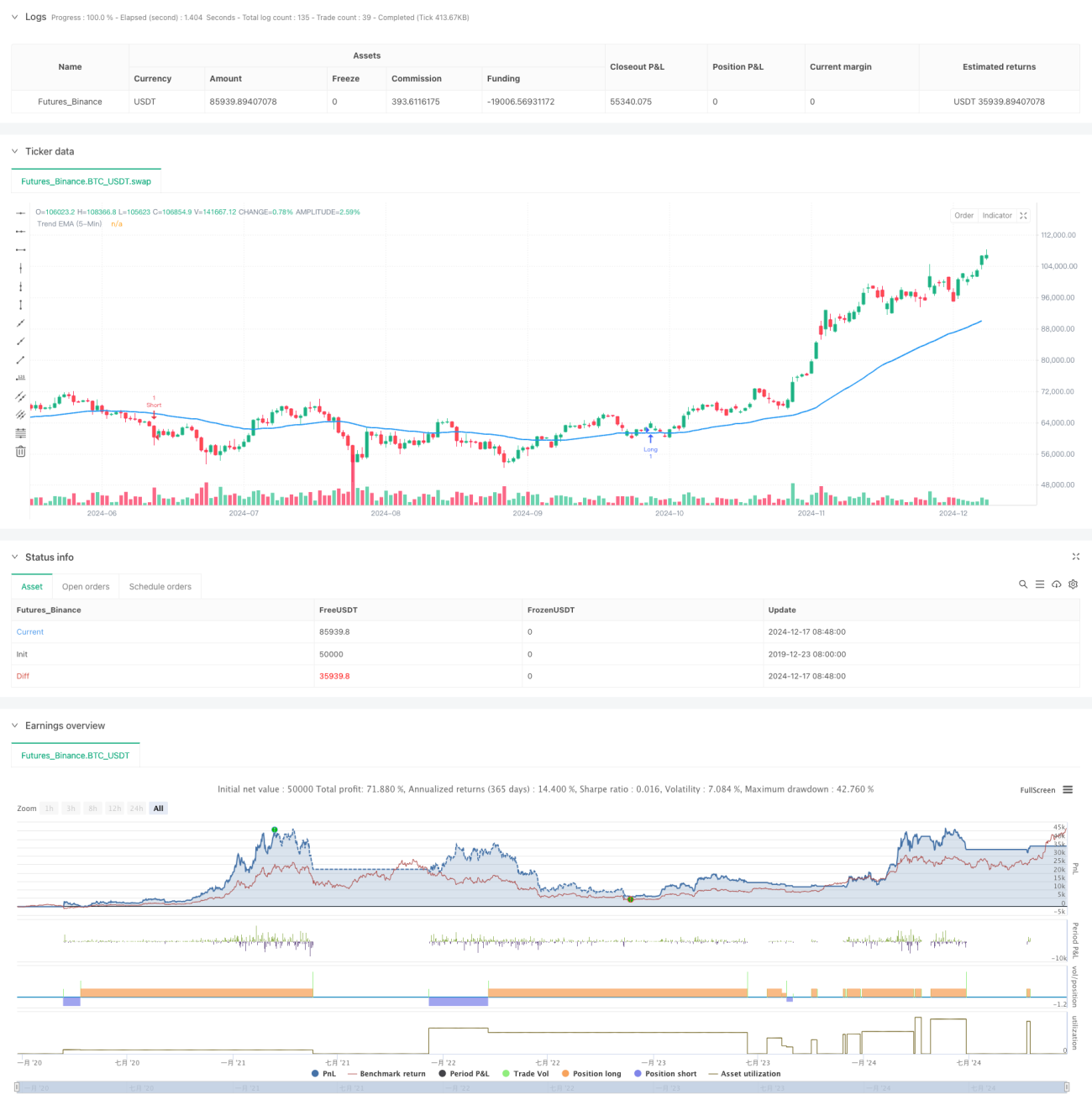

Стратегия трендового следования с несколькими таймфреймами и ATR-стоп-лосс и тейк-профит

Обзор

Это стратегия следования за трендом, сочетающая UT Bot и 50-периодную экспоненциальную скользящую среднюю (EMA). Стратегия в основном используется для краткосрочной торговли на 1-минутном таймфрейме, при этом линия тренда на 5-минутном таймфрейме служит фильтром направления. В стратегии динамически рассчитывается уровень стоп-лосса на основе индикатора ATR и устанавливаются две цели по take-profit для оптимизации доходности.

Принцип стратегии

Основная логика стратегии основана на следующих ключевых компонентах:

- Использование UT Bot для расчета динамических уровней поддержки и сопротивления

- Использование 50-периодной EMA на 5-минутном таймфрейме для определения общего направления тренда

- Комбинирование 21-периодной EMA и сигналов UT Bot для определения точки входа

- Установка динамического трейлинг-стопа на основе множителя ATR

- Установка двух целей по take-profit: 0,5% и 1%, с закрытием 50% позиции по каждой цели

Когда цена пробивает уровень поддержки/сопротивления, рассчитанный UT Bot, и происходит пересечение 21-периодной EMA с UT Bot, при условии, что цена находится в правильном направлении относительно 50-периодной EMA на 5-минутном таймфрейме, генерируется торговый сигнал.

Преимущества стратегии

- Комбинация нескольких таймфреймов повышает надежность торговли

- Динамический стоп-лосс на основе ATR адаптируется к рыночной волатильности

- Двойные цели по take-profit балансируют доходность и процент выигрышных сделок

- Использование свечей Heikin Ashi позволяет отфильтровать часть ложных пробоев

- Гибкий выбор направления торговли (только длинные, только короткие или обе стороны)

Риски стратегии

- Краткосрочная торговля может столкнуться с высокими спредами и комиссиями

- На боковом рынке возможно большое количество ложных сигналов

- Ограничения из-за множества условий могут привести к пропуску некоторых потенциальных возможностей

- Параметры ATR требуют оптимизации под разные рынки

Направления оптимизации стратегии

- Добавление индикатора объема в качестве дополнительного подтверждения

- Рассмотреть возможность введения дополнительных индикаторов рыночных настроений

- Разработка адаптивных параметров для разных характеристик рыночной волатильности

- Добавление фильтрации по времени торговли

- Разработка более умной системы управления позициями

Резюме

Данная стратегия создает целостную торговую систему путем комбинирования множества технических индикаторов и таймфреймов. Она включает не только четкие условия входа и выхода, но и полноценный механизм управления рисками. Хотя на практике все еще требуется оптимизация параметров в зависимости от конкретной рыночной ситуации, общая структура обладает хорошей практичностью и расширяемостью.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

- 1