Многоуровневая RSI-регрессионная торговая стратегия с динамической корректировкой волатильности

Обзор

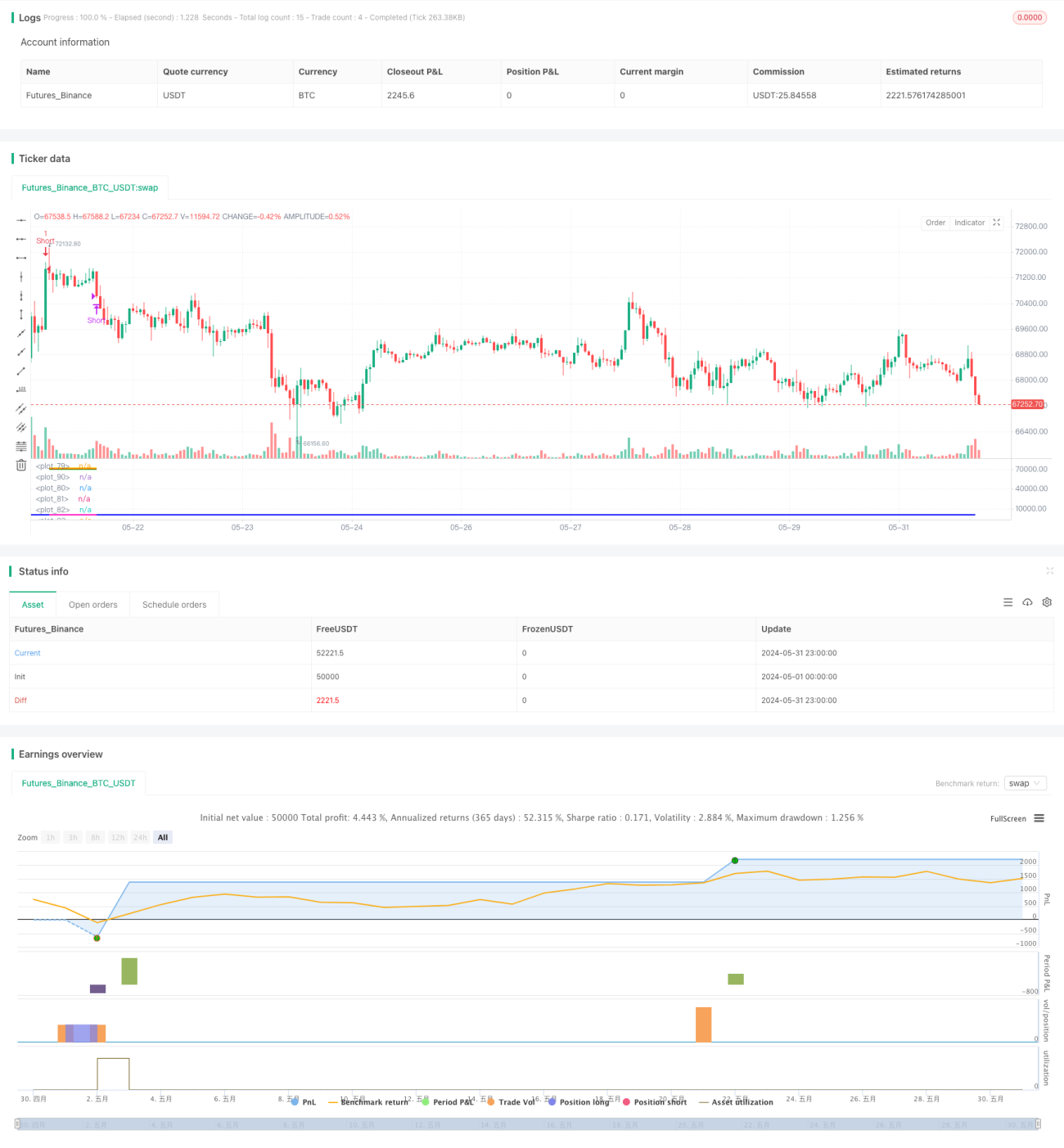

Данная стратегия представляет собой многоуровневую торговую систему, основанную на индикаторе RSI и волатильности цен. Она использует экстремальные значения RSI и аномально большие ценовые движения в качестве сигналов для входа, одновременно применяя пирамидальное наращивание позиции и динамическое фиксирование прибыли для управления рисками и оптимизации доходности. Основная идея стратегии — входить в рынок при экстремальных колебаниях и фиксировать прибыль при возврате цены к нормальным уровням.

Принцип стратегии

-

Условия входа:

- Используется 20-периодный RSI (RSI20) в качестве основного индикатора.

