Стратегия ложного пробоя уровня поддержки множественных скользящих средних с системой стоп-лосс на основе ATR

Обзор

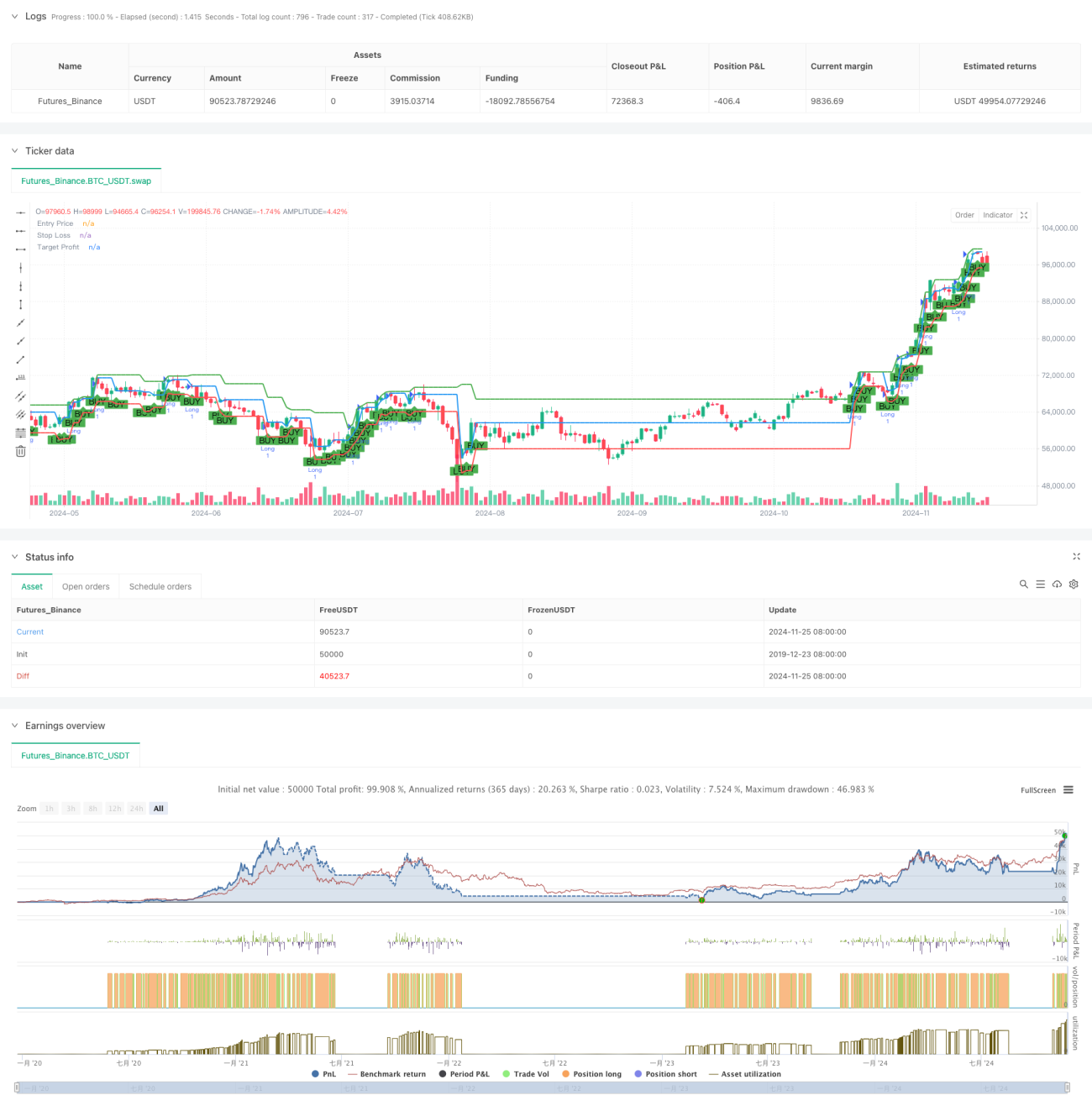

Данная стратегия представляет собой торговую систему, основанную на определении тренда с помощью скользящих средних и ложного пробоя уровней поддержки. Стратегия использует 50-периодную и 200-периодную простые скользящие средние для определения рыночного тренда, формирует торговые сигналы на основе паттерна ложного пробоя уровня поддержки, динамически устанавливает стоп-лосс с помощью индикатора ATR (средний истинный диапазон) и задаёт цель по прибыли на уровне точки пробоя. Данная стратегия полностью использует трендовые характеристики рынка и закономерности движения цены, получая прибыль за счёт ловли откатов после ложных пробоев.

