Стратегия возврата к среднему

Обзор

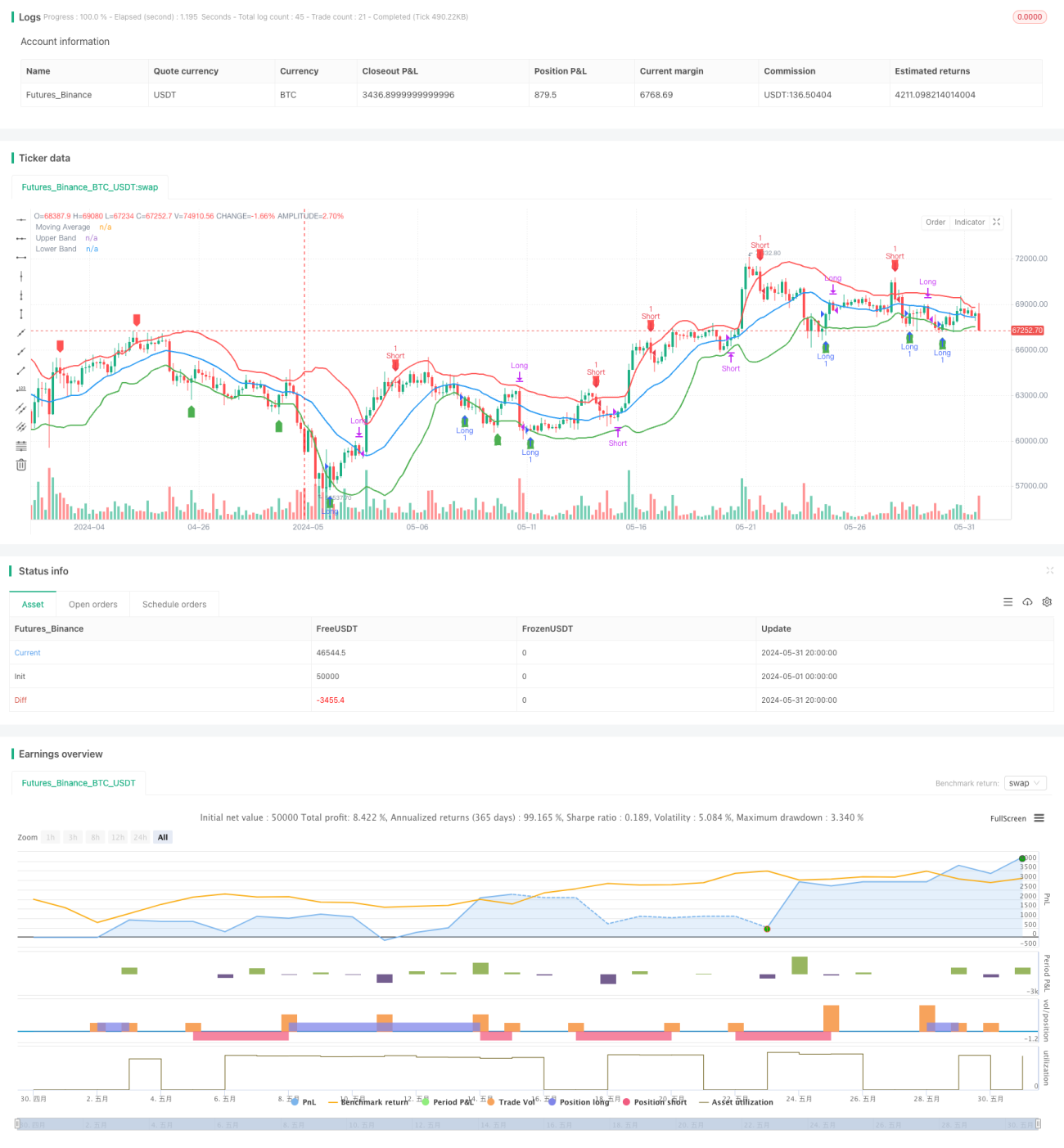

Данная стратегия основана на принципе возврата к среднему (mean reversion) и использует отклонение цены от скользящей средней для принятия торговых решений. Когда цена отклоняется вверх от верхней полосы, открывается короткая позиция; при отклонении вниз от нижней полосы – длинная позиция. Когда цена возвращается к скользящей средней, позиция закрывается. Ключевая идея стратегии заключается в предположении, что цена всегда стремится вернуться к среднему уровню.

Принцип стратегии

- Рассчитывается простая скользящая средняя (SMA) за указанный период (по умолчанию 20) как средний уровень цены.

- Вычисляется стандартное отклонение цены (DEV), на основе которого строятся верхняя и нижняя полосы. Верхняя полоса равна SMA плюс произведение стандартного отклонения на коэффициент (по умолчанию 1,5), нижняя полоса – SMA минус произведение стандартного отклонения на коэффициент.

- Когда цена пробивает верхнюю полосу вверх, открывается короткая позиция; когда пробивает нижнюю полосу вниз – длинная позиция.

- При движении цены вниз через SMA (для длинной позиции) длинная позиция закрывается; при движении цены вверх через SMA (для короткой позиции) короткая позиция закрывается.

- На графике отмечаются скользящая средняя, верхняя и нижняя полосы, а также сигналы покупки и продажи.

Анализ преимуществ

- Стратегия возврата к среднему основана на статистическом принципе, согласно которому цена всегда стремится вернуться к среднему значению, что в долгосрочной перспективе обеспечивает определённую вероятность получения прибыли.

- Наличие верхней и нижней полос даёт чёткие точки входа и выхода, что облегчает исполнение и управление.

- Логика стратегии проста и понятна, легко поддаётся пониманию и реализации.

- Подходит для инструментов и таймфреймов, где явно выражен возврат к среднему.

Анализ рисков

- При изменении рыночного тренда цена может долгое время отклоняться от среднего значения, не возвращаясь к нему, что приводит к неэффективности стратегии.

- Неправильный выбор множителя стандартного отклонения может привести к слишком высокой или низкой частоте сделок, что повлияет на доходность.

- В экстремальных рыночных условиях волатильность цены резко возрастает, и верхняя/нижняя полосы могут потерять свою эффективность.

- Если инструмент или таймфрейм не обладает свойством возврата к среднему, стратегия может быть убыточной.

Направления оптимизации

- Провести оптимизацию периода SMA и множителя стандартного отклонения для поиска наилучших параметров.

- Ввести индикаторы определения тренда, чтобы избегать контртрендовых сделок при явном тренде.

- Добавить индикаторы волатильности, такие как ATR, для построения динамических полос наряду со стандартным отклонением.

- Учесть торговые издержки, такие как проскальзывание и комиссии, для обеспечения реалистичности бэктестирования.

- Внедрить модуль управления рисками, например стоп-лосс, тейк-профит, управление позицией.

Заключение

Стратегия возврата к среднему – это количественная торговая стратегия, основанная на статистических принципах. Она использует построение верхней и нижней полос вокруг среднего уровня цены для принятия торговых решений. Логика стратегии проста, а исполнение – чётко. Однако необходимо уделять внимание выбору инструментов и оптимизации параметров. В практическом применении также следует учитывать такие факторы, как тренд, торговые издержки и управление рисками, чтобы повысить устойчивость и прибыльность стратегии. В целом, стратегия возврата к среднему является распространённой и заслуживающей углублённого изучения концепцией в области количественной торговли.

- 1