- Устанавливаются несколько порогов RSI (35/65, 30/70, 25/75, 20/80) и соответствующие пороги волатильности.

- Когда RSI достигает определённого порога, а размер тела текущей свечи превышает соответствующий порог волатильности, генерируется сигнал на вход.

- Дополнительное условие: цена должна пробить недавний максимум/минимум (уровень поддержки/сопротивления) на определённый процент.

-

Механизм наращивания позиции:

- Допускается максимум 5 входов (первоначальный вход + 4 наращивания).

- Каждое последующее наращивание должно удовлетворять более строгим условиям по RSI и волатильности.

-

Механизм выхода:

- Устанавливаются 5 различных уровней фиксации прибыли.

- Уровни фиксации прибыли динамически рассчитываются на основе уровней поддержки/сопротивления при входе.

- С увеличением количества удерживаемых позиций целевая прибыль постепенно снижается.

-

Управление рисками:

- Используется процентная модель риска: каждый раз риск фиксируется на уровне 20% от общего капитала счёта.

- Устанавливается максимальное количество одновременно открытых позиций — 5, что ограничивает общий риск-экспозицию.

Преимущества стратегии

-

Многоуровневый вход: За счёт нескольких порогов RSI и волатильности стратегия может улавливать различные степени экстремальных ситуаций на рынке, увеличивая число торговых возможностей.

-

Динамическое фиксирование прибыли: Уровни фиксации прибыли, рассчитанные на основе поддержки/сопротивления, адаптируются к рыночной структуре, что позволяет защищать прибыль, не выходя из позиции слишком рано.

-

Пирамидальное наращивание: При продолжении тренда наращивание позиции значительно повышает потенциал прибыли.

-

Управление рисками: Фиксированный процент риска и ограничение на максимальное количество позиций позволяют эффективно контролировать риск по каждой сделке и общий риск.

-

Гибкость: Большое количество настраиваемых параметров позволяет адаптировать стратегию к различным рыночным условиям и торговым инструментам.

-

Mean reversion + трендовое следование: Сочетание преимуществ обоих подходов позволяет как ловить краткосрочные развороты, так и не упускать крупные тренды.

Риски стратегии

-

Чрезмерная торговля: На высоковолатильных рынках сигналы могут генерироваться слишком часто, что приводит к высоким комиссиям.

-

Ложные пробои: Рынок может показать кратковременное экстремальное движение, за которым следует быстрый откат, вызывая ложные сигналы.

-

Последовательные убытки: При непрерывном движении рынка в одном направлении многократное наращивание позиции может привести к значительным убыткам.

-

Чувствительность к параметрам: Результаты стратегии могут сильно зависеть от настроек параметров, создавая риск переобучения.

-

Влияние проскальзывания: В периоды резких колебаний возможно значительное проскальзывание, ухудшающее результаты стратегии.

-

Зависимость от рыночных условий: Стратегия может показывать слабые результаты в определённых рыночных условиях, например, при низкой волатильности или сильном тренде.

Направления оптимизации стратегии

-

Динамическая настройка параметров: Внедрение адаптивных механизмов для изменения порогов RSI и волатильности в зависимости от состояния рынка.

-

Мультитаймфреймовый анализ: Учёт долгосрочных трендов для улучшения качества входов.

-

Оптимизация стоп-лоссов: Добавление трейлинг-стопа или динамического стопа на основе ATR для дальнейшего контроля рисков.

-

Фильтрация состояний рынка: Включение фильтров по силе тренда, циклам волатильности и т.п., чтобы избегать торговли в неподходящих условиях.

-

Оптимизация управления капиталом: Более детальное распределение размера позиции, например, с учётом уровня сигнала.

-

Интеграция машинного обучения: Использование алгоритмов машинного обучения для оптимизации выбора параметров и генерации сигналов.

-

Корреляционный анализ: Добавление анализа корреляции с другими активами для повышения стабильности и диверсификации стратегии.

Заключение

Данная многоуровневая стратегия mean reversion на основе RSI представляет собой тщательно разработанную количественную торговую систему, умело сочетающую технический анализ, динамическое управление рисками и пирамидальное наращивание позиции. Улавливая экстремальные колебания рынка и фиксируя прибыль при возврате цены, стратегия демонстрирует высокий потенциал прибыльности. Однако она сталкивается с такими вызовами, как чрезмерная торговля и зависимость от рыночных условий. Будущие направления оптимизации должны быть сосредоточены на повышении адаптивности и способности контролировать риски, чтобы соответствовать различным рыночным средам. В целом, это хорошо проработанная основа стратегии, которая при дальнейшей оптимизации и бэктестинге может превратиться в устойчивую торговую систему.

- 1