Комбинированная стратегия динамического адаптивного мультитаймфреймового следования за трендом и разворота колебаний

Обзор

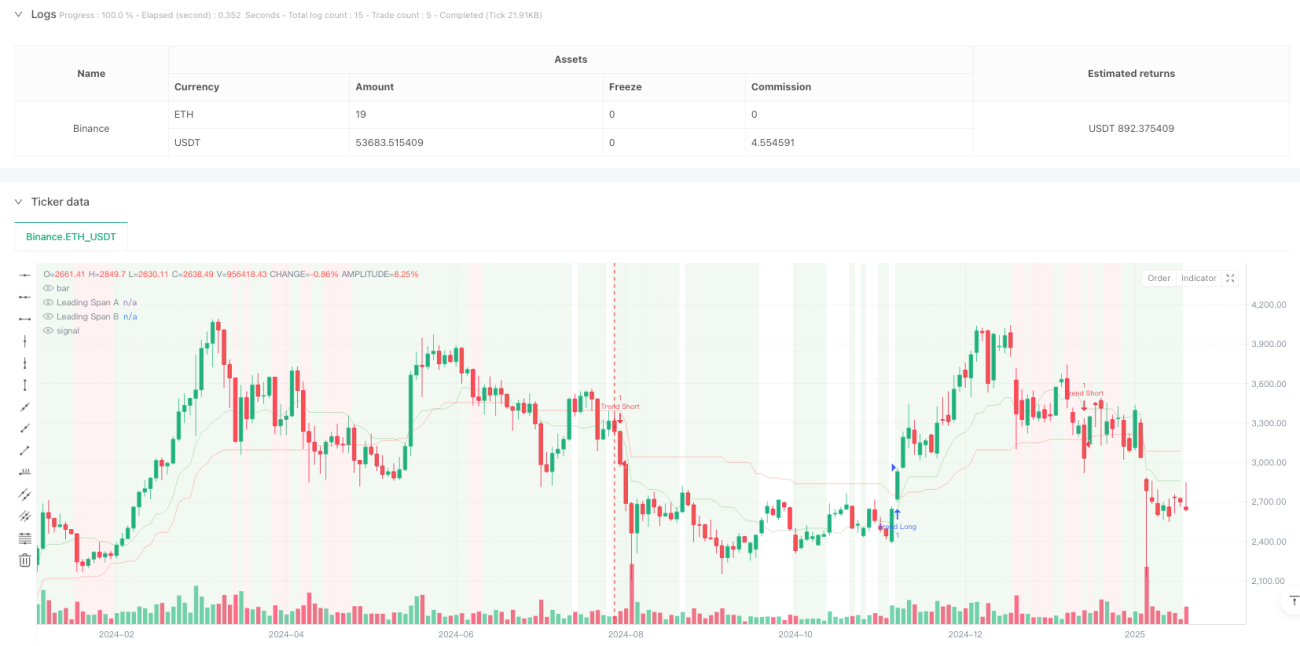

Данная стратегия представляет собой комбинированную торговую систему, сочетающую трендовое следование и торговлю в диапазоне. Она использует облако Ишимоку для определения состояния рынка, MACD для подтверждения импульса, RSI для сигналов перекупленности/перепроданности, а также ATR для динамического управления стоп-лоссом. Стратегия способна捕捉 трендовые возможности на трендовых рынках и находить точки разворота на колебательных рынках, обладая высокой адаптивностью и гибкостью.

Принцип стратегии

Стратегия использует многоуровневый механизм подтверждения сигналов:

- Облако Ишимоку служит основным индикатором состояния рынка: по положению цены относительно облака определяется, находится ли рынок в тренде или в боковике.

- На трендовом рынке: когда цена выше облака, RSI > 55 и гистограмма MACD положительна, открывается длинная позиция; когда цена ниже облака, RSI < 45 и гистограмма MACD отрицательна, открывается короткая позиция.

- На колебательном рынке: при RSI < 30 и стохастическом RSI < 20 ищутся возможности для покупки; при RSI > 70 и стохастическом RSI > 80 — для продажи.

- Для управления рисками используется динамический стоп-лосс на основе ATR с расстоянием, равным 2-кратному значению ATR.

Преимущества стратегии

- Высокая адаптивность к рынку: стратегия автоматически корректируется в зависимости от состояния рынка, повышая устойчивость.

- Высокая надежность сигналов: множественное подтверждение индикаторами снижает влияние ложных сигналов.

