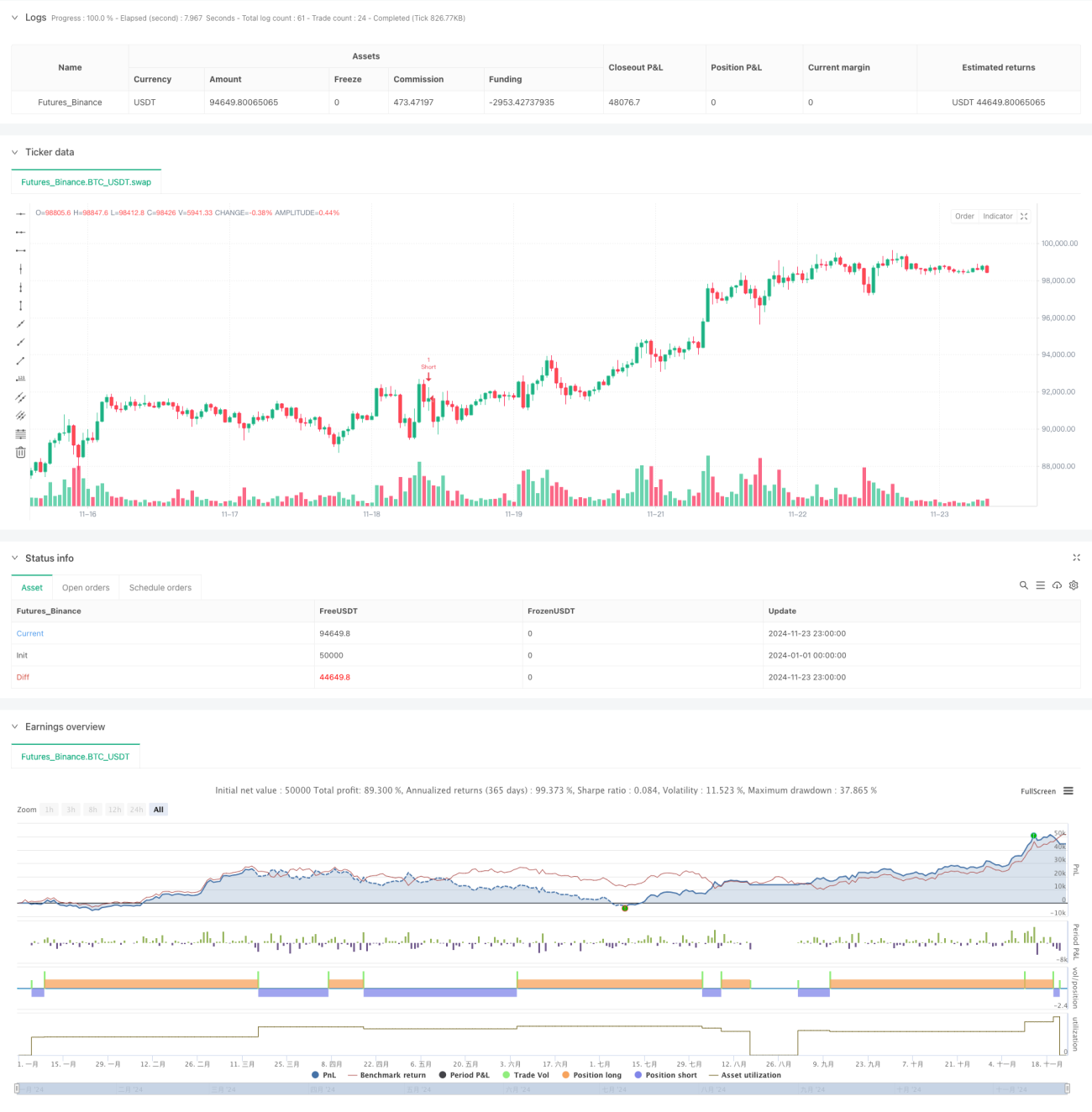

Стратегия следования за прорывом ценового действия на основе двойного MACD

Обзор

Это торговая стратегия, сочетающая двойной индикатор MACD и анализ ценового действия. Стратегия определяет рыночный тренд, наблюдая за изменением цвета гистограммы двойного MACD на 15-минутном таймфрейме, одновременно ищет сильные свечные паттерны на 5-минутном графике и подтверждает сигналы пробоя на 1-минутном таймфрейме. В стратегии используются динамический стоп-лосс на основе ATR и механизм трейлинг-тейк-профита, что позволяет эффективно управлять рисками и одновременно максимизировать прибыль.

Принцип стратегии

Стратегия использует две группы MACD с разными параметрами (34/144/9 и 100/200/50) для подтверждения рыночного тренда. Когда обе гистограммы MACD показывают одинаковый цветовой тренд, система ищет на 5-минутном графике сильные свечные паттерны, характеризующиеся тем, что тело свечи как минимум в 1,5 раза больше её тени. После обнаружения сильного свечного паттерна система на 1-минутном графике отслеживает возникновение пробоя. При пробое максимума в восходящем тренде или минимума в нисходящем тренде открывается позиция. Стоп-лосс устанавливается на основе ATR, а в качестве динамического трейлинг-тейк-профита используется значение ATR, умноженное на 1,5.

Преимущества стратегии

- Мультитаймфреймовый анализ: объединение трёх таймфреймов (15 минут, 5 минут и 1 минута) повышает надёжность сигналов.

- Подтверждение тренда: двойной MACD обеспечивает перекрёстную верификацию, снижая количество ложных сигналов.

- Анализ ценового действия: выявление ключевых ценовых уровней с помощью сильных свечных паттернов.

- Динамическое управление рисками: адаптивный стоп-лосс и механизм трейлинг-тейк-профита на основе ATR.

- Фильтрация сигналов: строгие условия входа сокращают число ошибочных сделок.

- Высокая степень автоматизации: полностью автоматическая торговля с минимальным участием человека.

Риски стратегии

- Риск разворота тренда: возможны ложные пробои на резко волатильных рынках.

- Риск проскальзывания: высокочастотная торговля на 1-минутном таймфрейме может привести к проскальзыванию.

- Риск излишней активности: частые сигналы могут спровоцировать чрезмерное количество сделок.

- Зависимость от рыночных условий: стратегия может показывать плохие результаты на боковых рынках.

Меры по снижению рисков:

- Добавление фильтра тренда.

- Установка минимального порога волатильности.

- Ограничение количества сделок.

- Внедрение механизма распознавания рыночных условий.

Направления оптимизации стратегии

- Оптимизация параметров MACD: возможность настройки параметров MACD под различные рыночные особенности.

- Оптимизация стоп-лосса: рассмотреть возможность добавления динамического стоп-лосса на основе волатильности.

- Фильтрация по времени торговли: добавить ограничения по временным окнам.

- Управление позицией: реализовать механизм частичного входа и выхода.

- Фильтрация рыночных условий: добавить индикатор силы тренда.

- Контроль просадок: внедрить механизм управления рисками на основе кривой капитала.

Заключение

Это торговая система, комплексно использующая технический анализ и управление рисками. Качество сделок обеспечивается за счёт мультитаймфреймового анализа и строгой фильтрации сигналов, а эффективное управление рисками достигается с помощью динамического стоп-лосса и трейлинг-тейк-профита. Стратегия обладает высокой адаптивностью, но требует постоянной доработки в зависимости от рыночных условий. Перед применением на реальном счёте рекомендуется провести тщательное бэктестирование и оптимизацию параметров, а также внести соответствующие корректировки с учётом особенностей рынка.

- 1