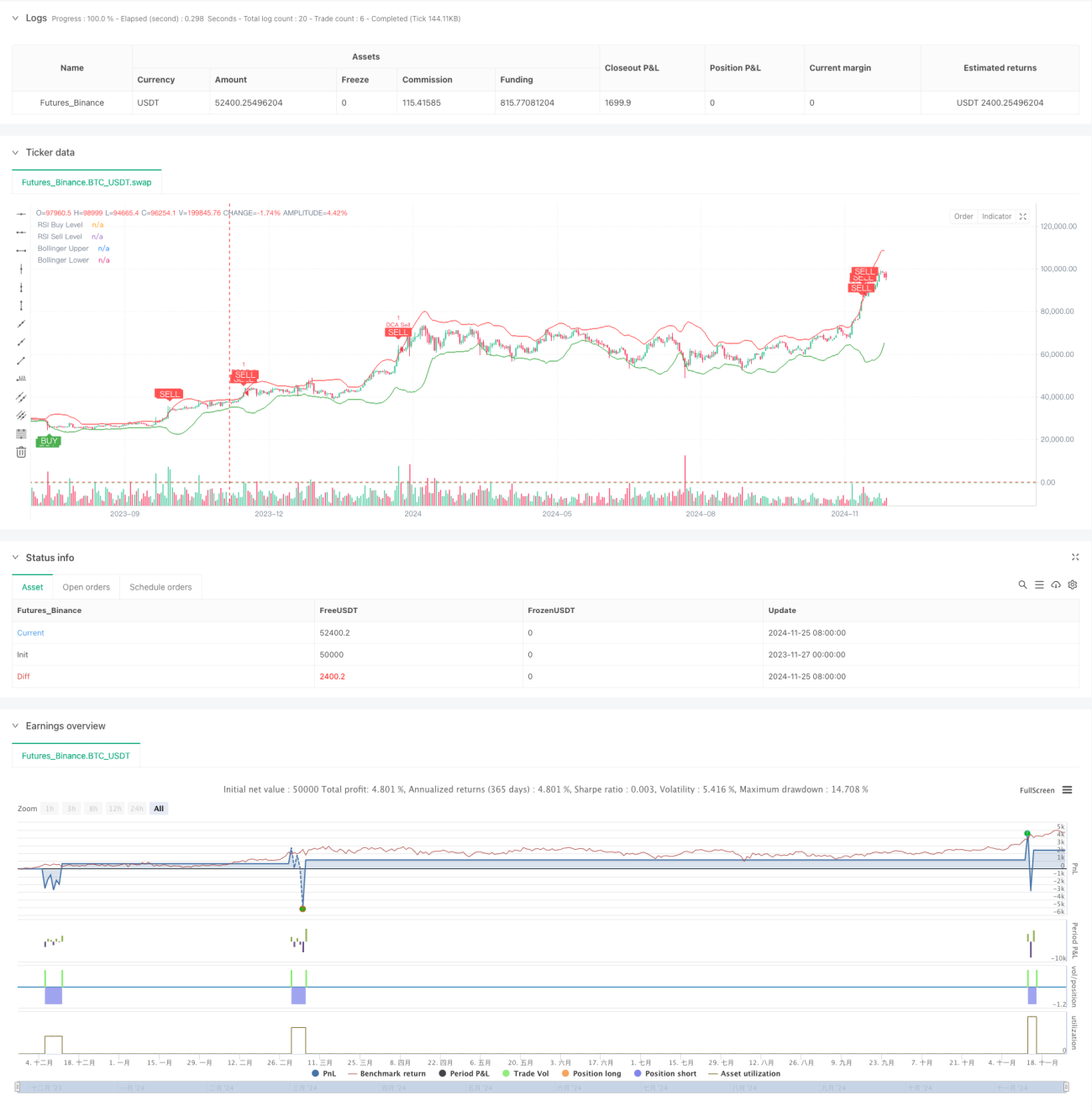

Обзор

Данная стратегия представляет собой систему количественной торговли, которая объединяет полосы Боллинджера (Bollinger Bands), индекс относительной силы (RSI) и метод динамического усреднения стоимости (DCA). Стратегия использует правила управления капиталом для автоматического выполнения поэтапного открытия позиций в условиях рыночной волатильности, одновременно применяя технические индикаторы для генерации сигналов покупки и продажи, что позволяет осуществлять торговлю с контролируемым риском. Система также включает логику фиксации прибыли и отслеживания суммарной прибыли, что позволяет эффективно контролировать и оценивать торговые результаты.