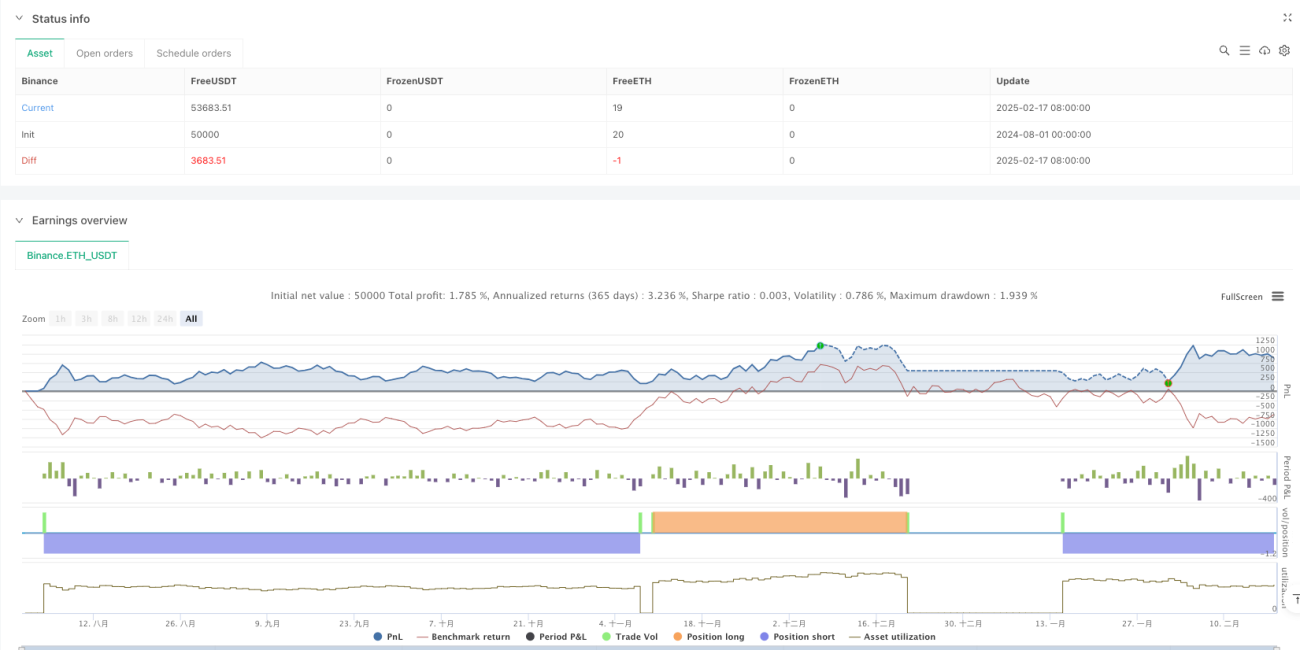

- Хороший контроль рисков: динамический стоп-лосс по ATR позволяет как развивать прибыль, так и эффективно ограничивать убытки.

- Отличная визуализация: фоновая окраска обозначает состояние рынка, облегчая трейдеру интуитивное понимание рыночной среды.

- Отличные показатели на старших таймфреймах: на дневном графике коэффициент прибыли составляет 2,159, чистая прибыль — 10,71%.

Риски стратегии

- Низкий процент выигрышных сделок: на всех таймфреймах процент побед ниже 40%, что требует высокой психологической устойчивости.

- Чрезмерная торговля на младших таймфреймах: на 4-часовом графике выполнено 430 сделок, эффективность низкая.

- Запаздывание сигналов: из-за множественных подтверждений могут быть упущены некоторые рыночные возможности.

- Сложность оптимизации параметров: комбинация нескольких индикаторов усложняет процесс настройки стратегии.

Направления оптимизации стратегии

- Оптимизация фильтрации сигналов: можно скорректировать пороговые значения индикаторов для повышения процента выигрышных сделок.

- Адаптация таймфреймов: рекомендуется использовать в основном на дневных и старших таймфреймах, параметры можно настраивать под особенности рынка.

- Оптимизация стоп-лосса: можно рассмотреть динамическое изменение множителя ATR в зависимости от состояния рынка.

- Оптимизация времени входа: можно добавить подтверждение объемов или ценовых паттернов для повышения точности входа.

- Оптимизация управления капиталом: можно разработать систему динамического управления позицией на основе силы сигнала.

Заключение

Данная стратегия представляет собой логически обоснованную и чётко оформленную комплексную торговую систему. За счёт совместного использования нескольких индикаторов она обеспечивает интеллектуальное распознавание состояния рынка и точный захват торговых возможностей. Несмотря на некоторые проблемы на младших таймфреймах, она показывает отличные результаты на старших, таких как дневной. Трейдерам рекомендуется при реальной торговле уделять основное внимание сигналам на дневном графике и разумно корректировать параметры в соответствии с собственной толерантностью к риску. При постоянной оптимизации и настройке данная стратегия способна обеспечить стабильные возможности для получения прибыли.

- 1