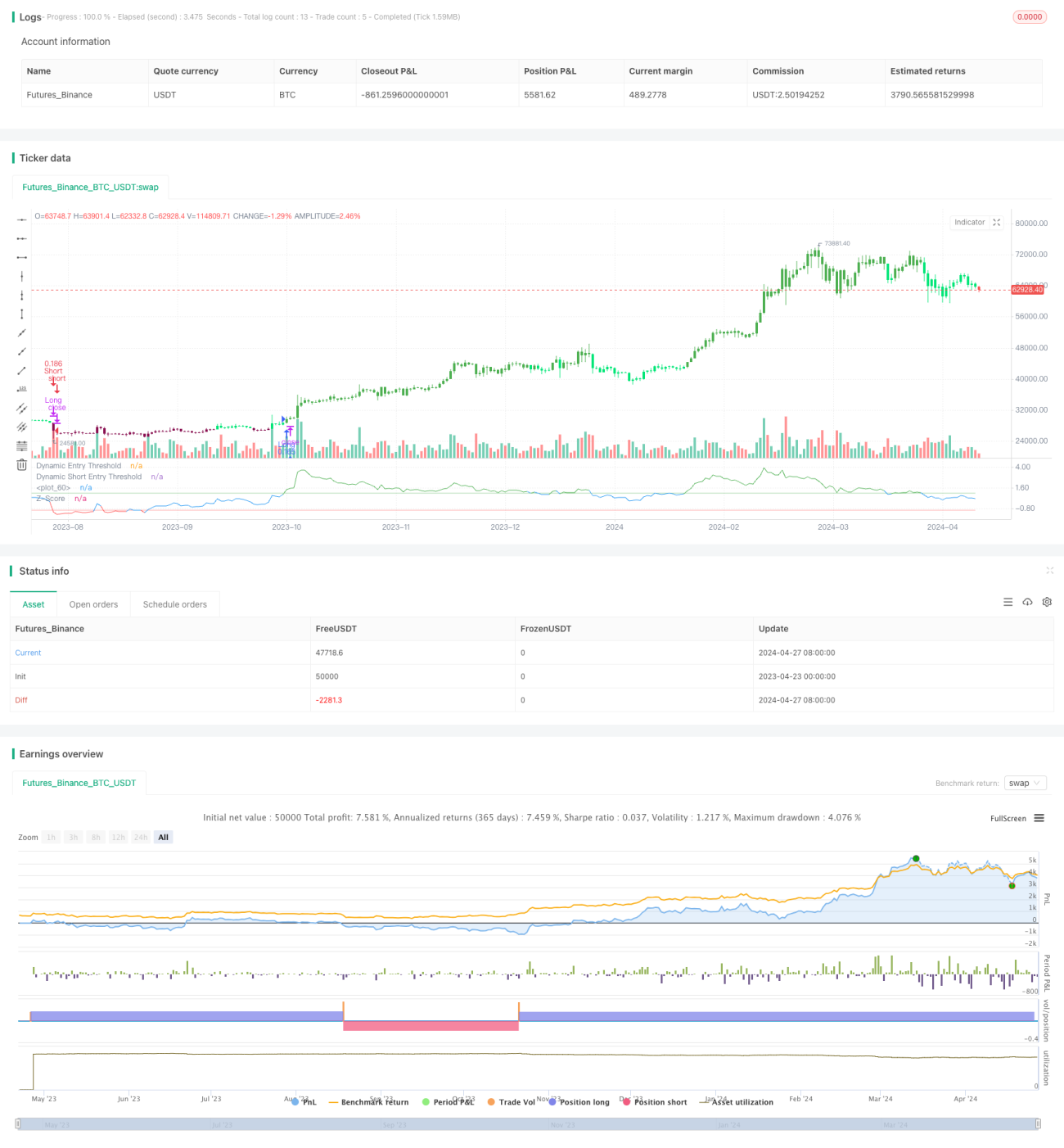

Стратегия трендового следования на основе Z-значения

Обзор

«Стратегия следования за трендом на основе Z-счета» использует статистический показатель Z-счет для измерения отклонения цены от ее скользящей средней, нормированного на стандартное отклонение, чтобы улавливать трендовые возможности. Стратегия отличается простотой и эффективностью, особенно на рынках, где цены часто возвращаются к среднему значению. В отличие от сложных систем, основанных на множестве индикаторов, «Z-счет трендовая стратегия» фокусируется на четких, статистически значимых движениях цены, что делает ее идеальной для трейдеров, предпочитающих лаконичные, управляемые данными подходы.

Принцип стратегии

Основой стратегии является расчет Z-счета. Z-счет вычисляется как разность между текущей ценой и экспоненциальной скользящей средней (EMA) заданной пользователем длины, деленная на стандартное отклонение цены за тот же период:

z = (x - μ) / σ

где x — текущая цена, μ — среднее значение EMA, σ — стандартное отклонение.

Торговые сигналы генерируются при пересечении Z-счетом заданных пороговых значений:

- Вход в длинную позицию: когда Z-счет пересекает положительный порог снизу вверх.

- Выход из длинной позиции: когда Z-счет пересекает отрицательный порог сверху вниз.

- Вход в короткую позицию: когда Z-счет пересекает отрицательный порог сверху вниз.

- Выход из короткой позиции: когда Z-счет пересекает положительный порог снизу вверх.

Преимущества стратегии

- Простота и эффективность: стратегия использует лишь несколько параметров, легка в понимании и реализации, при этом успешно улавливает трендовые возможности.

- Статистическая основа: Z-счет как устоявшийся статистический инструмент обеспечивает стратегии прочную теоретическую базу.

- Адаптивность: параметры, такие как пороговые значения, период EMA и стандартного отклонения, могут быть настроены для различных торговых стилей и рыночных условий.

- Четкие сигналы: сигналы, основанные на пересечении Z-счетом порогов, просты и понятны, что способствует быстрому принятию решений и исполнению.

