Количественная торговая стратегия с динамическим трейлинг-стопом на основе трети свечи

Обзор

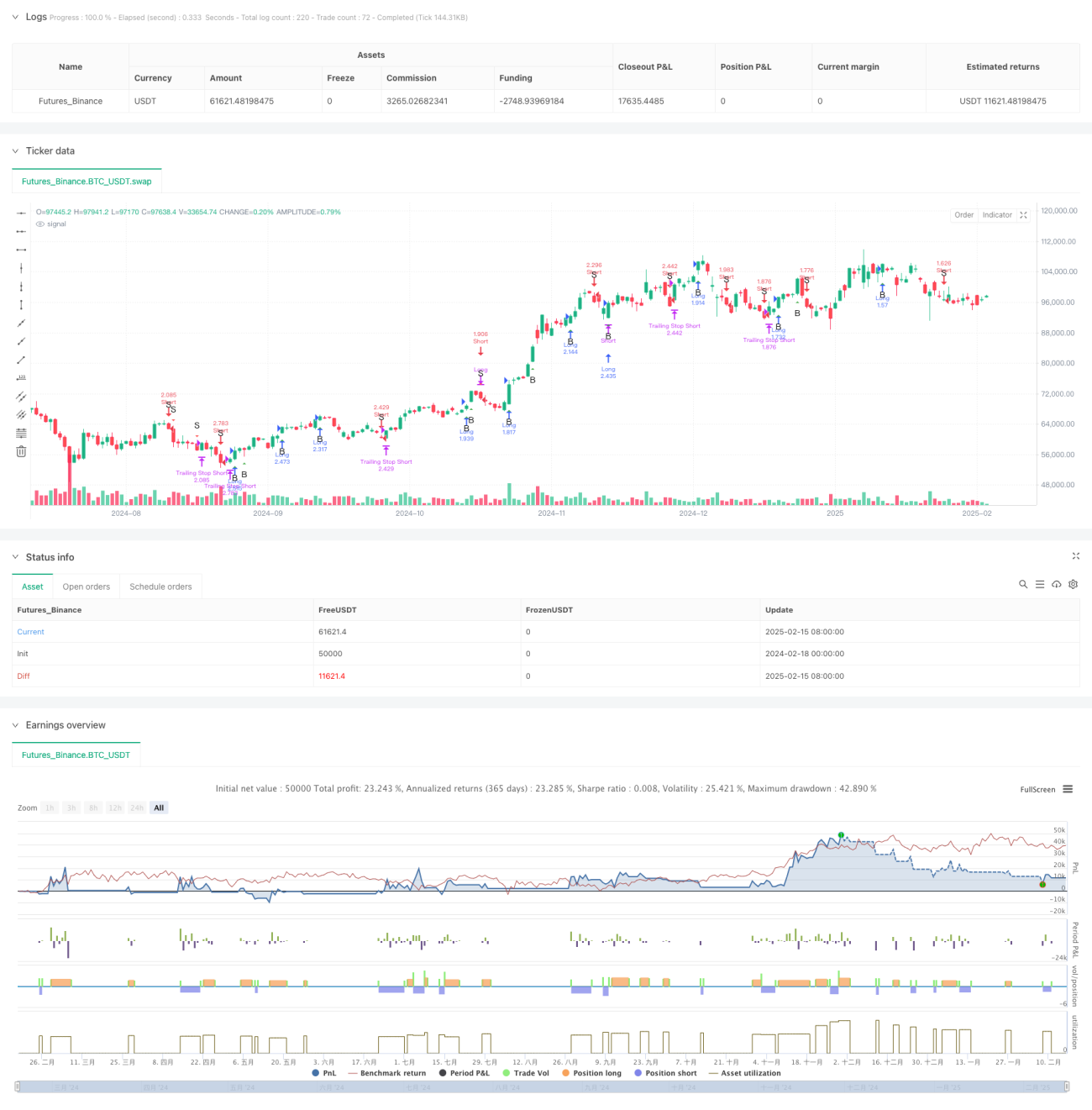

Это количественная торговая стратегия, объединяющая метод анализа свечей на трети (Bill Williams) с динамическим трейлинг-стопом. Стратегия использует структурные особенности текущей и предыдущей свечи для генерации четких сигналов на покупку и продажу, а также применяет настраиваемый трейлинг-стоп для защиты позиций, обеспечивая точный вход/выход и управление рисками.

Принцип стратегии

Основная логика стратегии основана на следующих ключевых частях:

- Расчет третей свечи: Диапазон каждой свечи (максимум – минимум) делится на три равные части, получая границы верхней и нижней зон.

- Классификация форм свечей: В зависимости от положения цены открытия и закрытия относительно третей свечи, свечи классифицируются по типам. Например, когда открытие находится в нижней зоне, а закрытие – в верхней, это считается сильным бычьим паттерном.

- Правила генерации сигналов: Путем комбинированного анализа форм текущей и предыдущей свечи определяются валидные торговые сигналы. Например, если две последовательные свечи демонстрируют сильные характеристики, генерируется сигнал на покупку.

- Динамический трейлинг-стоп: В заданном временном периоде в качестве уровня скользящего стопа используется минимум (для длинных позиций) или максимум (для коротких позиций) за предыдущие N свечей.

Преимущества стратегии

- Четкая логика: Стратегия использует интуитивно понятный метод анализа структуры свечей, правила торговли ясны и легко понимаемы.

- Надежное управление рисками: Механизм динамического трейлинг-стопа позволяет эффективно контролировать риск просадки, сохраняя достаточный потенциал прибыли.

- Высокая адаптивность: Стратегия может настраивать параметры трейлинг-стопа в зависимости от рыночных условий, обладая хорошей гибкостью.

- Высокая степень автоматизации: От генерации сигналов до управления позициями все автоматизировано, что снижает человеческое вмешательство.

Риски стратегии

- Риск бокового рынка: На флэтовом рынке могут часто возникать ложные пробои, приводящие к избыточной торговле.

- Риск гэпов: При сильных гэпах трейлинг-стоп может не сработать вовремя, что приведет к неожиданным убыткам.

- Чувствительность к параметрам: Выбор параметров трейлинг-стопа существенно влияет на результаты стратегии; неправильные настройки могут привести к преждевременному выходу или недостаточной защите.

Направления оптимизации стратегии

- Добавление фильтра рыночных условий: Можно внедрить трендовые индикаторы или индикаторы волатильности для динамической настройки параметров стратегии в разных рыночных условиях.

- Оптимизация механизма стопа: Рассмотреть возможность использования индикатора ATR для установки более гибкого расстояния стопа, повышая его адаптивность.

- Введение управления позицией: Можно динамически изменять размер позиции в зависимости от силы сигнала и рыночной волатильности, обеспечивая более точный контроль рисков.

- Улучшение выхода: Добавить цели по прибыли или вспомогательные индикаторы для оптимизации момента выхода.

Заключение

Это количественная торговая стратегия с целостной структурой и четкой логикой, сочетающая классические методы технического анализа с современными подходами к управлению рисками, что обеспечивает хорошую практичность. Дизайн стратегии учитывает реальные потребности торговли, включая генерацию сигналов, управление позициями и контроль рисков. При дальнейшей оптимизации и доработке стратегия может показать более высокие результаты в реальной торговле.

/*backtest

start: 2024-02-18 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrinityBar with Trailing Stop", overlay=true, initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=250)

- 1