Обзор

Это многоуровневая торговая стратегия, объединяющая вычисление адаптивного среднего истинного диапазона (ATR) и обнаружение тренда на основе импульса. Наиболее примечательной особенностью стратегии является уникальный механизм фиксации прибыли из 7 шагов, который сочетает в себе 4 уровня выхода на основе ATR и 3 уровня фиксированного процента. Такой гибридный подход позволяет трейдерам динамически адаптироваться к рыночной волатильности, систематически получая прибыль как на бычьем, так и на медвежьем рынке. Стратегия предлагает комплексное торговое решение за счёт комбинации динамического расчёта ATR, определения силы тренда и многоступенчатого механизма фиксации прибыли.

Принцип стратегии

Ядро стратегии работает через следующие ключевые компоненты:

- Улучшенный расчёт истинного диапазона: измерение рыночной волатильности с учётом наиболее значительных ценовых движений.

- Интеграция фактора импульса: корректировка ATR на основе недавних ценовых изменений, что делает его более адаптивным.

- Адаптивный расчёт ATR: настройка традиционного ATR в соответствии с фактором импульса, что повышает его чувствительность в периоды колебаний.

- Количественная оценка силы тренда: оценка силы тренда с помощью сложных алгоритмов.

- Семишаговый механизм фиксации прибыли: включает четыре уровня выхода на основе ATR и три уровня фиксированного процента.

Преимущества стратегии

- Адаптивность: подстраивается под различные рыночные условия за счёт динамического расчёта ATR.

- Надёжный риск-менеджмент: многоуровневый механизм фиксации прибыли обеспечивает систематический контроль рисков.

- Высокая гибкость: одинаково эффективна как на бычьем, так и на медвежьем рынке.

- Настраиваемые параметры: предоставляет множество регулируемых параметров для адаптации под разные стили торговли.

- Систематическое исполнение: чёткие правила входа и выхода снижают эмоциональную составляющую торговли.

Риски стратегии

- Чувствительность к параметрам: неправильная настройка параметров может привести к чрезмерной торговле или упущенным возможностям.

- Зависимость от рыночных условий: может показывать низкую эффективность при сильных колебаниях или боковом движении рынка.

- Риск сложности: многоуровневый механизм фиксации прибыли может увеличить сложность исполнения.

- Влияние проскальзывания: множественные точки фиксации прибыли могут существенно пострадать от проскальзывания.

- Требования к управлению капиталом: для исполнения многоуровневой стратегии фиксации прибыли требуется достаточный капитал.

Направления оптимизации стратегии

- Динамическая настройка параметров: автоматическая корректировка параметров в зависимости от рыночной ситуации.

- Фильтрация рыночной среды: добавление механизма распознавания рыночной среды.

- Усиление риск-менеджмента: внедрение динамического стоп-лосса.

- Оптимизация исполнения: упрощение механизма фиксации прибыли для уменьшения влияния проскальзывания.

- Совершенствование фреймворка для бэктестинга: добавление большего количества реалистичных торговых факторов.

Заключение

Данная стратегия предлагает трейдерам комплексную торговую систему за счёт объединения адаптивного ATR и многоуровневого механизма фиксации прибыли. Её преимущество заключается в способности адаптироваться к различным рыночным условиям и одновременно управлять рисками систематическим подходом. Несмотря на некоторые потенциальные риски, при правильной оптимизации и управлении рисками стратегия может стать эффективным торговым инструментом. Её инновационный многоуровневый механизм фиксации прибыли особенно подходит для трейдеров, стремящихся максимизировать прибыль при сохранении контроля над рисками.

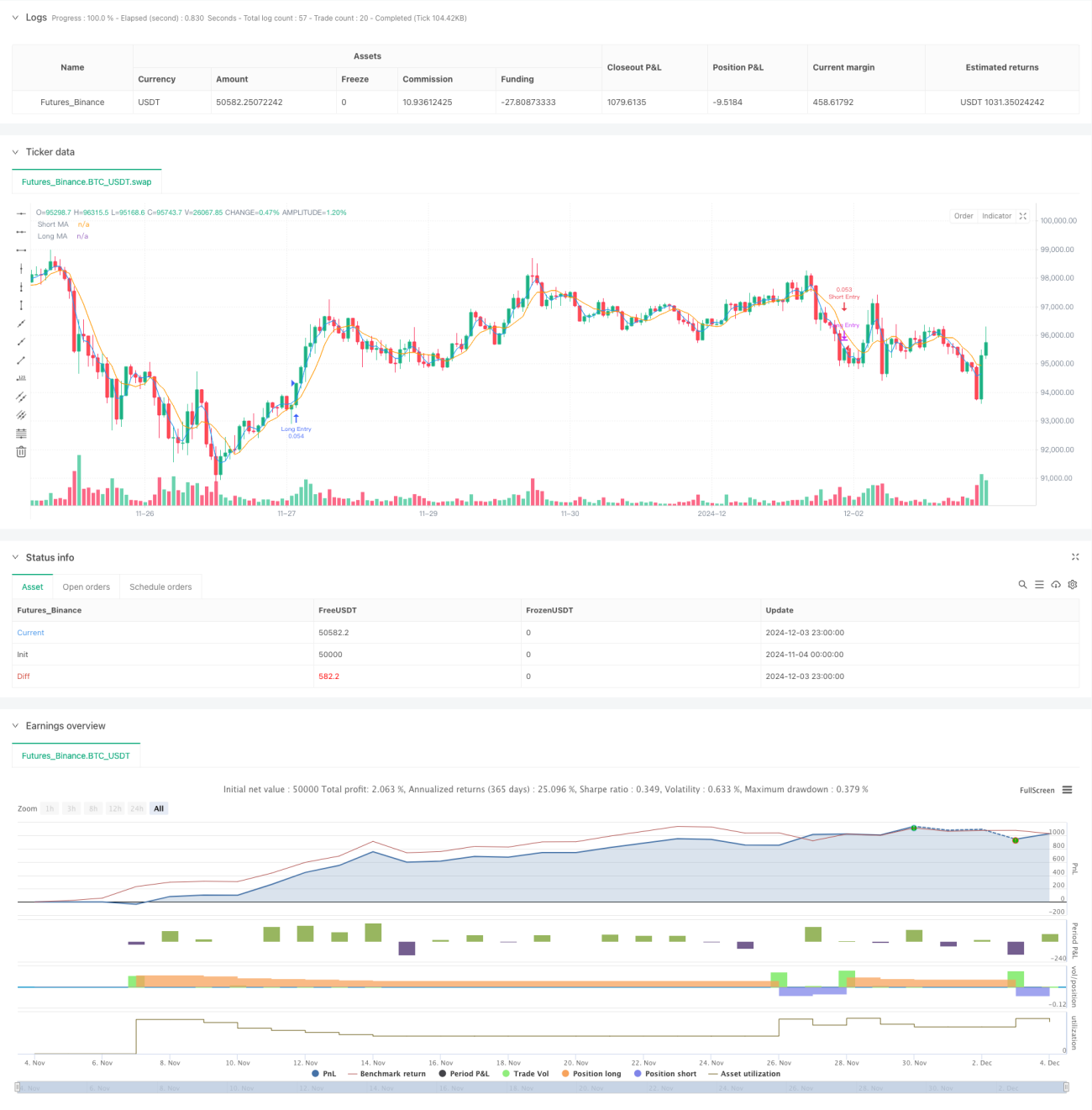

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The SuperATR 7-Step Profit Strategy is a multi-layered trading strategy that combines adaptive ATR and momentum-based trend detection - 1