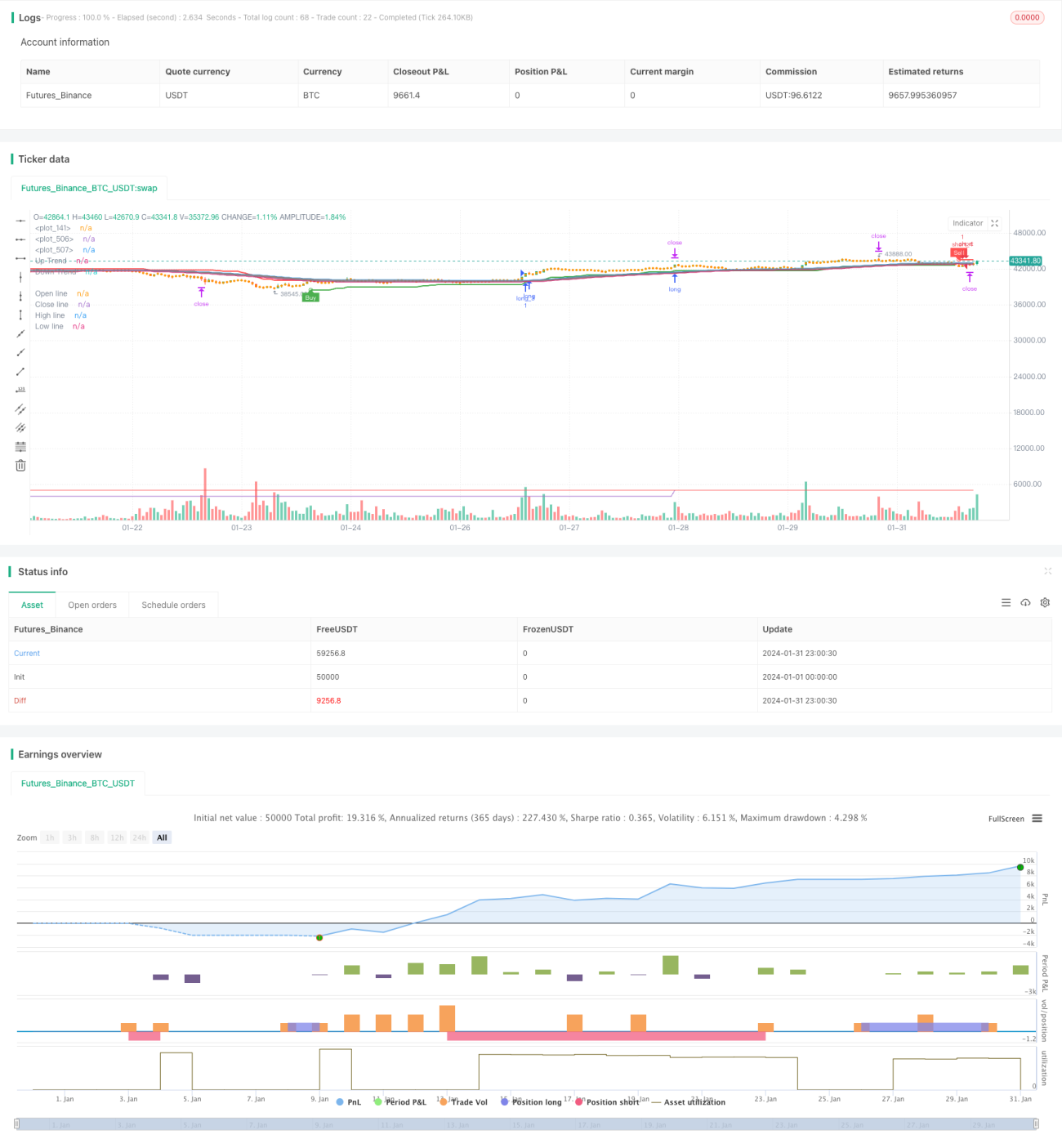

Стратегия отслеживания тренда с тройным подтверждением

Обзор

Стратегия отслеживания тренда с тройным подтверждением использует комбинацию сигналов трех основных индикаторов: скользящей средней, линии Ichimoku и супертренда для высоковероятностного захвата тренда. Когда все три индикатора одновременно подают сигнал на покупку или продажу, стратегия своевременно входит в рынок и отслеживает тренд; при развороте тренда стратегия быстро закрывает позицию с убытком и открывает короткую позицию.

