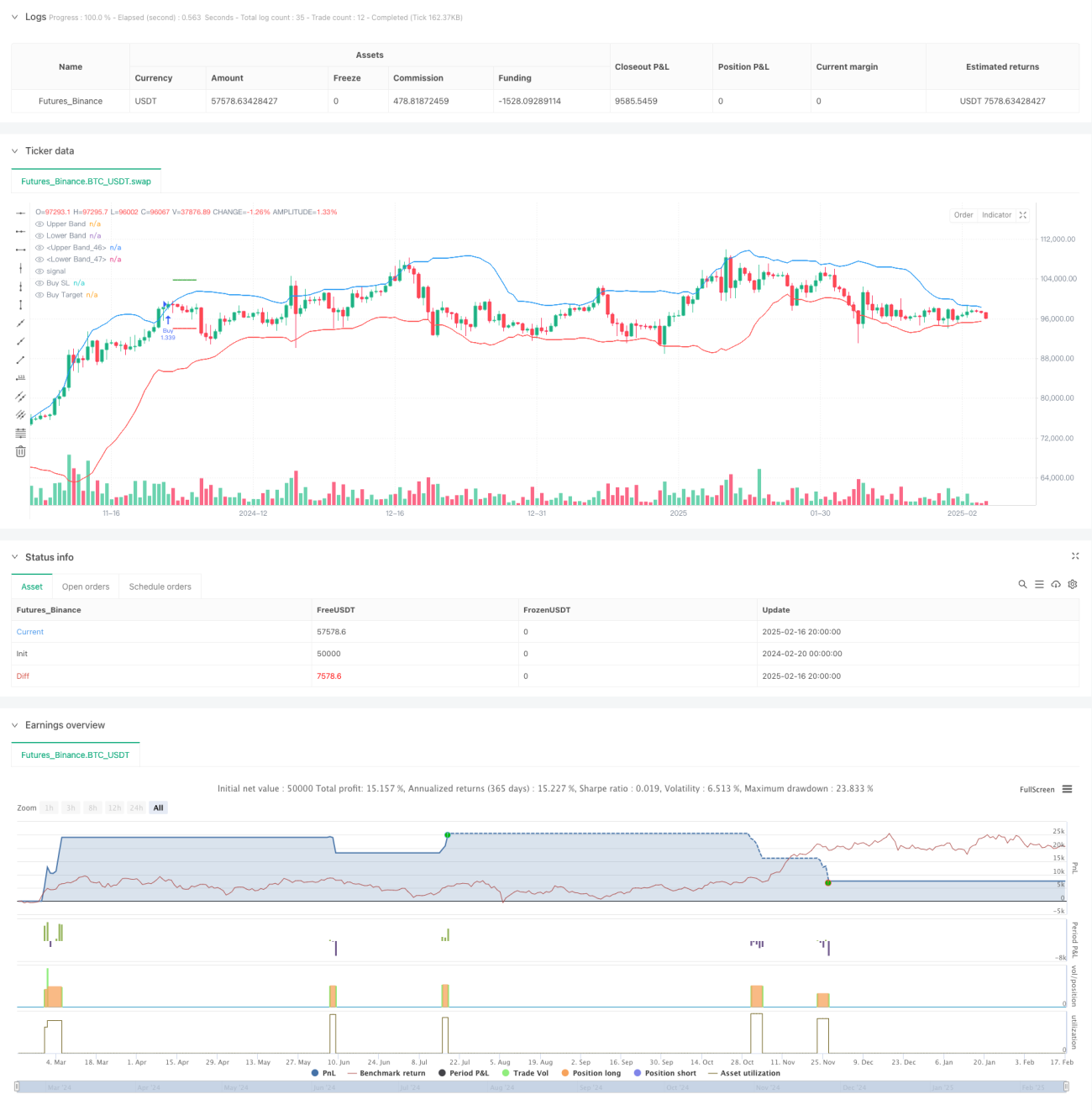

Обзор

Данная стратегия представляет собой трендовую торговую систему, основанную на пробое полос Боллинджера и свечных паттернах. Стратегия выявляет торговые сигналы, идентифицируя три последовательные свечи, пробивающие полосы Боллинджера, а также учитывая положение цены закрытия относительно тела свечи. Система использует фиксированное соотношение риска и прибыли 1:1 для управления стоп-лоссом и тейк-профитом каждой сделки.

