Скользящая средняя, простая скользящая средняя, наклон скользящей средней, трейлинг-стоп, повторный вход

Обзор

Данная стратегия принимает торговые решения на основе наклона скользящей средней (MA) и относительного положения цены относительно MA. Когда наклон MA превышает минимальный порог наклона, а цена находится выше MA, стратегия совершает покупку. При этом стратегия использует трейлинг-стоп (Trailing Stop Loss) для управления рисками и повторно входит в рынок (Re-Entry) при определенных условиях. Стратегия направлена на捕捉 возможностей в восходящем тренде, одновременно оптимизируя доходность и риск с помощью динамического стоп-лосса и механизма повторного входа.

Принцип стратегии

- Рассчитывается простая скользящая средняя (SMA) за указанный период в качестве основного индикатора тренда.

- Вычисляется наклон SMA за указанный период окна для оценки силы текущего тренда.

- Когда наклон SMA превышает минимальный порог наклона и цена находится выше SMA, считается, что рынок находится в восходящем тренде, и стратегия совершает покупку.

- После входа стратегия использует механизм трейлинг-стопа, динамически корректируя уровень стоп-лосса на основе текущей цены и указанного процента.

- Если цена достигает уровня трейлинг-стопа, стратегия закрывает позицию и отмечает срабатывание стоп-лосса.

- После срабатывания стоп-лосса, если цена откатывается ниже SMA на определенный процент, стратегия повторно входит в рынок.

- Если цена опускается ниже SMA, стратегия немедленно закрывает позицию.

Анализ преимуществ

- Следование за трендом: оценка тренда по наклону SMA и относительному положению цены относительно SMA помогает стратегии получать прибыль на восходящих трендах.

- Динамический стоп-лосс: использование механизма трейлинг-стопа, корректирующего уровень стоп-лосса в зависимости от изменения цены, позволяет лучше защитить прибыль и ограничить убытки.

- Повторный вход: после срабатывания стоп-лосса стратегия повторно входит в рынок при откате цены ниже SMA на определенный процент, чтобы уловить потенциальные отскоки.

- Гибкость параметров: стратегия предлагает несколько настраиваемых параметров, таких как период SMA, минимальный порог наклона, процент трейлинг-стопа и т.д., которые можно оптимизировать под разные рыночные условия.

Анализ рисков

- Чувствительность к параметрам: эффективность стратегии может быть чувствительна к настройкам параметров; неправильный выбор может привести к плохим результатам.

- Идентификация тренда: стратегия в основном полагается на наклон SMA и относительное положение цены для определения тренда, что при определенных рыночных условиях может давать ложные сигналы.

- Частота стоп-лоссов: механизм трейлинг-стопа может приводить к частым срабатываниям стоп-лоссов, особенно в условиях высокой волатильности, что влияет на общую производительность стратегии.

- Риск повторного входа: механизм повторного входа в некоторых случаях может привести к тому, что стратегия снова войдет в рынок и столкнется с дальнейшим падением, увеличивая убытки.

Направления оптимизации

- Подтверждение тренда: при оценке тренда можно комбинировать другие технические индикаторы или модели поведения цены для повышения точности идентификации тренда.

- Оптимизация стоп-лосса: можно исследовать другие методы стоп-лосса, например, на основе волатильности или уровней поддержки/сопротивления, чтобы лучше адаптироваться к различным рыночным условиям.

- Условия повторного входа: можно оптимизировать условия повторного входа, например, учитывать величину отката цены, временной промежуток и другие факторы, чтобы отсеять неблагоприятные сигналы повторного входа.

- Управление размером позиции: внедрение механизма управления размером позиции, корректирующего объем каждой сделки в зависимости от рыночной волатильности или других показателей риска для контроля общего уровня риска.

Заключение

Данная стратегия определяет тренд на основе наклона скользящей средней и относительного положения цены относительно скользящей средней, а также использует трейлинг-стоп и механизм условного повторного входа для управления торговлей. Преимущества стратегии заключаются в способности следовать за трендом, динамической защите стоп-лоссом и улавливании возможностей повторного входа. Однако стратегия также имеет потенциальные проблемы, такие как чувствительность к параметрам, ошибки идентификации тренда, частота стоп-лоссов и риск повторного входа. В соответствии с направлениями оптимизации, такими как улучшение идентификации тренда, методов стоп-лосса, условий повторного входа и управления размером позиции, можно скорректировать недостатки стратегии. При практическом применении необходимо тщательно оценивать и адаптировать стратегию в соответствии с конкретными рыночными характеристиками и торговым стилем.

