Стратегия межпериодной трендовой торговли биткоином на основе динамической силы EMA и RSI на множественных уровнях

Обзор

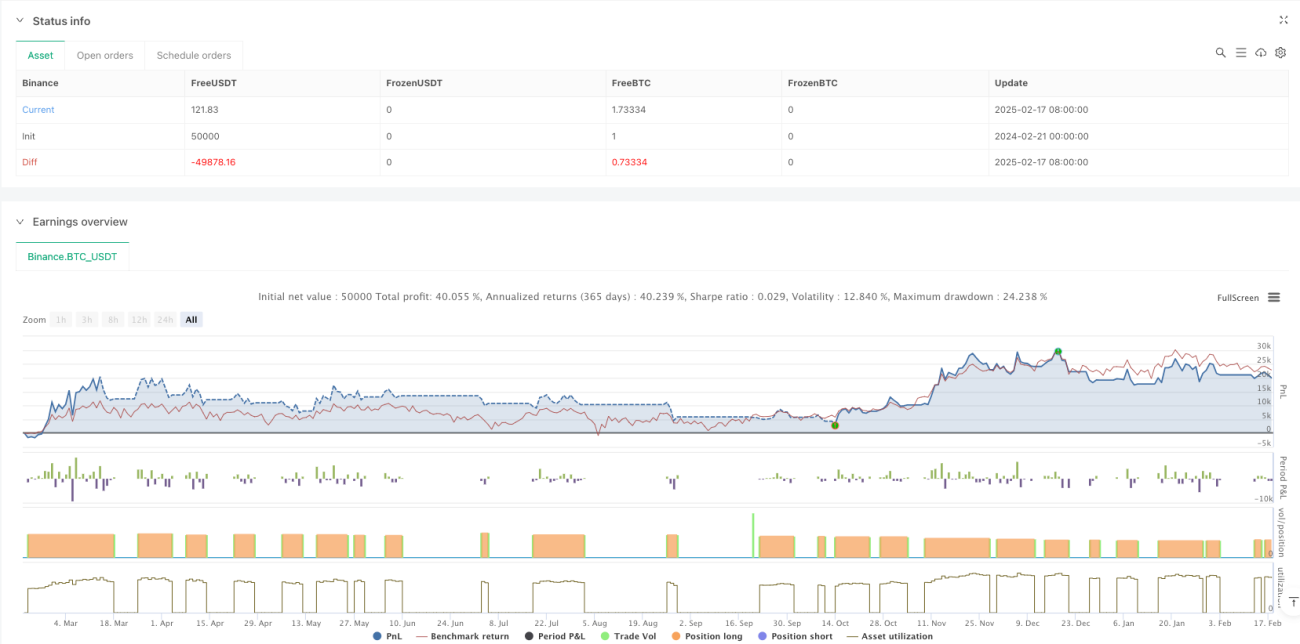

Стратегия представляет собой систему отслеживания тренда, основанную на межвременном анализе, сочетающем скользящие средние EMA недельного и дневного уровней, а также индикатор RSI для определения рыночного тренда и импульса. Торговые возможности определяются по согласованности тренда на нескольких таймфреймах, а для управления рисками используется динамический стоп-лосс на основе ATR. Система применяет управление капиталом, используя 100% средств счета на каждую сделку, и учитывает комиссию за торговлю в размере 0,1%.

Принцип стратегии

Основная логика стратегии основана на следующих ключевых элементах:

- Использование EMA недельного уровня в качестве основного фильтра тренда, в сочетании с соотношением дневной цены закрытия и недельной EMA для определения рыночного состояния.

- Динамическая корректировка пороговых значений для определения тренда с помощью индикатора ATR, что повышает адаптивность стратегии.

- Интеграция импульсного индикатора RSI в качестве дополнительного фильтра для торговли.

- Использование системы трейлинг-стопа на основе минимальной цены за 7 дней и ATR.

- При появлении сигнала о чрезмерном росте стратегия приостанавливает открытие позиций, чтобы избежать риска.

Преимущества стратегии

- Анализ на нескольких таймфреймах обеспечивает более полное представление о рынке и позволяет эффективно отфильтровывать ложные пробои.

- Механизм динамического стоп-лосса адаптируется к рыночной волатильности, обеспечивая гибкий контроль рисков.

- Фильтр импульса RSI помогает подтвердить силу тренда, повышая качество входа в рынок.

- Система включает механизм предупреждения о чрезмерном росте, что помогает избежать рисков просадки.

- Параметры стратегии легко настраиваются, что позволяет оптимизировать ее под различные рыночные условия.

Риски стратегии

- На боковом рынке возможны частые входы и выходы, что приводит к увеличению торговых издержек.

- Использование 100% средств на каждую сделку несет значительный риск просадки.

- Зависимость от технических индикаторов может привести к несвоевременной реакции на рыночные события.

- Анализ на нескольких таймфреймах может давать противоречивые сигналы на разных уровнях.

- Трейлинг-стоп может быть преждевременно срабатывать при резких колебаниях.

Направления оптимизации стратегии

- Внедрение фильтра волатильности для снижения частоты торговли в периоды низкой волатильности.

- Добавление системы управления позицией, динамически корректирующей долю позиции в зависимости от рыночного состояния.

- Интеграция фундаментальных индикаторов для дополнительной оценки рыночной среды.

- Оптимизация параметров трейлинг-стопа для лучшей адаптации к различным рыночным фазам.

- Включение анализа объема для повышения точности определения тренда.

Заключение

Это хорошо структурированная и логически ясная стратегия следования за трендом. Благодаря анализу на нескольких таймфреймах и динамическим индикаторам, стратегия достаточно хорошо улавливает основные тренды. Несмотря на некоторые внутренние риски, стратегия имеет значительный потенциал для улучшения за счет оптимизации параметров и добавления дополнительных индикаторов. Рекомендуется провести тщательное бэктестирование перед реальной торговлей и настроить параметры в соответствии с конкретными рыночными условиями.

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

// @version=6

strategy("Bitcoin Regime Filter Strategy", // Strategy name

overlay=true, // The strategy will be drawn directly on the price chart

initial_capital=10000, // Initial capital of 10000 USD- 1