Обзор

Данная стратегия представляет собой количественную торговую систему, сочетающую индикатор ускорения (AC) и стохастический осциллятор (Stochastic). Она выявляет дивергенцию между ценой и техническими индикаторами, чтобы уловить смену рыночного импульса и предсказать потенциальные развороты тренда. Стратегия также интегрирует скользящую среднюю (SMA) и индекс относительной силы (RSI) для повышения надежности сигналов, а также устанавливает фиксированные уровни тейк-профита и стоп-лосса для управления рисками.

Принцип стратегии

Основная логика стратегии основана на совместной работе нескольких технических индикаторов. Сначала рассчитывается индикатор ускорения (AC), который представляет собой разницу между 5-периодной и 34-периодной скользящими средними от медианной цены, минус её N-периодная скользящая средняя. Одновременно вычисляются значения K и D стохастического осциллятора для подтверждения сигналов дивергенции. Когда цена обновляет минимум, а индикатор AC растет, формируется бычья дивергенция; когда цена обновляет максимум, а AC снижается, формируется медвежья дивергенция. Стратегия также использует RSI в качестве вспомогательного подтверждающего индикатора, повышая точность сигналов за счет перекрестной проверки нескольких индикаторов.

Преимущества стратегии

- Совместная работа нескольких индикаторов: Комбинация AC, Stochastic и RSI позволяет эффективно отфильтровывать ложные сигналы.

- Автоматическое управление рисками: Встроенные фиксированные уровни тейк-профита и стоп-лосса позволяют контролировать риск по каждой сделке.

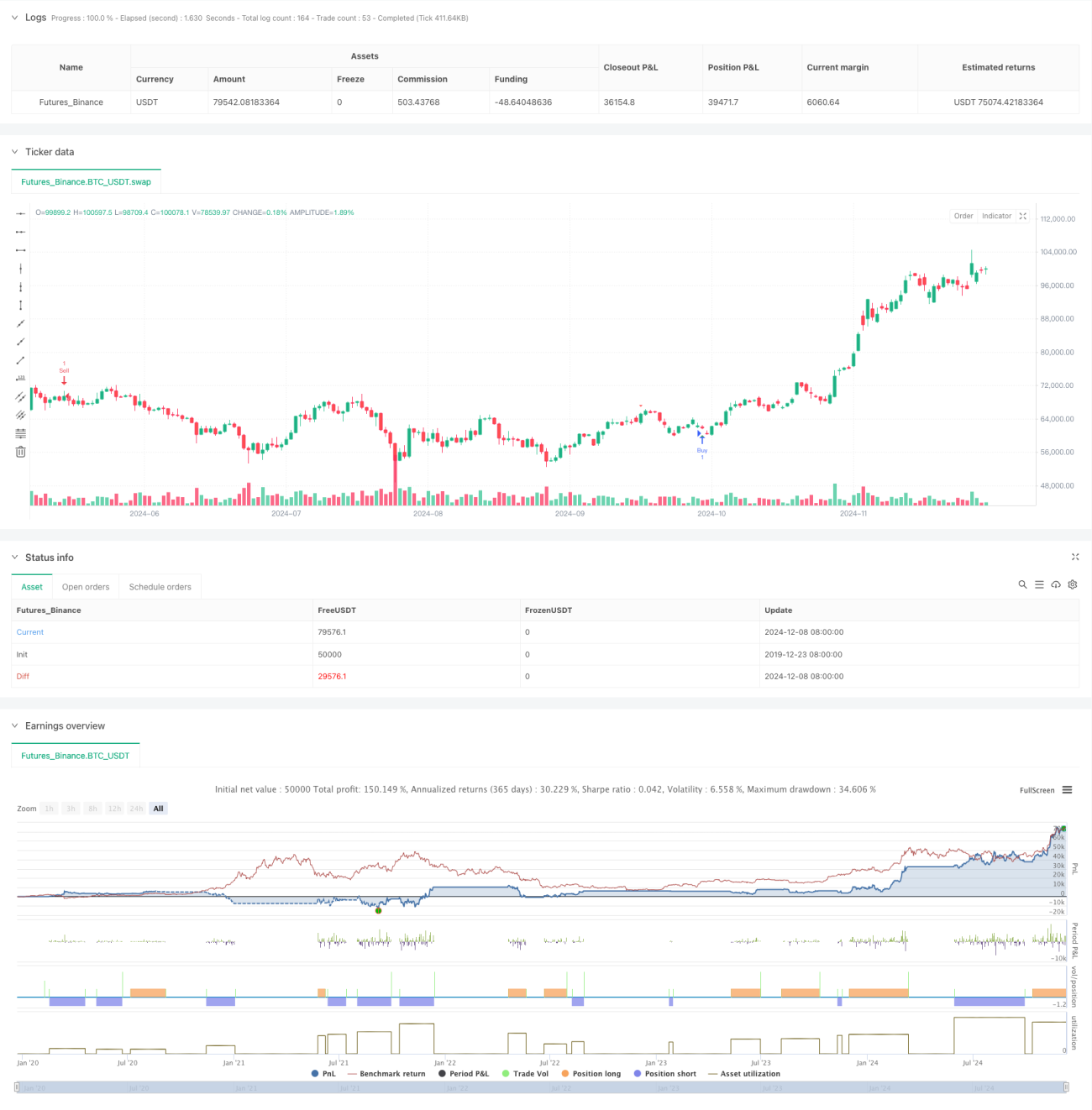

- Визуальные подсказки: На графике четко отображаются сигналы покупки и продажи, что помогает трейдеру быстро идентифицировать возможности.

- Высокая гибкость: Настраиваемые параметры позволяют адаптировать стратегию к различным рыночным условиям и таймфреймам.

- Мгновенные оповещения: Встроенная система сигналов гарантирует, что вы не пропустите торговые возможности.

Риски стратегии

- Риск ложных пробоев: На колебательном рынке могут возникать ложные сигналы дивергенции.

- Риск проскальзывания: Использование фиксированных уровней тейк-профита и стоп-лосса может привести к значительному проскальзыванию при резких движениях рынка.

- Чувствительность к параметрам: Различные комбинации параметров могут существенно повлиять на производительность стратегии.

- Зависимость от рыночных условий: На рынках без четкого тренда эффективность стратегии может снижаться.

- Запаздывание сигналов: Из-за использования скользящих средних сигналы могут быть запоздалыми.

Направления оптимизации стратегии

- Динамические уровни тейк-профита и стоп-лосса: Возможность корректировать уровни в зависимости от волатильности рынка.

- Внедрение индикатора объема: Использование подтверждения объема для повышения надежности сигналов.

- Фильтрация рыночных условий: Добавление модуля определения тренда для применения различных торговых подходов в зависимости от ситуации на рынке.

- Оптимизация параметров: Использование методов машинного обучения для нахождения наилучших комбинаций параметров индикаторов.

- Добавление временных фильтров: Учет временных характеристик рынка, чтобы избегать торговли в неблагоприятные периоды.

Заключение

Это количественная торговая стратегия, объединяющая несколько технических индикаторов для выявления разворотных точек рынка через сигналы дивергенции. Её преимущества заключаются в перекрестной проверке сигналов и развитой системе управления рисками, однако следует учитывать проблемы ложных пробоев и оптимизации параметров. Благодаря постоянной оптимизации и доработке стратегия способна сохранять стабильную эффективность в различных рыночных условиях.

- 1