Обзор

Данная стратегия представляет собой краткосрочную валютную торговую стратегию, основная идея которой заключается в усилении управления рисками за счет динамического изменения размера позиции. Стратегия рассчитывает динамический размер позиции на основе текущего капитала счета и процента риска на одну сделку. Кроме того, устанавливаются строгие условия стоп-лосса и тейк-профита, позволяющие быстро закрыть позицию при неблагоприятном движении цены (контроль риска) и своевременно зафиксировать прибыль при движении в благоприятном направлении.

Принцип стратегии

- На основе введенных пользователем параметров, таких как количество дней удержания краткосрочной позиции, процент снижения цены, процент риска на одну сделку, процент стоп-лосса и процент тейк-профита, инициализируются соответствующие переменные.

- При отсутствии открытой позиции рассчитывается динамический размер позиции на основе текущего капитала счета и процента риска на одну сделку, после чего открывается короткая позиция по рыночной цене.

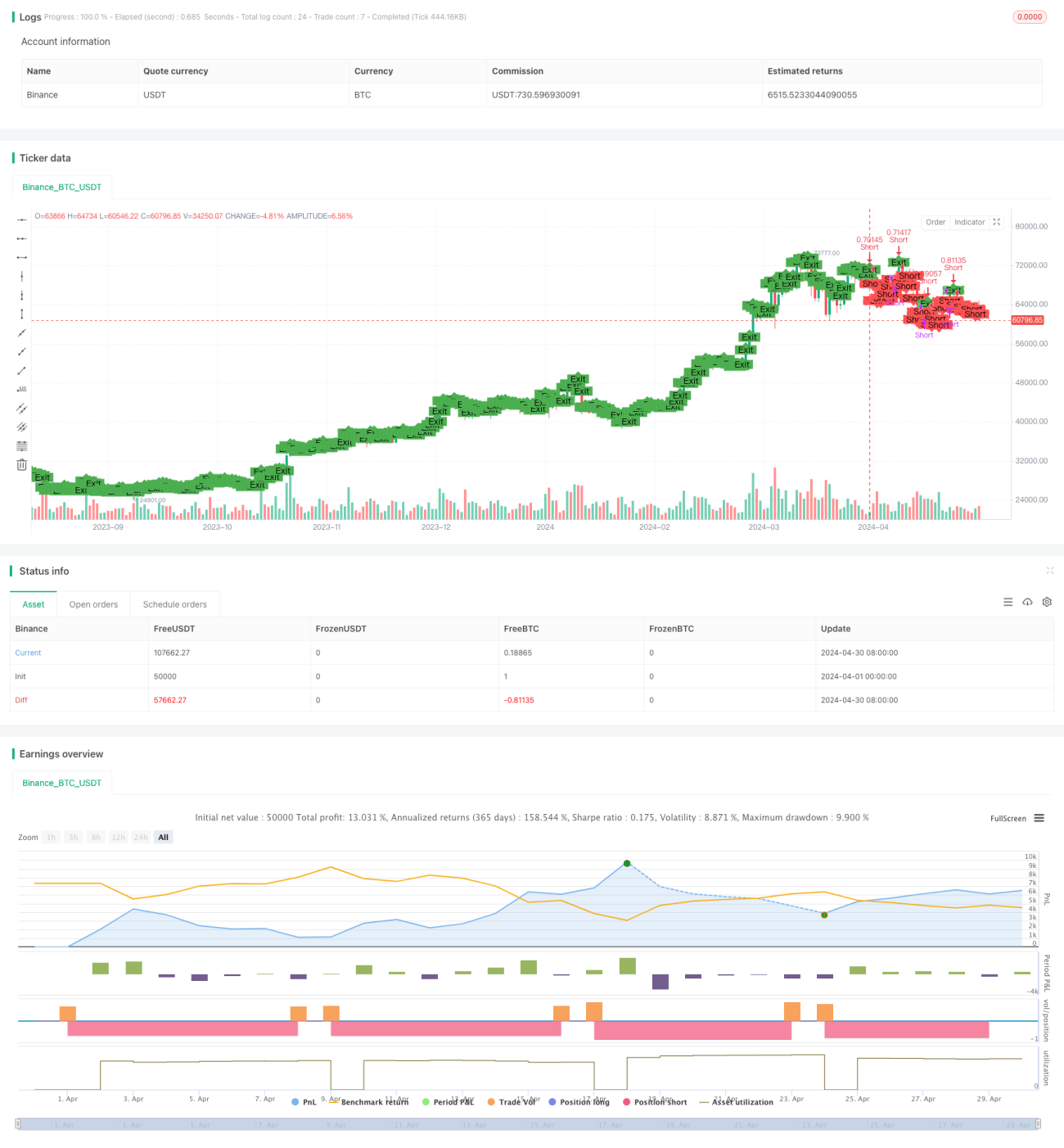

- Фиксируется цена открытия и ожидаемое время закрытия позиции.

- Во время удержания позиции в реальном времени отслеживаются изменения цены. При достижении уровня стоп-лосса, тейк-профита или установленного времени удержания позиция закрывается.

- На графике отмечаются точки открытия и закрытия позиций для наглядного отображения хода торгов.

Анализ преимуществ

- Динамический размер позиции: размер позиции для каждой сделки динамически корректируется в зависимости от капитала счета и процента риска, что позволяет контролировать риски и повышать эффективность использования средств.

- Строгие стоп-лосс и тейк-профит: установка плотных уровней стоп-лосса и тейк-профита позволяет эффективно ограничивать риск по одной сделке и своевременно фиксировать прибыль.

- Краткосрочная торговля: стратегия ориентирована на краткосрочные торговые возможности, время удержания позиции невелико, что позволяет быстро адаптироваться к изменениям рынка и использовать краткосрочные ценовые колебания.