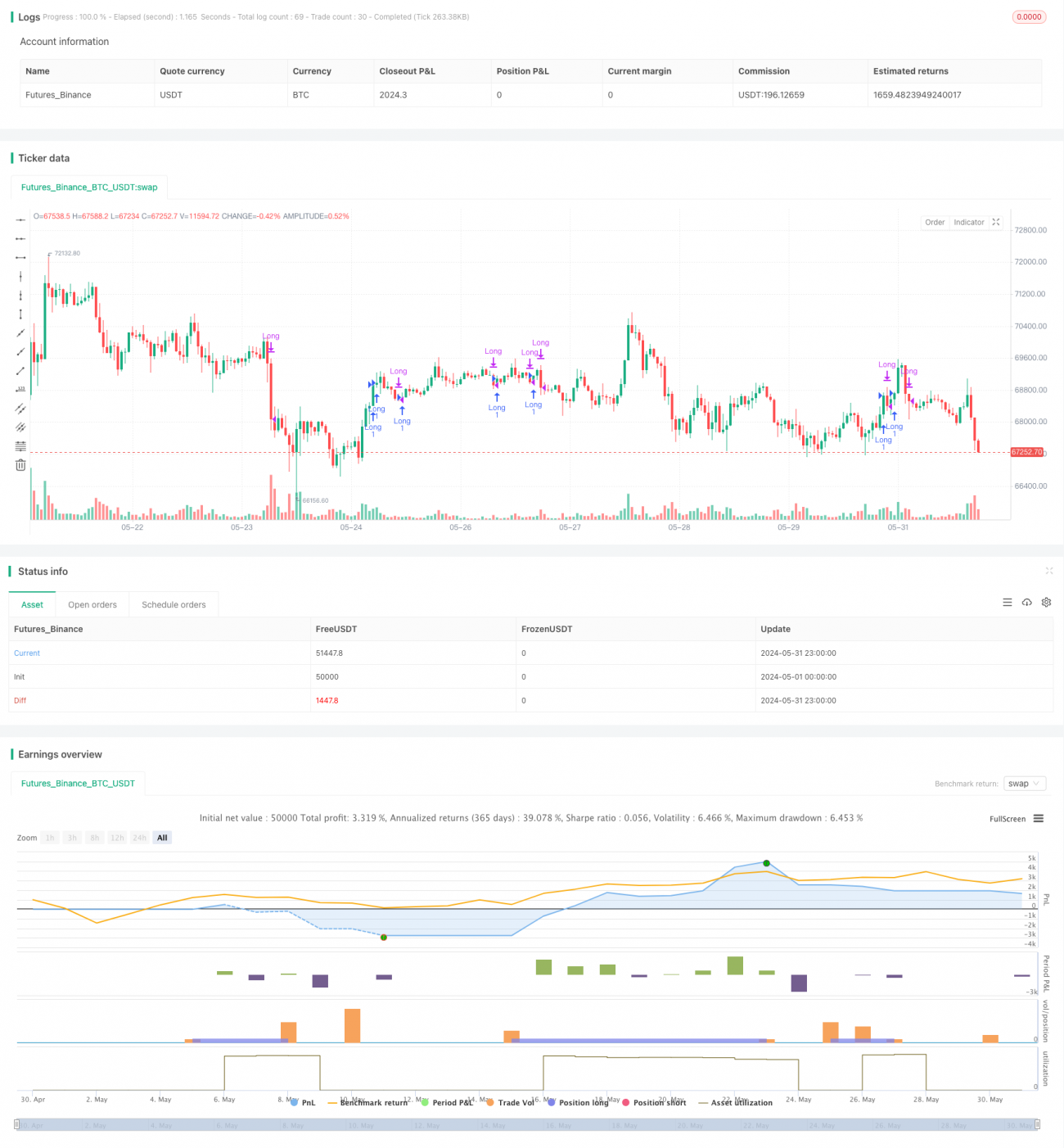

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("MA Incline Strategy with Trailing Stop-Loss and Conditional Re-Entry", overlay=true, calc_on_every_tick=true)

// Input parameters- 1