Многоиндикаторная стратегия количественной торговли на основе технического анализа

Обзор

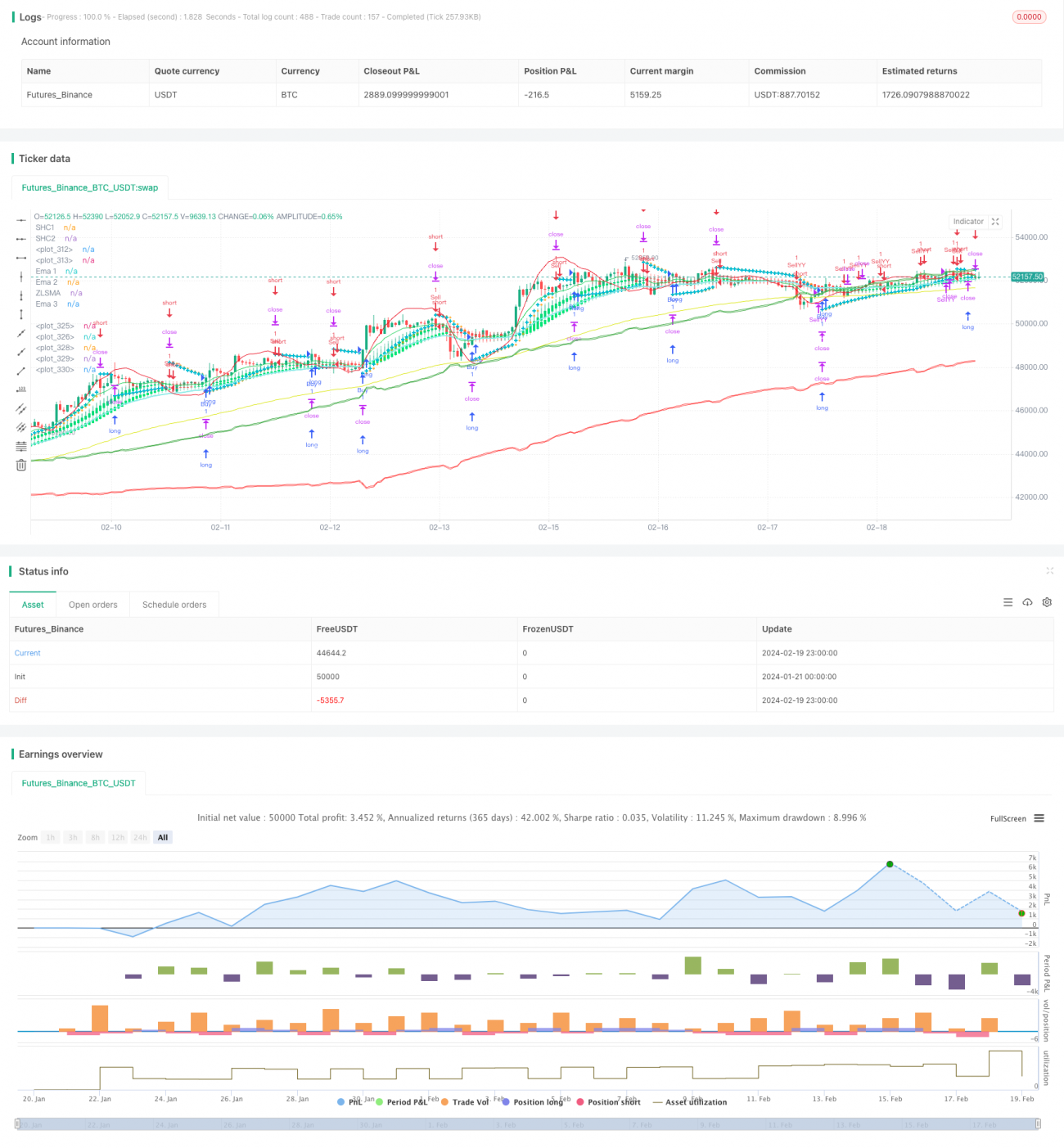

Данная стратегия комплексно использует различные технические индикаторы, включая параболическую систему разворота, стратегию выхода по теории Чань, скользящую среднюю с нулевым запаздыванием, экспоненциальную скользящую среднюю, трендовую скользящую среднюю и другие, для выявления потенциальных точек покупки и продажи на графике.

Принципы стратегии

Основные индикаторы

- Параболическая система разворота (Parabolic SAR): используется для определения уровней стоп-лосса и потенциальных точек входа.

- Стратегия выхода по теории Чань: применяется для определения направления тренда.

- Скользящая средняя с нулевым запаздыванием (Zero Lag SMA): обеспечивает скользящую среднюю с низкой задержкой.

- Экспоненциальная скользящая средняя (EMA): отслеживает ценовой тренд и волатильность.

- Сглаженная скользящая средняя: формирует более гладкую среднюю линию.

Торговые сигналы

- Длинная позиция открывается, когда параболическая система показывает восходящий тренд и цена превышает 99-ю экспоненциальную скользящую среднюю; короткая позиция – когда система показывает нисходящий тренд и цена ниже 99-й экспоненциальной скользящей средней.

- Сигналы стратегии выхода по теории Чань используются для дополнительного подтверждения направления тренда.

- Сглаженная скользящая средняя применяется совместно с сигналами параболической системы для избежания ложных пробоев.

Управление рисками

- Установка стоп-лосса и тейк-профита.

- Рассматривается возможность сброса условий покупки для гибкой корректировки позиций.

Анализ преимуществ

Главное преимущество стратегии – комплексный набор индикаторов, который эффективно определяет направление тренда. Параболическая система определяет потенциальные точки разворота; стратегия выхода по теории Чань оценивает основной тренд; скользящие средние отфильтровывают ложные сигналы. Взаимная проверка нескольких индикаторов значительно повышает точность сигналов.

Кроме того, стратегия включает механизмы стоп-лосса и тейк-профита для контроля рисков. Сглаженная скользящая средняя также помогает избежать помех от краткосрочных шумов. Всё это обеспечивает высокую стабильность стратегии.

Анализ рисков

Из-за зависимости от большого числа индикаторов стратегия может столкнуться с трудностями, когда эти индикаторы подают противоречивые сигналы. Кроме того, неправильная настройка параметров может негативно повлиять на торговлю.

Также сама по себе техническая торговля сопряжена с определёнными рисками и не может полностью исключить убытки. Необходимо действовать осторожно и избегать слепого следования сигналам.

Направления оптимизации

- Тестирование и оптимизация параметров индикаторов для поиска наилучшей комбинации.

- Внедрение алгоритмов машинного обучения для обучения модели на больших данных с целью дальнейшего повышения точности сигналов.

- Интеграция индикаторов настроений и новостной информации для оценки рыночной ситуации, динамическая корректировка позиций и уровней стоп-лосса.

- Оптимизация логики сброса условий покупки для более гибкого и непрерывного обнаружения сигналов.

Заключение

Данная стратегия объединяет множество технических индикаторов для выявления торговых сигналов на основе их комбинации. Преимущества – высокая точность сигналов и стабильность. При этом меры контроля рисков реализованы должным образом. В целом, это заслуживающая рассмотрения торговая система. В дальнейшем она может быть усовершенствована путём оптимизации параметров, обучения модели, внедрения индикаторов настроений и других методов.

- 1