- Простота использования: логика стратегии понятна, параметры настраиваются просто, что подходит для изучения и применения начинающими трейдерами.

Анализ рисков

- Рыночный риск: валютный рынок быстро меняется, краткосрочные колебания цен могут быть сильными, что может привести к частому срабатыванию стоп-лосса.

- Риск настройки параметров: неправильные настройки параметров, такие как слишком высокий процент риска или слишком узкие диапазоны стоп-лосса и тейк-профита, могут привести к быстрой потере капитала.

- Риск размера позиции: несмотря на использование динамического размера позиции, необходимо осторожно задавать процент риска на одну сделку, чтобы избежать чрезмерного отвлечения средств в одной сделке.

Направления оптимизации

- Внедрение дополнительных технических индикаторов, таких как скользящие средние, MACD и др., для вспомогательного определения тренда и моментов входа/выхода.

- Оптимизация логики стоп-лосса и тейк-профита, например, использование трейлинг-стопа, частичного закрытия позиции и т.д., для улучшения соотношения прибыли к риску.

- Настройка различных комбинаций параметров для разных валютных пар и рыночных ситуаций, чтобы повысить адаптивность и стабильность стратегии.

- Включение логики управления позицией, например, использование формулы Келли, для динамического изменения процента риска на каждую сделку.

Заключение

Данная стратегия с помощью динамического размера позиции и строгих стоп-лосса/тейк-профита достигает баланса между контролем рисков и стремлением к прибыли в краткосрочной торговле. Логика стратегии проста и понятна, что подходит для освоения новичками. Однако при практическом применении необходимо соблюдать осторожность, контролировать риски и постоянно оптимизировать и совершенствовать стратегию в соответствии с изменениями рынка. Внедрение дополнительных технических индикаторов, оптимизация логики стоп-лосса и тейк-профита, настройка параметров для различных рыночных условий, добавление методов управления позициями и т.д. могут дополнительно повысить надежность и прибыльность стратегии.

- 1