Среднереверсивная инвестиционная стратегия доллар-стоимостного усреднения на основе полос Боллинджера

Обзор

Данная стратегия представляет собой интеллектуальный инвестиционный подход, сочетающий метод усреднения долларовой стоимости (DCA) и технический индикатор «полосы Боллинджера». Она систематически формирует позиции во время коррекций цен, используя принцип возврата к среднему. Суть стратегии заключается в выполнении покупок на фиксированную сумму при пробое цены ниже нижней полосы Боллинджера, что позволяет получить более выгодные цены входа в периоды рыночных спадов.

Принцип стратегии

Основной принцип стратегии строится на трёх составляющих: 1) метод усреднения долларовой стоимости – регулярное инвестирование фиксированной суммы для снижения риска неудачного выбора времени; 2) теория возврата к среднему – цена в конечном итоге должна вернуться к своему историческому среднему уровню; 3) индикатор полос Боллинджера – используется для выявления зон перекупленности/перепроданности. При пробое цены ниже нижней полосы Боллинджера формируется сигнал на покупку, а объём покупки определяется делением заданной суммы инвестиций на текущую цену. В стратегии используется 200-периодная экспоненциальная скользящая средняя в качестве средней линии полос Боллинджера с множителем стандартного отклонения, равным 2, для определения верхней и нижней границ.

Преимущества стратегии

- Снижение риска выбора времени – систематические покупки вместо субъективных решений уменьшают человеческие ошибки.

- Использование возможностей коррекции – автоматическое выполнение покупок при чрезмерном падении цены.

- Гибкие настройки параметров – возможность корректировать параметры полос Боллинджера и сумму инвестиций в зависимости от рыночных условий.

- Чёткие правила входа и выхода – объективные сигналы на основе технических индикаторов.

- Автоматическое исполнение – не требуется ручное вмешательство, исключаются эмоциональные сделки.

Риски стратегии

- Риск отказа возврата к среднему – на трендовых рынках возможно появление большого числа ложных сигналов.

- Риск управления капиталом – необходимо резервировать достаточные средства для последовательных сигналов на покупку.

- Риск оптимизации параметров – чрезмерная оптимизация может привести к неэффективности стратегии.

- Зависимость от рыночных условий – на высоковолатильных рынках результаты могут быть неудовлетворительными.

Рекомендуется строгое управление капиталом и регулярная оценка эффективности стратегии для управления этими рисками.

Направления оптимизации стратегии

- Введение трендового фильтра для избежания контртрендовых операций на сильных трендах.

- Добавление механизма подтверждения на нескольких временных рамках.

- Оптимизация системы управления капиталом с динамической корректировкой суммы инвестиций в зависимости от волатильности.

- Включение механизма фиксации прибыли при возврате цены к среднему значению.

- Рассмотрение возможности комбинирования с другими техническими индикаторами для повышения надёжности сигналов.

Заключение

Это надёжная стратегия, объединяющая технический анализ с систематическим инвестиционным подходом. Полосы Боллинджера используются для выявления возможностей перепроданности, а метод усреднения долларовой стоимости помогает снизить риски. Ключевыми факторами успеха стратегии являются разумная настройка параметров и строгая дисциплина исполнения. Несмотря на наличие определённых рисков, постоянная оптимизация и управление рисками могут повысить стабильность стратегии.

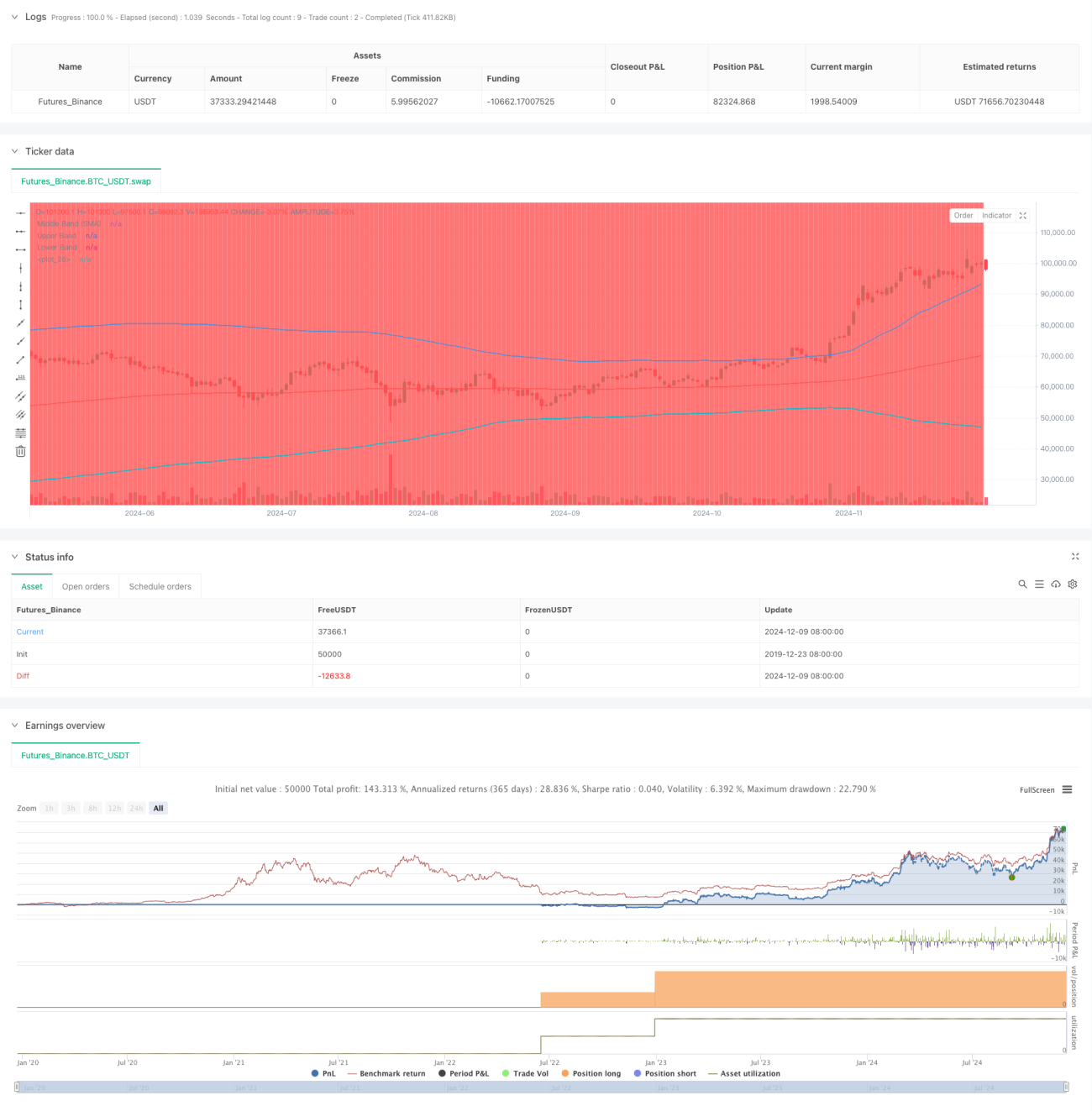

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("DCA Strategy with Mean Reversion and Bollinger Band", overlay=true) // Define the strategy name and set overlay=true to display on the main chart

// Inputs for investment amount and dates- 1