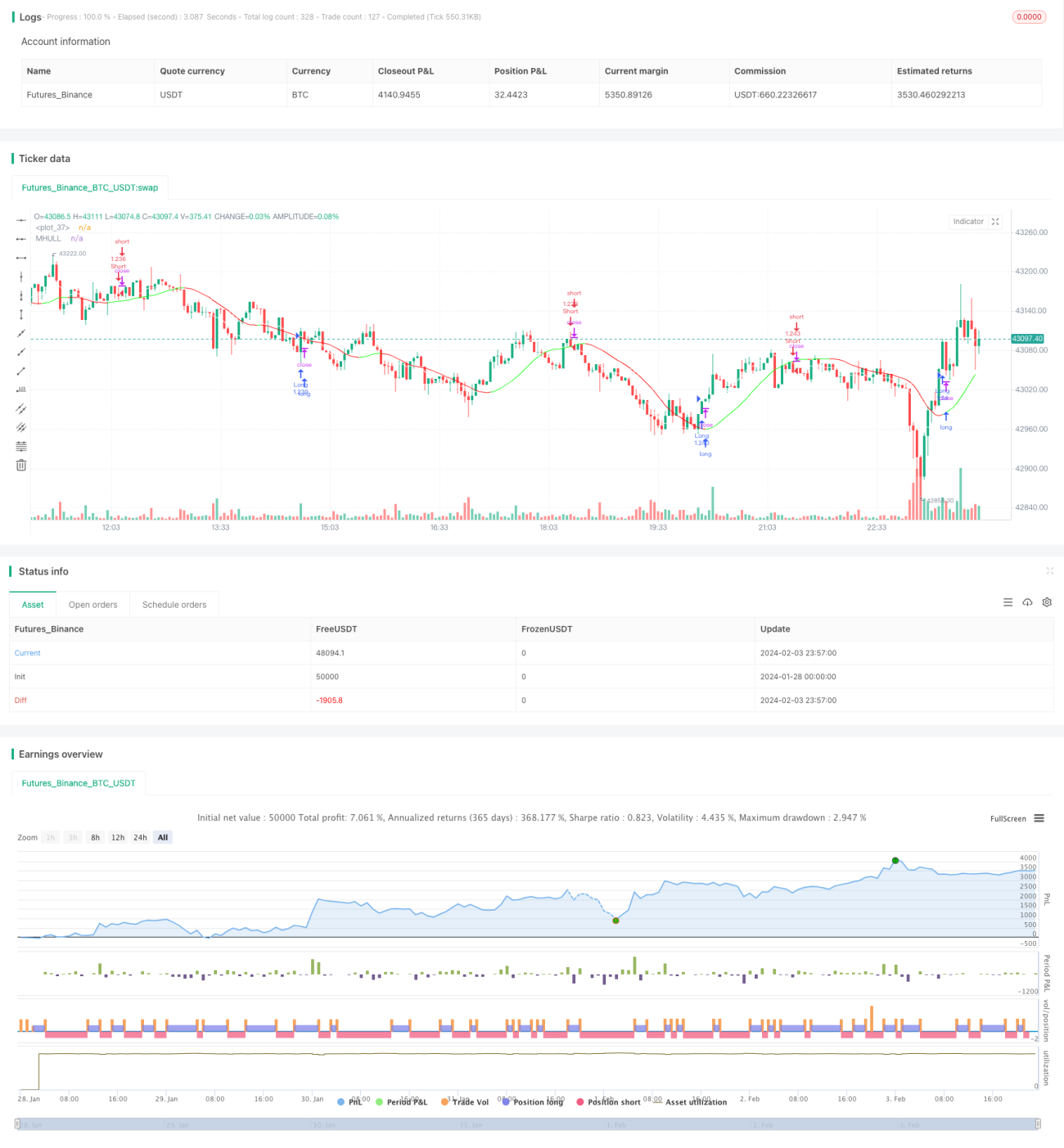

Данная стратегия отслеживает тренд, комбинируя индикатор Hull (Халла) и LSMA (скользящее среднее методом наименьших квадратов) для определения направления тренда и точек разворота. Когда индикатор Hull показывает восходящий тренд, а LSMA пересекает Hull снизу вверх, открывается длинная позиция; когда Hull показывает нисходящий тренд, а LSMA пересекает Hull сверху вниз, открывается короткая позиция. Стратегия подходит для средне-низкочастотной торговли и может использоваться на 1-минутном таймфрейме.

Принцип стратегии

-

Индикатор Hull используется для определения направления тренда цены. Когда средняя линия (MHULL) находится выше нижней линии (LHULL), это указывает на восходящий тренд; в противном случае – на нисходящий.

-

Индикатор LSMA используется для выявления точек разворота тренда. Когда LSMA пересекает MHULL снизу вверх, это сигнализирует о формировании или ускорении восходящего тренда; когда LSMA пересекает MHULL сверху вниз – о формировании или ускорении нисходящего тренда.

-

Комбинируя их: когда индикатор Hull показывает восходящий тренд (MHULL > LHULL) и LSMA пересекает MHULL снизу вверх, открывается длинная позиция; когда индикатор Hull показывает нисходящий тренд (MHULL < LHULL) и LSMA пересекает MHULL сверху вниз, открывается короткая позиция.

-

Стоп-лосс устанавливается по ближайшей экстремальной точке. Для длинной позиции стоп-лосс – последний минимум, для короткой – последний максимум.

Преимущества анализа

Стратегия обладает следующими преимуществами:

-

Индикатор Hull быстро реагирует и своевременно улавливает смену тренда; LSMA обладает высокой сглаженностью, а сигналы разворота надёжны и точны. Их комбинация даёт хороший эффект.

-

Использование пересечения LSMA для фильтрации ложных сигналов индикатора Hull снижает вероятность ошибочных сделок.

-

Установка стоп-лосса по экстремальным точкам максимально защищает капитал.

-

Подходит для средне-низкочастотной торговли, может применяться на 1-минутном и даже более низких таймфреймах, что делает её универсальной.

Анализ рисков

Стратегия также имеет некоторые риски:

-

На боковом рынке индикатор Hull и LSMA могут давать множество пересечений, что приводит к слишком частым сделкам. Следует соответствующим образом настроить параметры для снижения частоты торговли.

-

Установка стоп-лосса по экстремальным точкам может вызвать его активацию из-за краткосрочных ценовых корректировок, поэтому расстояние до стоп-лосса следует немного увеличить.

-

Из-за запаздывания индикатора LSMA возможны небольшие ошибки. Рекомендуется подтверждать сигналы с помощью других индикаторов, например, свечных паттернов.

Направления оптимизации

Стратегию можно оптимизировать по следующим направлениям:

-

Оптимизация параметров индикатора Hull и LSMA для лучшего соответствия различным инструментам и временным периодам.

-

Добавление фильтров на основе волатильности, объёма и т.д., чтобы избежать ошибочных сделок на боковом рынке.

-

Внедрение алгоритмов машинного обучения для оценки склонности к тренду.

-

Использование технологий глубокого обучения для определения ключевых зон поддержки и сопротивления, что сделает стоп-лоссы более обоснованными.

Заключение

Данная стратегия, комбинируя индикаторы Hull и LSMA, определяет изменение направления тренда и реализует следование за трендом. Её преимущества: простота, быстрота реакции и широкая применимость в средне-низкочастотной количественной торговле. Дальнейшая оптимизация фильтров, вспомогательных индикаторов и алгоритмов стоп-лосса может привести к улучшению результатов.

- 1