Принцип стратегии

Основная логика стратегии базируется на следующих ключевых элементах:

- Используются полосы Боллинджера с периодом 20 и множителем стандартного отклонения 2.0 в качестве основного индикатора.

- Условие для входа в длинную позицию: три последовательные свечи с ценой закрытия выше верхней полосы, причем все три свечи являются бычьими, и цена закрытия находится в верхней половине их тела.

- Условие для входа в короткую позицию: три последовательные свечи с ценой закрытия ниже нижней полосы, причем все три свечи являются медвежьими, и цена закрытия находится в нижней половине их тела.

- Стоп-лосс устанавливается на экстремальном значении самой первой сигнальной свечи.

- Уровень тейк-профита устанавливается на основе соотношения риска и прибыли 1:1.

Преимущества стратегии

- Применяется механизм множественного подтверждения: требования к форме трех последовательных пробивающих свечей эффективно снижают риск ложных пробоев.

- Оценка положения цены закрытия относительно тела свечи повышает надежность подтверждения тренда.

- Использование фиксированного соотношения риска и прибыли для управления позициями упрощает контроль рисков.

- Логика стратегии ясна, легко понимается и выполняется.

- Торговые сигналы наглядно отображаются с помощью функций маркировки, что удобно для анализа при бэктестинге.

Риски стратегии

- На рынке с боковым движением могут часто возникать ложные сигналы.

- Фиксированное соотношение риска и прибыли может не позволить полностью реализовать потенциал сильного трендового движения.

- Строгое требование к трем последовательным свечам может привести к пропуску некоторых потенциально выгодных возможностей.

- Стоп-лосс, установленный на экстремальном значении сигнальной свечи, при высокой волатильности может оказаться слишком далеким.

Рекомендуется управлять рисками следующими способами:

- Адаптировать параметры полос Боллинджера в соответствии с рыночными циклами волатильности.

- Динамически корректировать соотношение риска и прибыли на основе характеристик рынка.

- Добавлять индикаторы подтверждения тренда.

- Оптимизировать метод установки уровня стоп-лосса.

Направления оптимизации стратегии

- Оптимизация параметров:

- Возможность динамической настройки периода полос Боллинджера и множителя стандартного отклонения в зависимости от характеристик рынка.

- Рассмотреть возможность замены требования к трем свечам на динамическую оценку.

- Оптимизация сигналов:

- Добавить индикаторы подтверждения тренда, такие как ADX или трендовые линии.

- Ввести механизм подтверждения объемом торгов.

- Рассмотреть возможность добавления осцилляторов в качестве вспомогательных индикаторов.

- Оптимизация управления позициями:

- Реализовать динамическое установление соотношения риска и прибыли.

- Добавить модуль управления капиталом.

- Рассмотреть возможность использования механизмов поэтапного открытия и закрытия позиций.

- Оптимизация стоп-лосса:

- Внедрить механизм трейлинг-стопа.

- Устанавливать расстояние до стоп-лосса на основе ATR.

- Рассмотреть возможность использования временного стоп-лосса.

Заключение

Это структурно завершенная и логически ясная трендовая стратегия. Благодаря механизму множественного подтверждения через пробой полос Боллинджера и свечные паттерны, она эффективно снижает риск ложных сигналов. Фиксированное соотношение риска и прибыли упрощает управление сделками, но также ограничивает гибкость стратегии. Стратегия имеет значительный потенциал для улучшения за счет оптимизации параметров, добавления подтверждающих индикаторов, улучшения управления позициями и другими методами. В целом, это практичный базовый каркас стратегии, который может быть доработан в соответствии с конкретными требованиями.

/*backtest

start: 2024-02-20 00:00:00

end: 2025-02-17 08:00:00

period: 12h

basePeriod: 12h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Bollinger Band Strategy (Close Near High/Low Relative to Half Range)", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=200, pyramiding=0)

// Bollinger Bands- 1