Обзор

Данная стратегия представляет собой продвинутую торговую систему, основанную на анализе точек разворота (pivot points). Она выявляет ключевые точки перелома на рынке для прогнозирования потенциальных разворотов тренда. Стратегия использует инновационный метод «точки разворота от точек разворота» в сочетании с индикатором волатильности ATR для управления позицией, образуя целостную торговую систему. Стратегия применима на различных рынках и может быть оптимизирована по параметрам с учётом их особенностей.

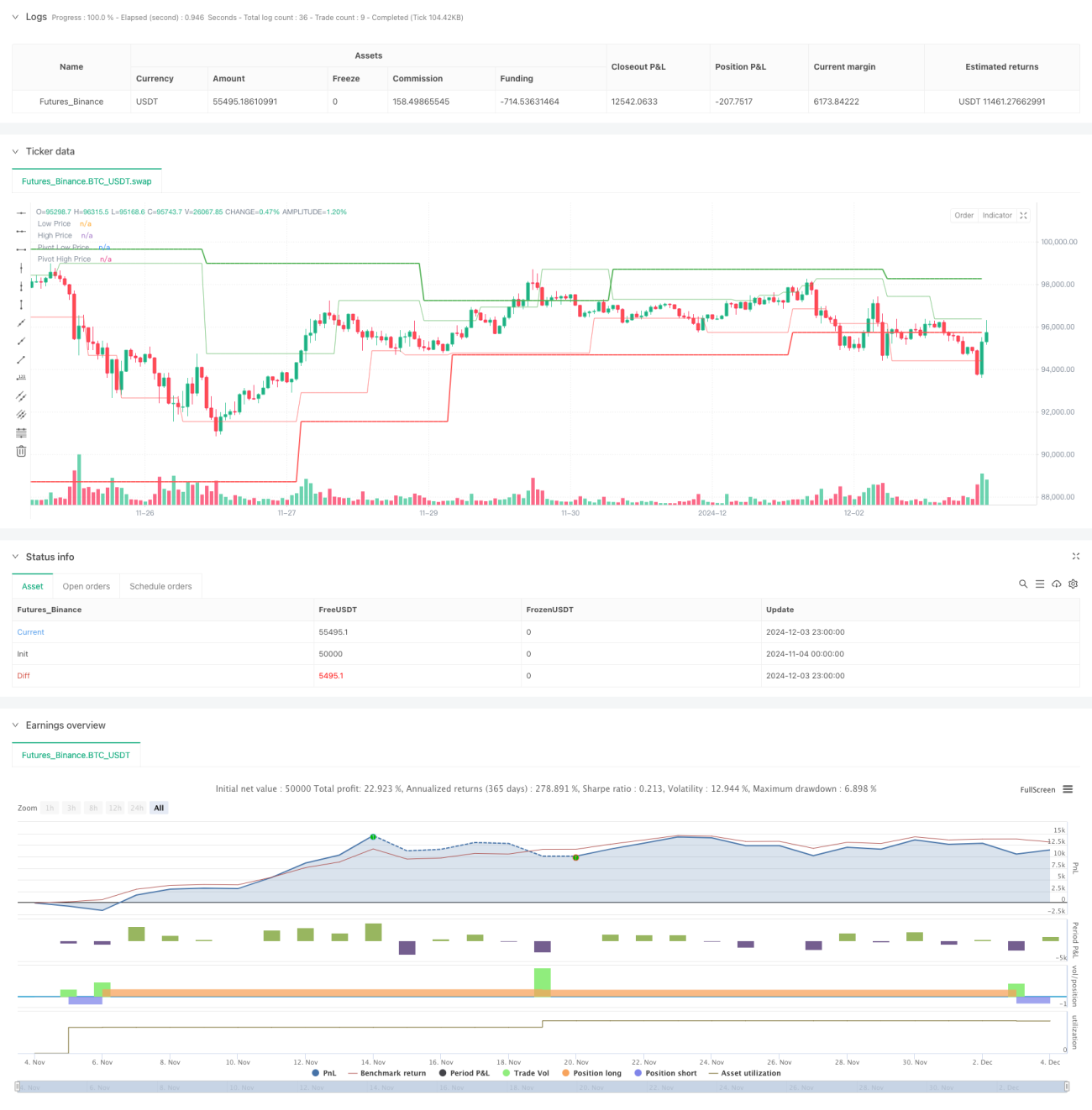

Принцип работы стратегии

Основная идея стратегии заключается в выявлении возможностей разворота рынка с помощью двухуровневого анализа точек разворота. Первый уровень — это базовые максимумы и минимумы. Второй уровень — это значимые точки разворота, отобранные из первого уровня. Когда цена пробивает эти ключевые уровни, система генерирует торговый сигнал. Параллельно стратегия использует индикатор ATR для измерения рыночной волатильности, что помогает определить уровни стоп-лосса, тейк-профита и размер позиции.

Преимущества стратегии

- Высокая адаптивность: стратегия может подстраиваться под различные рыночные условия путём изменения параметров в зависимости от уровня волатильности.

- Надёжное управление рисками: использование ATR для динамической установки стоп-лосса позволяет автоматически корректировать уровень защиты в зависимости от рыночной волатильности.

- Многоуровневое подтверждение: двухуровневый анализ точек разворота снижает риск ложных пробоев.

- Гибкое управление позицией: размер позиции динамически изменяется в зависимости от размера счёта и рыночной волатильности.

- Чёткие правила входа: наличие ясного механизма подтверждения сигналов уменьшает влияние субъективных решений.

Риски стратегии

- Риск проскальзывания: на рынках с высокой волатильностью возможны значительные проскальзывания.

- Риск ложных пробоев: при боковом движении рынка могут возникать ложные сигналы.

- Риск чрезмерного кредитного плеча: неправильное использование кредитного плеча может привести к серьёзным убыткам.

- Риск переоптимизации параметров: чрезмерная оптимизация может привести к переобучению модели.

Направления оптимизации стратегии

- Фильтрация сигналов: можно добавить фильтр по тренду, чтобы торговать только в направлении основного тренда.

- Динамические параметры: автоматическая настройка параметров точек разворота в зависимости от состояния рынка.

- Мультитаймфреймовый анализ: добавление подтверждения с нескольких таймфреймов для повышения точности.

- Умный стоп-лосс: разработка более интеллектуальных стратегий стоп-лосса, например, трейлинг-стоп.

- Контроль рисков: внедрение дополнительных мер контроля рисков, например, анализ корреляции.

Заключение

Это хорошо продуманная торговая стратегия разворота тренда, которая строит надёжную торговую систему на основе двухуровневого анализа точек разворота и управления волатильностью с помощью ATR. Преимущества стратегии — высокая адаптивность и надёжное управление рисками, однако трейдеру необходимо осторожно использовать кредитное плечо и постоянно оптимизировать параметры. Предложенные направления оптимизации позволяют дополнительно улучшить стратегию. Данная стратегия подходит для консервативных трейдеров и представляет собой торговую систему, заслуживающую углублённого изучения и практического применения.

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Pivot of Pivot Reversal Strategy [MAD]", shorttitle="PoP Reversal Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// Inputs with Tooltips- 1