Стратегия динамической корректировки тейк-профита и стоп-лосса на основе Williams %R

Обзор

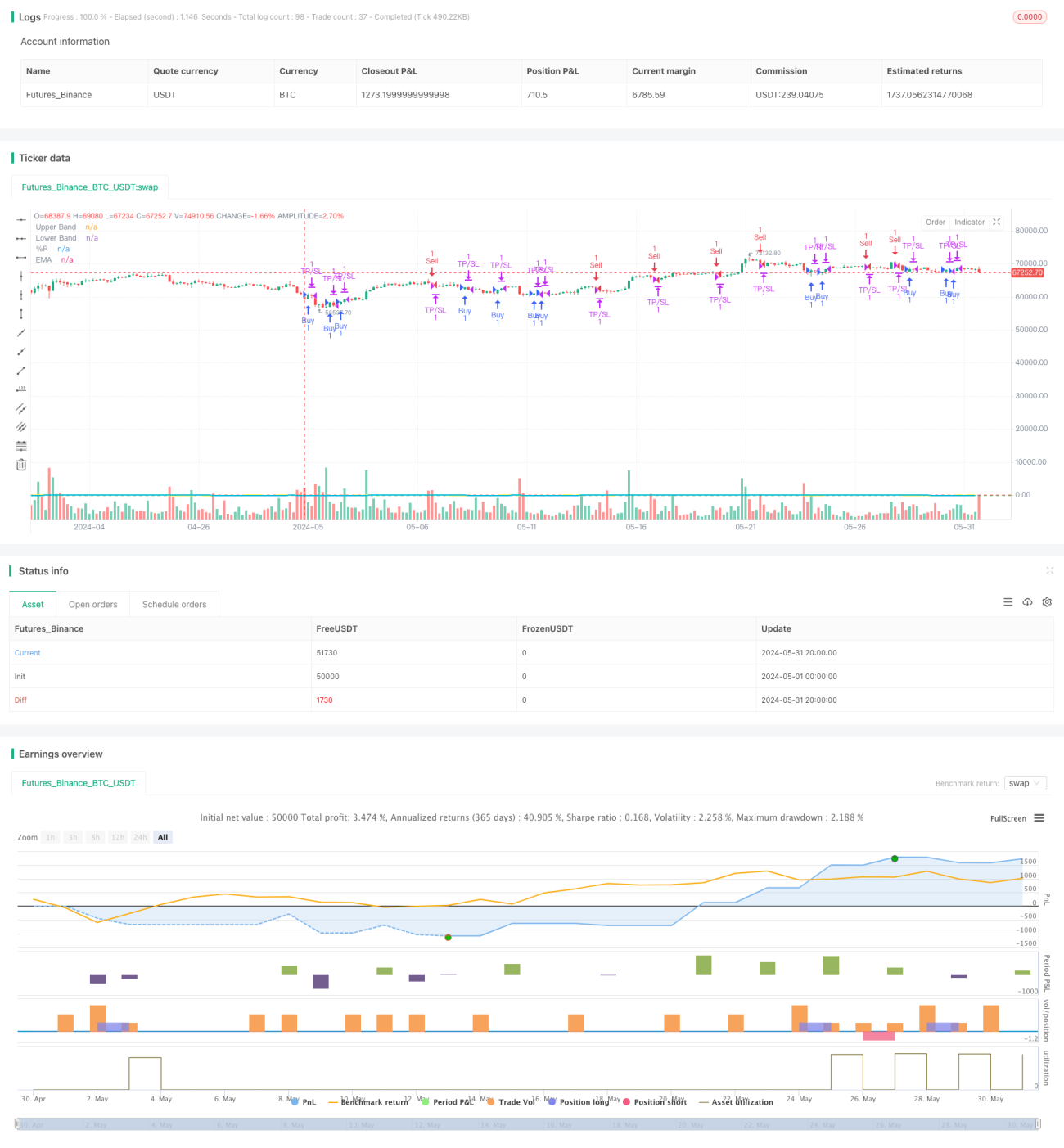

Данная стратегия основана на индикаторе Williams %R и оптимизирует торговые результаты путем динамической корректировки уровней тейк-профита и стоп-лосса. Сигнал на покупку генерируется при пересечении Williams %R из зоны перепроданности (-80), а сигнал на продажу — при пересечении из зоны перекупленности (-20). Для сглаживания значений Williams %R используется экспоненциальная скользящая средняя (EMA), что снижает шум. Стратегия предлагает гибкие настройки параметров, включая период индикатора, уровни тейк-профита и стоп-лосса (TP/SL), время торговли и направление сделок, что позволяет адаптироваться к различным рыночным условиям и предпочтениям трейдера.

Принцип стратегии

- Рассчитывается значение Williams %R за заданный период.

- Вычисляется экспоненциальная скользящая средняя (EMA) Williams %R.

- Когда Williams %R пересекает уровень -80 снизу вверх, генерируется сигнал на покупку; при пересечении уровня -20 сверху вниз — сигнал на продажу.

- После покупки устанавливаются уровни тейк-профита и стоп-лосса; позиция закрывается только при достижении этих уровней или при появлении противоположного сигнала от Williams %R.

- После продажи устанавливаются уровни тейк-профита и стоп-лосса; позиция закрывается только при достижении этих уровней или при появлении противоположного сигнала от Williams %R.

- Возможна торговля только в заданном временном диапазоне (например, с 9:00 до 11:00) и с ограничением по времени около часа (X минут до и Y минут после).

- Можно выбрать направление торговли: только лонг, только шорт или обе стороны.

Анализ преимуществ

- Динамический тейк-профит и стоп-лосс: уровни корректируются согласно настройкам пользователя, что позволяет лучше защищать прибыль и контролировать риски.

- Гибкие параметры: пользователь может настроить различные параметры (период индикатора, уровни TP/SL, время торговли и т.д.) в соответствии со своими предпочтениями и рыночными условиями.

