Продвинутая стратегия динамического трейлинг-стопа и целевой прибыли

Обзор

Данная стратегия представляет собой продвинутую торговую систему, объединяющую динамический трейлинг-стоп, соотношение риска к прибыли и выход по экстремумам RSI. Стратегия идентифицирует специфические рыночные паттерны (параллельные свечные паттерны и свечные паттерны «пинцет») для открытия сделок, одновременно используя ATR и недавние минимумы для установки динамических стоп-лоссов, а также определяет цели по прибыли на основе заданного соотношения риска к доходности. Система также включает механизм оценки перегрева/переохлаждения рынка на основе индикатора RSI, позволяющий своевременно закрывать позиции при достижении экстремальных значений.

Принцип стратегии

Основная логика стратегии включает следующие ключевые части:

- Сигналы на вход основаны на двух паттернах: параллельный свечной паттерн (большая бычья свеча, за которой следует большая медвежья свеча) и двойной свечной паттерн «пинцет».

- Динамический трейлинг-стоп использует множитель ATR для корректировки минимальной цены за последние N свечей, обеспечивая адаптацию стоп-лосса к рыночной волатильности.

- Цель по прибыли устанавливается на основе фиксированного соотношения риска к доходности и определяется путем расчета стоимости риска (R) для каждой сделки.

- Размер позиции динамически рассчитывается на основе фиксированной суммы риска и стоимости риска для каждой сделки.

- Механизм выхода по экстремумам RSI срабатывает при перегреве или переохлаждении рынка, подавая сигнал на закрытие позиции.

Преимущества стратегии

- Динамическое управление рисками: благодаря сочетанию ATR и недавних минимумов стоп-лосс может динамически корректироваться в соответствии с рыночной волатильностью.

- Точный контроль позиции: метод расчета позиции на основе фиксированной суммы риска обеспечивает одинаковый уровень риска для каждой сделки.

- Многомерный механизм выхода: сочетание трейлинг-стопа, фиксированной цели по прибыли и выхода по экстремумам RSI — тройной механизм.

- Гибкий выбор направления торговли: возможность выбирать только длинные, только короткие или двусторонние сделки.

- Четкое соотношение риска к доходности: с помощью заранее заданного соотношения риска к прибыли четко определяется целевая прибыль для каждой сделки.

Риски стратегии

- Риск точности распознавания паттернов: возможны ложные идентификации параллельных свечей и свечей «пинцет».

- Риск проскальзывания при установке стоп-лосса: на сильно волатильных рынках возможны значительные проскальзывания.

- Выход по экстремумам RSI может быть преждевременным: на сильных трендовых рынках это может привести к преждевременному выходу и потере потенциальной прибыли.

- Ограниченность фиксированного соотношения риска к доходности: оптимальное соотношение может различаться в разных рыночных условиях.

- Риск переоптимизации параметров: комбинация нескольких параметров может привести к чрезмерной оптимизации.

Направления оптимизации стратегии

- Оптимизация сигналов входа: можно добавить дополнительные подтверждающие индикаторы, такие как объем, трендовые индикаторы и т.д.

- Динамическое соотношение риска к доходности: корректировка соотношения в зависимости от рыночной волатильности.

- Интеллектуальная адаптация параметров: внедрение алгоритмов машинного обучения для динамической оптимизации параметров.

- Подтверждение на нескольких таймфреймах: добавление механизмов подтверждения сигналов на большем количестве временных интервалов.

- Классификация рыночных условий: использование различных комбинаций параметров в зависимости от состояния рынка.

Заключение

Это хорошо продуманная торговая стратегия, объединяющая несколько зрелых концепций технического анализа в единую торговую систему. Преимущество стратегии заключается в комплексной системе управления рисками и гибких правилах торговли, однако необходимо учитывать проблемы оптимизации параметров и адаптации к рынку. Предложенные направления оптимизации открывают возможности для дальнейшего улучшения стратегии.