Принцип стратегии

Стратегия работает на основе следующих ключевых компонентов:

- Полосы Боллинджера используются для определения ценовых диапазонов: когда цена касается нижней полосы, рассматривается покупка, при касании верхней полосы — продажа.

- Индекс RSI подтверждает состояния перекупленности и перепроданности на рынке: RSI ниже 25 указывает на перепроданность, выше 75 — на перекупленность.

- Модуль DCA динамически рассчитывает сумму для каждого пополнения позиции на основе собственного капитала счета, обеспечивая адаптивное управление капиталом.

- Модуль фиксации прибыли устанавливает целевую прибыль в 5% — при её достижении позиция автоматически закрывается для защиты прибыли.

- Модуль мониторинга рыночного состояния рассчитывает амплитуду изменений рынка за 90 дней, помогая оценить общий тренд.

- Модуль отслеживания суммарной прибыли фиксирует прибыль или убыток каждой сделки для удобства оценки эффективности стратегии.

Преимущества стратегии

- Комбинация нескольких технических индикаторов с перекрестной верификацией повышает надёжность сигналов.

- Использование динамического управления позицией позволяет избежать рисков, связанных с фиксированным размером позиции.

- Установка разумного уровня фиксации прибыли позволяет своевременно зафиксировать прибыль.

- Наличие функции мониторинга рыночных трендов облегчает понимание общей ситуации.

- Полноценная система отслеживания прибыли упрощает анализ эффективности стратегии.

- Хорошо настроенные оповещения позволяют своевременно получать уведомления о торговых возможностях.

Риски стратегии

- На колеблющемся рынке сигналы могут генерироваться слишком часто, что приведёт к увеличению торговых издержек.

- В трендовом рынке индикатор RSI может давать запаздывающие сигналы.

- Фиксированный процент фиксации прибыли может привести к преждевременному выходу из позиции на сильном тренде.

- Стратегия DCA может привести к значительным просадкам при однонаправленном падении рынка.

Рекомендуется принять следующие меры для управления рисками:

- Установить максимальный лимит на количество открытых позиций.

- Динамически корректировать параметры в зависимости от рыночной волатильности.

- Добавить фильтр тренда.

- Применить многоуровневую стратегию фиксации прибыли.

Направления оптимизации стратегии

- Динамическая оптимизация параметров:

- Параметры полос Боллинджера можно адаптивно настраивать в зависимости от волатильности.

- Пороги RSI могут изменяться в зависимости от рыночного цикла.

- Доля капитала для DCA может корректироваться в соответствии с размером счета.

- Улучшение системы сигналов:

- Добавить подтверждение по объёму.

- Включить анализ трендовых линий.

- Комбинировать больше технических индикаторов для перекрестной верификации.

- Совершенствование контроля рисков:

- Реализовать динамический стоп-лосс.

- Добавить контроль максимальной просадки.

- Установить дневной лимит убытков.

Заключение

Данная стратегия формирует относительно полную торговую систему за счёт интеграции технического анализа и методов управления капиталом. Её преимущество заключается в множественной верификации сигналов и всестороннем управлении рисками, однако она требует тщательного тестирования и оптимизации в реальной торговле. Постоянное совершенствование настроек параметров и добавление вспомогательных индикаторов позволит стратегии достигать стабильных результатов в практической торговле.

/*backtest

start: 2023-11-27 00:00:00

end: 2024-11-26 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Combined BB RSI with Cumulative Profit, Market Change, and Futures Strategy (DCA)", shorttitle="BB RSI Combined DCA Strategy", overlay=true)

// Input Parameters- 1