- Сглаживание индикатора: использование EMA для сглаживания Williams %R снижает шум и повышает надёжность сигналов.

- Ограничение времени торговли: возможность торговать только в определённые часы, избегая периодов высокой волатильности и снижая риски.

- Настраиваемое направление: в зависимости от рыночного тренда и личных суждений можно выбрать только лонг, только шорт или обе стороны.

Анализ рисков

- Неправильная настройка параметров: слишком широкие или слишком узкие уровни TP/SL могут привести к потере прибыли или частым срабатываниям стоп-лосса.

- Ошибки в определении тренда: индикатор Williams %R показывает слабые результаты на боковом рынке, возможны ложные сигналы.

- Ограниченная эффективность временных рамок: ограничение времени торговли может привести к пропуску хороших возможностей.

- Чрезмерная оптимизация: переоптимизация параметров может привести к плохим результатам при реальной торговле в будущем.

Направления оптимизации

- Комбинирование с другими индикаторами: например, с трендовыми индикаторами или индикаторами волатильности для повышения точности подтверждения сигналов.

- Динамическая оптимизация параметров: корректировка параметров в реальном времени в зависимости от рыночных условий, например, использование разных настроек для трендового и бокового рынка.

- Улучшение методов TP/SL: применение трейлинг-стопа, частичного тейк-профита и т.д. для лучшей защиты прибыли и контроля рисков.

- Добавление управления капиталом: динамическое изменение размера позиции в зависимости от баланса счёта и склонности к риску.

Заключение

Стратегия динамической корректировки тейк-профита и стоп-лосса на основе Williams %R позволяет простым и эффективным способом выявлять состояния перекупленности и перепроданности, предлагая при этом гибкие настройки для адаптации к различным рыночным условиям и торговым стилям. Динамическое изменение уровней TP/SL позволяет лучше контролировать риски и защищать прибыль. Однако на практике необходимо учитывать такие факторы, как настройка параметров, подтверждение сигналов и выбор времени торговли, чтобы дополнительно повысить устойчивость и доходность стратегии.

- 1