Обзор

Данная стратегия представляет собой трендовую следящую систему, основанную на двойной скользящей средней и динамическом стоп-лоссе по ATR. Она использует экспоненциальные скользящие средние (EMA) с периодами 38 и 62 для определения рыночного тренда, пересечение цены с быстрой EMA служит сигналом для входа, а совместно с индикатором ATR реализовано динамическое управление стоп-лоссом. Стратегия предлагает два режима торговли – агрессивный и консервативный, чтобы адаптироваться к различным предпочтениям трейдеров по риску.

Принцип стратегии

Основная логика стратегии основана на следующих ключевых элементах:

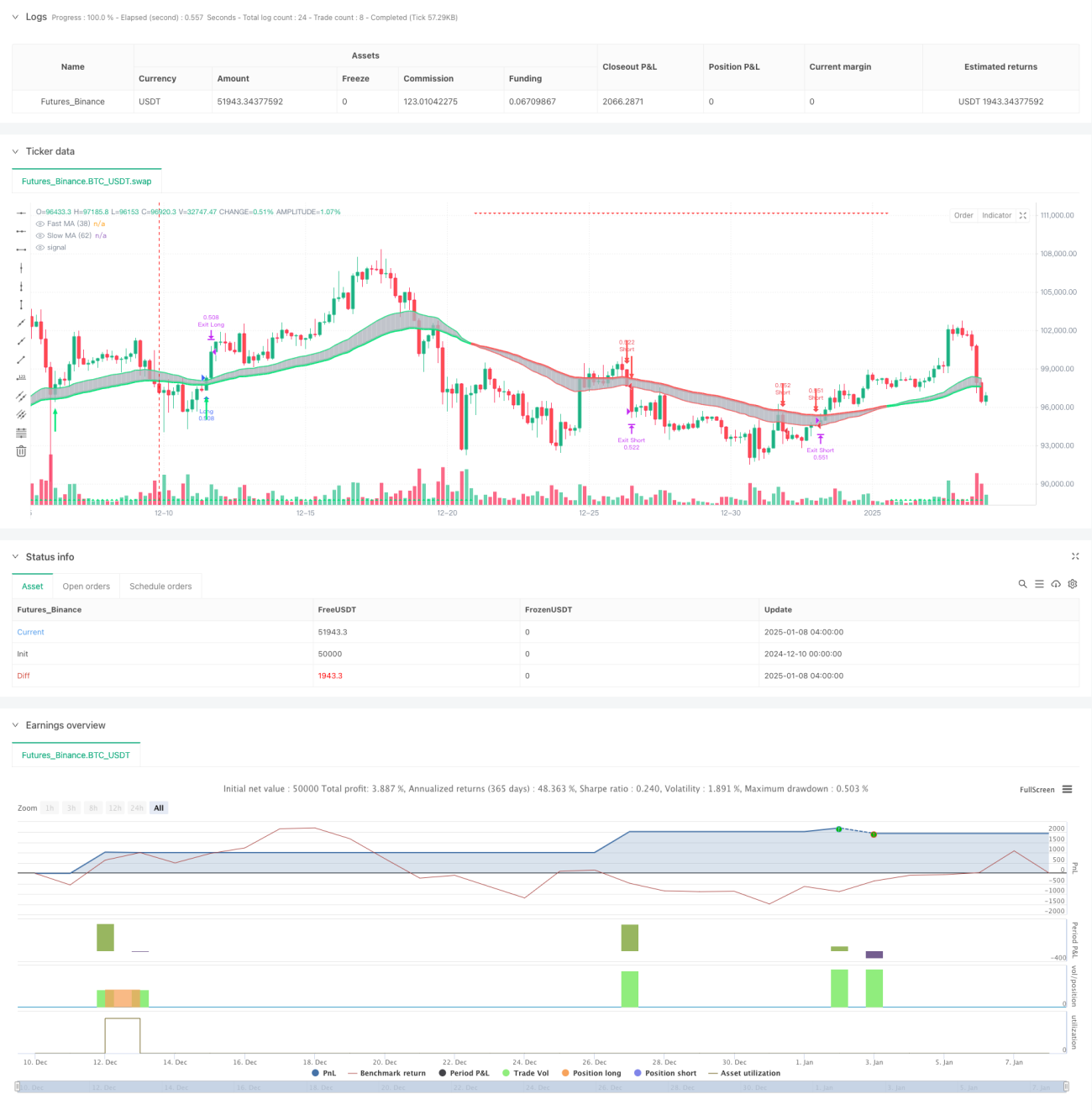

- Определение тренда: Текущий рыночный тренд определяется по взаимному расположению EMA(38) и EMA(62). Когда быстрая EMA находится выше медленной – тренд восходящий, в противном случае – нисходящий.

- Сигналы входа: При восходящем тренде, когда цена пробивает быструю EMA снизу вверх, формируется сигнал на покупку; при нисходящем тренде, когда цена пробивает быструю EMA сверху вниз – сигнал на продажу.

- Управление рисками: Используется динамический стоп-лосс на основе ATR, который корректируется при благоприятном движении цены, защищая полученную прибыль, но не вызывая преждевременного выхода. Также установлены фиксированные процентные стоп-лосс и тейк-профит.

Преимущества стратегии

- Отличная производительность в трендах: Система двойных скользящих средних позволяет эффективно улавливать среднесрочные и долгосрочные тренды, избегая частых сделок в боковике.

- Полноценный контроль рисков: Сочетание фиксированного и динамического стоп-лоссов ограничивает максимальный риск и одновременно защищает прибыль.

- Высокая адаптивность: Наличие агрессивного и консервативного режимов позволяет гибко настраиваться под рыночные условия и индивидуальную толерантность к риску.

- Чёткая визуальная обратная связь: Свечи разного цвета и стрелки наглядно отображают состояние рынка и торговые сигналы.

Риски стратегии

- Риск разворота тренда: В точках разворота возможна серия стоп-лоссов. Рекомендуется входить только при чётко выраженном тренде.

- Риск проскальзывания: При высокой волатильности фактическая цена исполнения может значительно отличаться от сигнальной. Следует немного расширить диапазон стоп-лосса.

- Чувствительность к параметрам: Выбор периодов скользящих средних и множителя ATR существенно влияет на результаты. Требуется оптимизация под разные рыночные условия.

Направления оптимизации

- Добавление фильтра силы тренда: Можно внедрить индикатор силы тренда (например, ADX) и входить только при уверенном тренде.

- Улучшение механизма стоп-лосса: Динамически корректировать множитель ATR в зависимости от волатильности, делая стоп-лосс более адаптивным.

- Подтверждение объёмом: При появлении сигнала входа анализировать объёмы для повышения надёжности сигнала.

- Классификация рыночных условий: В зависимости от рыночной среды (тренд/боковик) динамически изменять параметры стратегии.

Заключение

Данная стратегия объединяет классическую систему двойных скользящих средних с современной техникой динамического стоп-лосса, создавая полноценную трендовую следящую систему. Её преимущества – надёжный контроль рисков и высокая адаптивность, однако трейдеру необходимо оптимизировать параметры и управлять рисками в соответствии с конкретными рыночными условиями. Предложенные направления оптимизации могут дополнительно повысить стабильность и прибыльность стратегии.

- 1