Риски стратегии

- Чувствительность к параметрам: неправильный выбор параметров (например, слишком высокий или низкий порог) может исказить торговые сигналы, привести к упущенным возможностям или убыткам.

- Идентификация тренда: на боковых или консолидационных рынках стратегия может генерировать частые ложные сигналы и показывать низкую эффективность.

- Эффект запаздывания: как стратегия следования за трендом, она имеет некоторое запаздывание при входе и выходе, что может привести к упущению оптимальных моментов.

Эти риски могут быть контролируемы и смягчены путем постоянного анализа рынка, оптимизации параметров и осторожной реализации на основе бэктестинга.

Направления оптимизации стратегии

- Динамические пороги: введение порогов, зависящих от волатильности, позволяет эффективно адаптироваться к различным рыночным состояниям и повысить качество сигналов.

- Комбинация индикаторов: использование дополнительных технических индикаторов, таких как RSI, MACD, для вторичного подтверждения торговых сигналов, повышая надежность.

- Управление позицией: включение механизмов контроля позиции, таких как ATR, для своевременного сокращения позиции на волатильных рынках и увеличения на трендовых, оптимизируя соотношение риск/доходность.

- Множественные временные масштабы: расчет Z-счета на нескольких таймфреймах для улавливания трендов разных уровней, обогащая размерность стратегии.

Заключение

«Стратегия следования за трендом на основе Z-счета» благодаря своей простоте, устойчивости и гибкости предлагает уникальный взгляд на улавливание трендовых возможностей. При правильной настройке параметров, осторожном управлении рисками и постоянной оптимизации эта стратегия может стать надежным помощником количественного трейдера, уверенно двигаясь в изменчивом рынке.

/*backtest

start: 2023-04-23 00:00:00

end: 2024-04-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy employs a statistical approach by using a Z-score, which measures the deviation of the price from its moving average normalized by the standard deviation.- 1