Стратегия отслеживания тренда на основе пересечения DEMA

Обзор

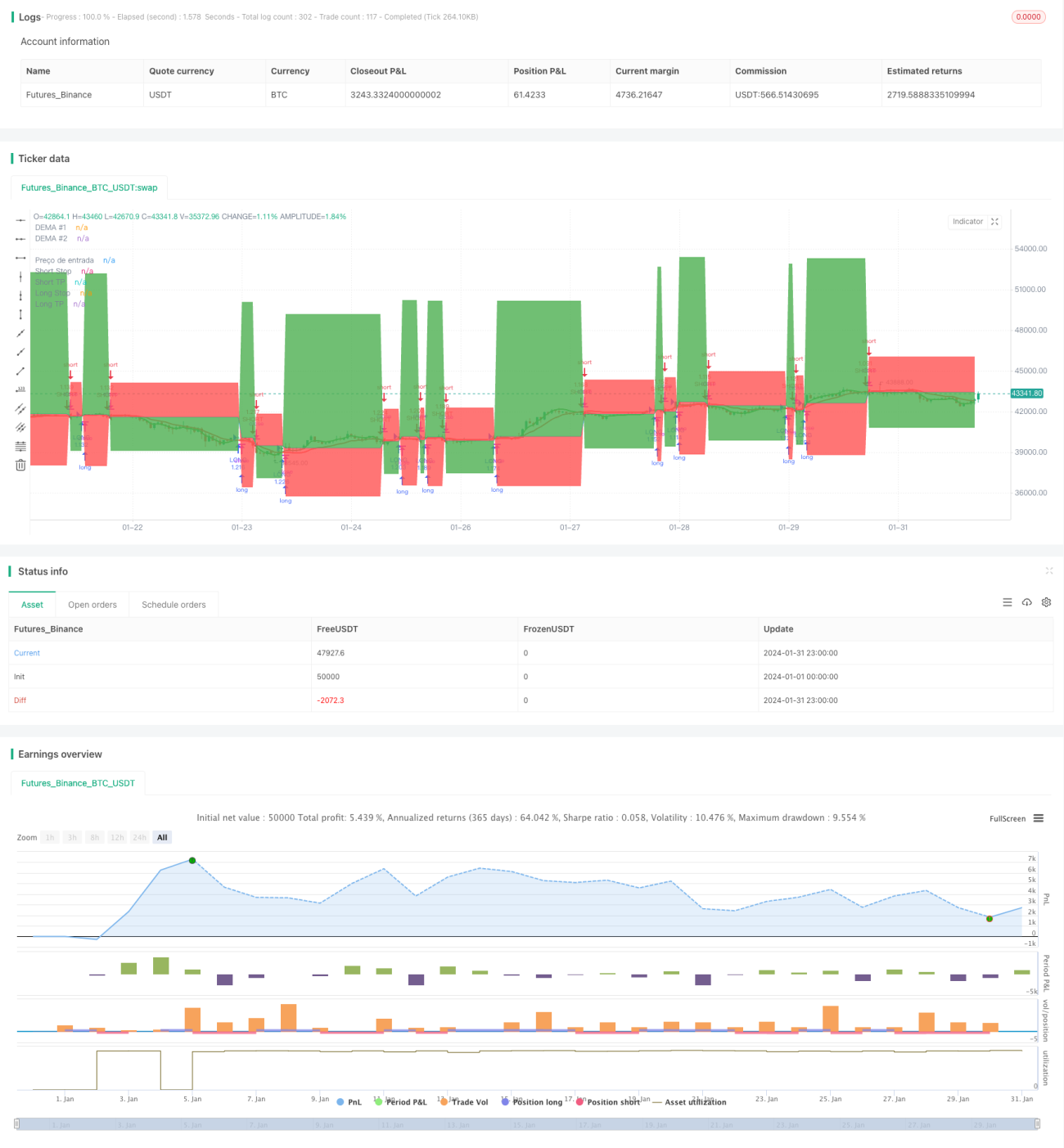

Данная стратегия основана на пересечении двойных экспоненциальных скользящих средних (DEMA) как торгового сигнала, использует следование за трендом и автоматически устанавливает стоп-лосс и тейк-профит. Преимущества стратегии: четкие торговые сигналы, гибкая настройка стоп-лосса и тейк-профита, эффективный контроль рисков.

Принцип стратегии

-

Рассчитываются быстрая линия DEMA (8 периодов), медленная линия DEMA (24 периода) и вспомогательная линия DEMA (настраиваемая).

-

Когда быстрая линия пересекает медленную линию снизу вверх (золотое пересечение) – открывается длинная позиция; когда быстрая линия пересекает медленную линию сверху вниз (мертвое пересечение) – открывается короткая позиция.

-

Добавлен фильтр торговых сигналов: сигнал генерируется только в том случае, если текущее значение вспомогательной линии выше предыдущего, чтобы избежать ложных пробоев.

-

Используется механизм трейлингового стоп-лосса: линия стоп-лосса корректируется в зависимости от движения цены, что позволяет зафиксировать часть прибыли.

-

Одновременно устанавливаются фиксированные процентные стоп-лосс и тейк-профит для контроля максимального убытка и прибыли по одной сделке.

Преимущества стратегии

-

Четкие торговые сигналы, легко определять моменты входа и выхода.

-

Алгоритм двойной DEMA более сглажен, избегает чрезмерной оптимизации, сигналы надежнее.

-

Фильтр вспомогательной линии повышает эффективность сигналов, уменьшая количество ложных.

-

Использование трейлингового стоп-лосса позволяет зафиксировать часть прибыли и эффективно контролировать риски.

-

Установка фиксированных процентных стоп-лосса и тейк-профита ограничивает максимальный убыток по одной сделке, не допуская выхода за пределы допустимого риска.

Риски стратегии

-

В условиях бокового рынка возможно частое совершение сделок, что увеличивает издержки и может привести к убыткам.

-

Слишком большой фиксированный стоп-лосс при аномальных движениях рынка может вызвать крупный убыток.

-

Сигнал пересечения DEMA запаздывает, при быстром движении вход вблизи максимумов может увеличить риск убытка.

-

При реальной торговле проскальзывание влияет на прибыльность, требуется корректировка параметров тейк-профита и стоп-лосса.

Оптимизация стратегии

-

Параметры DEMA можно настраивать в зависимости от рыночных условий для поиска оптимального баланса.

-

В реальной торговле необходимо учитывать проскальзывание и соответствующим образом расширять диапазон фиксированного стоп-лосса.

-

Можно добавить дополнительные вспомогательные индикаторы, например MACD, для усиления сигналов.

-

Возможно задать шаг трейлингового стоп-лосса для оптимизации логики.

Заключение

Данная стратегия использует способность DEMA определять тренд в сочетании с механизмом следования за трендом для контроля рисков. Она является типичным представителем стратегий, определяющих направление тренда. В целом стратегия отличается четкими сигналами, разумной настройкой стоп-лосса и тейк-профита, проста в освоении и позволяет контролировать риски. При реальной торговле с учетом оптимизации проскальзывания и вспомогательных индикаторов можно получить хорошую доходность.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1