Справочная стратегия для восходящего тренда прорывного типа

Обзор

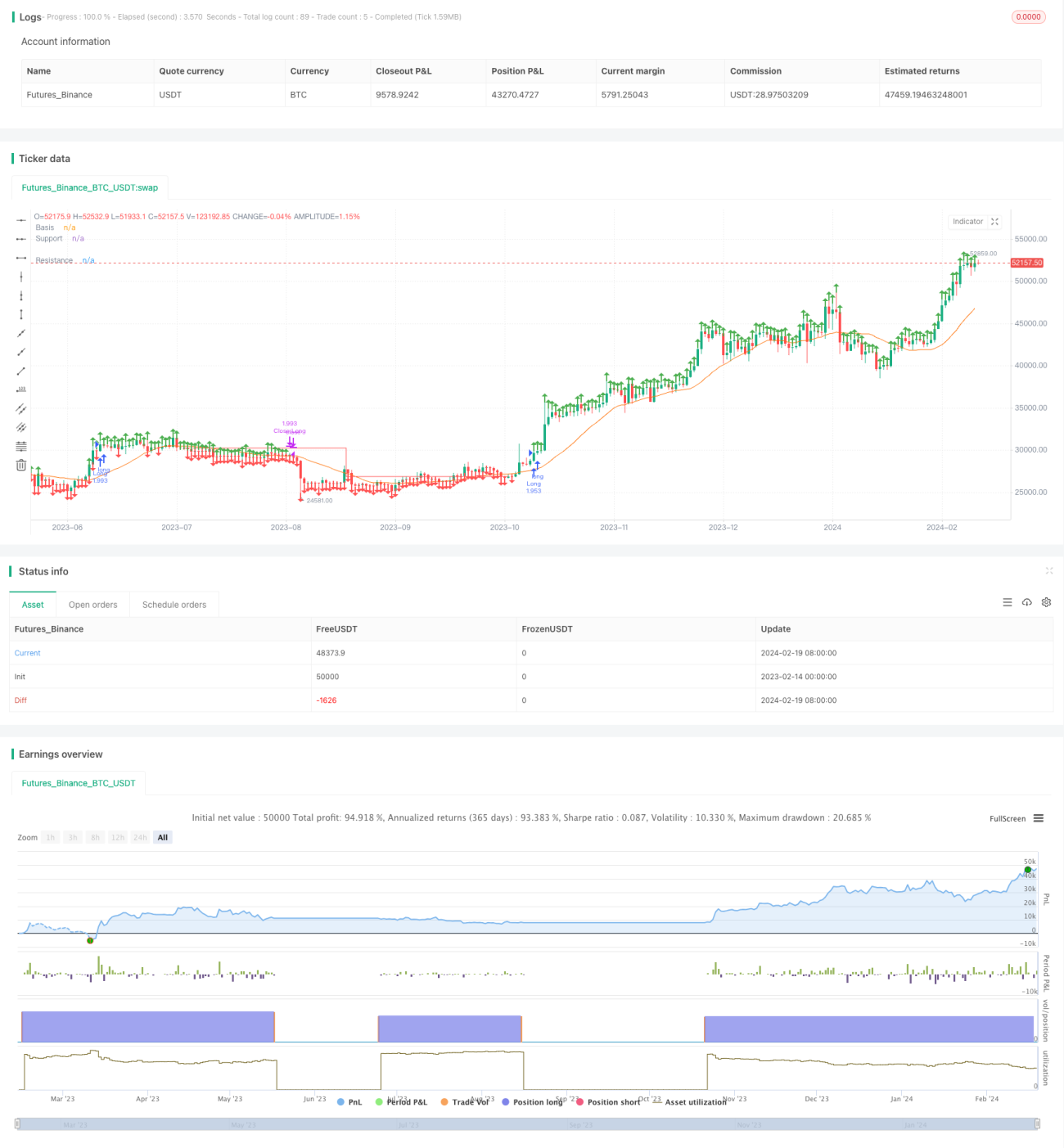

Данная стратегия представляет собой долгосрочную позиционную стратегию, основанную на определении направления тренда с помощью простой скользящей средней и формировании сигналов прорыва через уровни сопротивления и поддержки. С помощью расчета Pivot-максимумов и Pivot-минимумов строятся линии сопротивления и поддержки. При пробое цены вверх через линию сопротивления открывается длинная позиция, при пробое вниз через линию поддержки – закрывается. Стратегия подходит для акций с явно выраженным трендом и позволяет получить хорошее соотношение риска и доходности.

Принцип стратегии

- Рассчитывается 20-дневная простая скользящая средняя в качестве базовой линии для определения тренда.

- На основе введенных пользователем параметров вычисляются Pivot-максимумы и Pivot-минимумы.

- По Pivot-максимумам и Pivot-минимумам строятся линии сопротивления и поддержки.

- Когда цена закрытия выше линии сопротивления, открывается длинная позиция.

- Когда линия поддержки пересекает линию сопротивления снизу вверх, позиция закрывается.

Стратегия использует простую скользящую среднюю для определения общего направления тренда, а затем формирует торговые сигналы на основе пробоя ключевых уровней – это типичная пробойная стратегия. Благодаря анализу ключевых уровней и тренда она позволяет эффективно отсеивать ложные пробои.

Анализ преимуществ

- Достаточное количество торговых сигналов, подходит для высоковолатильных акций, легко захватывает тренды.

- Хороший контроль риска, высокое соотношение риска и доходности.

- Использование сигналов пробоя позволяет избежать риска ложных пробоев.

- Настраиваемые параметры, высокая адаптивность.

Анализ рисков

- Зависит от оптимизации параметров – неверно подобранные параметры увеличивают вероятность ложных пробоев.

- Запаздывание сигналов пробоя может привести к упущенным возможностям.

- В боковом рынке высока вероятность срабатывания стоп-лоссов.

- Несвоевременная корректировка линии поддержки может привести к убыткам.

Риски можно снизить путем оптимизации параметров на реальных торгах и комбинирования с механизмами стоп-лосса и тейк-профита.

Направления оптимизации

- Оптимизация периода скользящей средней.

- Оптимизация параметров линий поддержки и сопротивления.

- Добавление стратегий стоп-лосса и тейк-профита.

- Внедрение механизма подтверждения пробоя.

- Фильтрация сигналов с помощью таких индикаторов, как объем торгов.

Заключение

В целом данная стратегия является типичной пробойной, зависит от оптимизации параметров и ликвидности и подходит для трейдеров, следующих за трендом. Как опорная схема, она может быть расширена модулями в соответствии с реальными потребностями, а риски могут быть снижены за счет таких механизмов, как стоп-лосс / тейк-профит и фильтрация сигналов, что повышает стабильность.

- 1