Принцип стратегии

Основная логика стратегии включает следующие ключевые элементы:

- Определение тренда: Используется взаимное расположение 50-периодной и 200-периодной скользящих средних для оценки рыночного тренда. Когда краткосрочная средняя находится выше долгосрочной, подтверждается восходящий тренд.

- Расчёт уровня поддержки: Уровень поддержки рассчитывается по формуле точки разворота (Pivot Point), используя взвешенное среднее максимума, минимума и цены закрытия предыдущего периода.

- Подтверждение ложного пробоя: Когда цена в восходящем тренде кратковременно пробивает уровень поддержки вниз, а затем закрывается выше него, формируется сигнал на покупку (лонг).

- Управление рисками: Используется 14-периодный ATR для расчёта динамического уровня стоп-лосса, что обеспечивает расширение диапазона стопа при усилении волатильности рынка.

- Цель по прибыли: В качестве цели по прибыли используется максимум за предыдущие 10 периодов, что обеспечивает достаточное пространство для получения прибыли.

Преимущества стратегии

- Следование за трендом: Стратегия гарантирует торговлю в направлении основного тренда через систему скользящих средних, повышая процент выигрышных сделок.

- Динамический контроль рисков: Использование ATR для динамической корректировки уровня стоп-лосса позволяет адаптироваться к различным рыночным условиям.

- Чёткие торговые сигналы: Паттерн ложного пробоя уровня поддержки имеет ясные критерии, что снижает субъективность в принятии решений.

- Разумное соотношение риска и прибыли: Установка динамического стоп-лосса и цели по прибыли на основе исторических максимумов обеспечивает благоприятное соотношение риска и доходности.

- Систематизация операций: Логика стратегии прозрачна, что упрощает её программную реализацию и тестирование на исторических данных.

Риски стратегии

- Риск ложных сигналов: В боковом рынке (флэте) может возникать множество ложных пробоев, что увеличивает торговые издержки.

- Риск разворота тренда: Система скользящих средних реагирует с запаздыванием на точки разворота тренда, что может привести к задержке входа в позицию.

- Риск величины стоп-лосса: Стоп-лосс на основе ATR при резком расширении волатильности может привести к значительным потерям.

- Риск установки цели по прибыли: Фиксированный период для определения исторического максимума может неточно отражать текущую рыночную ситуацию.

Направления оптимизации стратегии

- Добавление фильтров: Можно добавить подтверждение по объёму торгов для повышения надёжности сигналов.

- Оптимизация параметров скользящих средних: Корректировка периодов скользящих средних в зависимости от характеристик рынка для повышения точности определения тренда.

- Улучшение метода стоп-лосса: Возможно использование комбинированного стопа на основе уровней поддержки для повышения эффективности.

- Динамическая цель по прибыли: Ввести динамический метод расчёта цели по прибыли для лучшей адаптации к изменениям рынка.

- Добавление временного фильтра: Ввести фильтр по временному окну торговли, чтобы избегать неблагоприятных периодов.

Заключение

Стратегия на основе ложного пробоя уровней поддержки с множественными скользящими средними представляет собой целостную торговую систему, объединяющую следование за трендом и ценовые паттерны. Используя определение тренда с помощью скользящих средних и идентификацию паттерна ложного пробоя поддержки в сочетании с динамическим стоп-лоссом на основе ATR, она формирует контролируемую по рискам торговую стратегию. Основное преимущество стратегии заключается в систематизированном процессе операций и чётком подходе к управлению рисками. Путём постоянной оптимизации и доработки стратегия может лучше адаптироваться к различным рыночным условиям и повысить эффективность торговли. При практическом применении инвесторам рекомендуется настраивать параметры стратегии с учётом собственной толерантности к риску и особенностей рынка.

- 1