Принцип стратегии

Определение основного тренда по скользящей средней

Стратегия использует скользящую среднюю с периодом 52 для определения направления основного тренда. Когда цена пересекает скользящую среднюю снизу вверх – тренд восходящий; когда цена пересекает скользящую среднюю сверху вниз – тренд нисходящий.

Линия Ichimoku для выявления вторичных разворотов

Стратегия также использует линию Ichimoku для выявления краткосрочных вторичных разворотов. Метод расчета линии Ichimoku аналогичен скользящей средней, но цена закрытия заменяется ценой открытия, что позволяет быстрее отражать развороты цены. Когда цена пересекает падающую линию Ichimoku снизу вверх, это сигнализирует о краткосрочной стабилизации и отскоке цены; когда цена пересекает растущую линию Ichimoku сверху вниз – о краткосрочном снижении цены.

Определение точек разворота с помощью супертренда

Стратегия также использует индикатор супертренда для выявления ключевых точек разворота. Индикатор супертренда использует период ATR и данные цены для динамической корректировки верхней и нижней границ канала, определяя момент разворота.

Фильтрация сигналов с тройным подтверждением

Когда все три индикатора – скользящая средняя, линия Ichimoku и супертренд – одновременно подают сигнал на покупку, стратегия открывает длинную позицию; когда все три индикатора одновременно подают сигнал на продажу – открывает короткую позицию. Тройное подтверждение позволяет эффективно отсеивать ложные сигналы и повышать вероятность успешного входа.

Преимущества

Многомерная оценка, высокая вероятность

Комбинация скользящей средней, линии Ichimoku и супертренда позволяет оценивать тренд и ключевые точки с разных сторон, обеспечивая высокую вероятность входа.

Быстрая реакция, отслеживание в реальном времени

Линия Ichimoku обеспечивает быструю реакцию стратегии на краткосрочные развороты цены; супертренд с адаптивным каналом на основе ATR также отслеживает изменения цены в реальном времени.

Автоматический фиксация прибыли и стоп-лосс, эффективный контроль рисков

Стратегия имеет встроенную логику автоматического фиксации прибыли и стоп-лосса, которая динамически корректирует уровни на основе ATR, эффективно контролируя убыток по каждой сделке.

Риски и их устранение

Риск чрезмерной частоты торгов

Из-за частых торговых сигналов возможна излишняя активность. Рекомендуется увеличить период скользящей средней, чтобы уменьшить частоту сделок.

Риск неопределенности разворота

Линия Ichimoku и супертренд не всегда точно определяют точки разворота, возможны ошибки. Можно ужесточить фильтры параметров индикаторов, чтобы повысить вероятность точных сигналов разворота.

Риск убытков в боковом тренде

При боковом движении из-за многократных пересечений стратегия будет часто открывать позиции и закрывать их с убытком. Можно идентифицировать боковой тренд и приостанавливать торговлю на этом этапе.

Направления оптимизации

Добавление индикатора волатильности

Можно рассмотреть добавление индикатора волатильности, например полос Боллинджера. Если цена приближается к верхней или нижней границе полос, избегать открытия новых позиций – это поможет снизить риск в боковом рынке.

Ужесточение фильтров входа

Можно попробовать добавить дополнительные вспомогательные индикаторы, такие как KDJ, MACD, и входить только при одновременном сигнале от всех. Это дополнительно отсеет ложные сигналы и уменьшит количество ненужных сделок.

Оптимизация стратегии фиксации прибыли и стоп-лосса

Можно оптимизировать тактику фиксации прибыли и стоп-лосса, например, использовать трейлинг-стоп, экспоненциальный трейлинг-стоп, частичную фиксацию с интервалом, чтобы сделать прибыль более стабильной и увеличить ее.

Заключение

Стратегия отслеживания тренда с тройным подтверждением эффективно использует преимущества скользящей средней, линии Ichimoku и супертренда для высоковероятностного определения и захвата тренда. Встроенный механизм автоматической фиксации прибыли и стоп-лосса позволяет эффективно контролировать убыток по каждой сделке. Дальнейшая оптимизация может включать добавление вспомогательных индикаторов для фильтрации входа, а также улучшение тактики фиксации прибыли и стоп-лосса, что сделает стратегию более практичной.

- 1