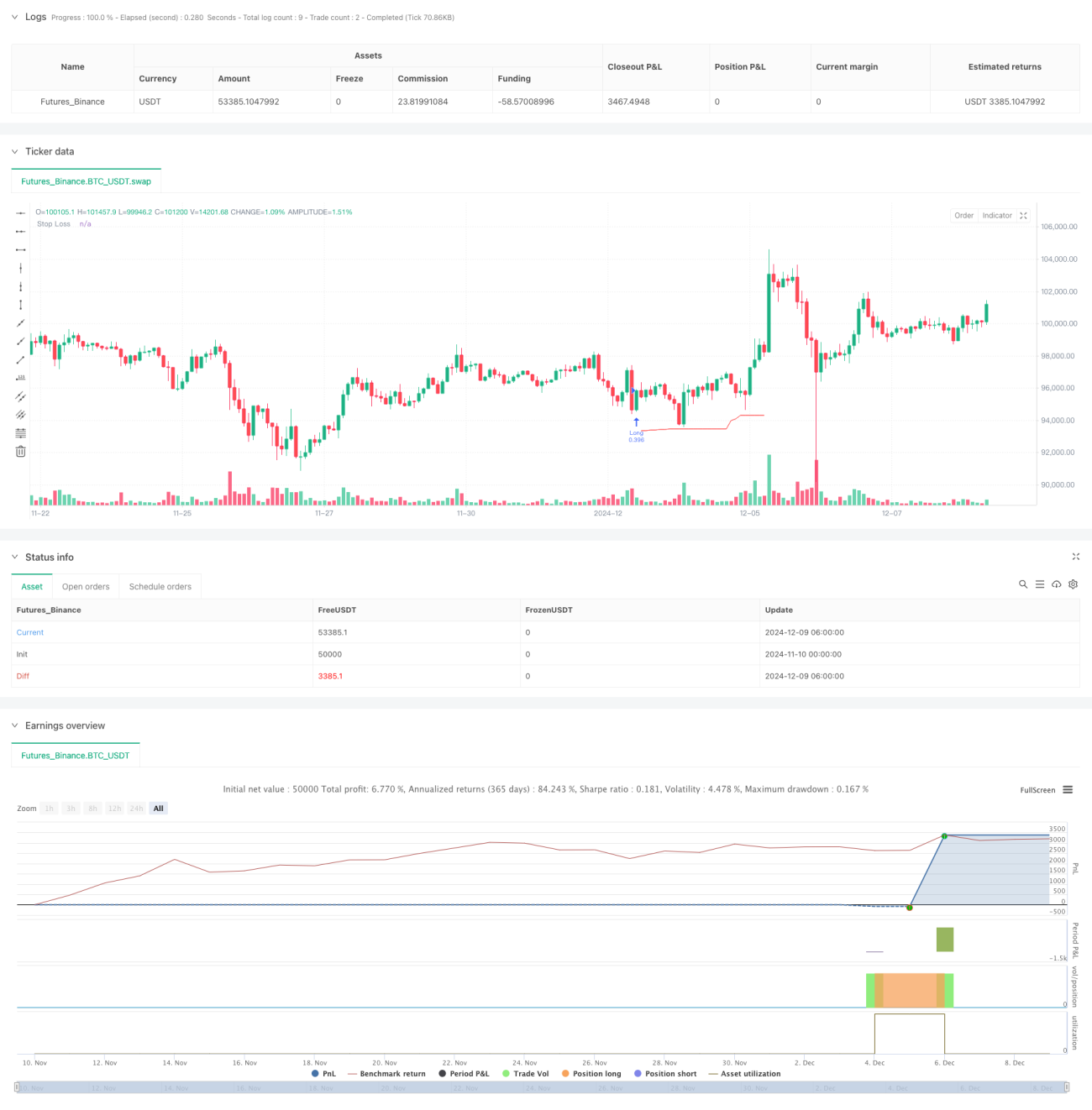

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading | www.TheArtOfTrading.com

// @version=5

strategy("Trailing stop 1", overlay=true)- 1