Интеллектуальная многомерная адаптивная система для трендовой торговли

Обзор

Данная стратегия представляет собой интеллектуальную торговую систему, объединяющую множество технических индикаторов. Она идентифицирует рыночные возможности на основе комплексного анализа Fair Value Gap (FVG), трендовых сигналов и ценовых паттернов. Система использует двойной механизм стратегии, сочетая особенности следования за трендом и свинговой торговли, оптимизируя эффективность сделок через динамическое управление позицией и многомерные механизмы выхода. Стратегия уделяет особое внимание контролю рисков, фильтруя сигналы на основе волатильности и подтверждения объёмов.

Принцип стратегии

Основная логика стратегии базируется на следующих аспектах:

- Идентификация FVG-разрывов – вычисление размера ценовых гэпов для поиска потенциальных торговых возможностей.

- Система подтверждения тренда – используется комбинация 200-дневной скользящей средней, индикатора SuperTrend и MACD для подтверждения рыночного тренда.

- Подтверждение «умных денег» – применение уровней перекупленности/перепроданности RSI, аномалий объёмов и ценовых паттернов в качестве триггеров сделок.

- Динамическое управление позицией – корректировка размера позиции на основе волатильности (ATR) для обеспечения единообразного рискового профиля.

- Многоуровневый выход из позиции – сочетание трейлинг-стопа и целевой фиксации прибыли для управления завершением сделок.

Преимущества стратегии

- Высокая адаптивность – стратегия способна автоматически настраивать параметры и размер позиции в зависимости от рыночной волатильности.

- Надёжный контроль рисков – множественные фильтры и строгое управление позицией минимизируют риски.

- Качественные сигналы – многомерное подтверждение индикаторами повышает точность торговых сигналов.

- Гибкость в торговле – позволяет одновременно захватывать возможности как трендовых, так и флэтовых рынков.

- Научное управление капиталом – используется процентное управление риском, обеспечивающее рациональное использование средств.

Риски стратегии

- Чувствительность к параметрам – настройка нескольких параметров может влиять на производительность, требуется постоянная оптимизация.

- Зависимость от рыночных условий – в определённых рыночных условиях возможны ложные пробои.

- Влияние проскальзывания – на рынках с низкой ликвидностью возможны значительные проскальзывания.

- Вычислительная сложность – расчёт множественных индикаторов может приводить к задержкам сигналов.

- Высокие требования к капиталу – полная реализация стратегии требует значительного начального капитала.

Направления оптимизации стратегии

- Оптимизация весов индикаторов – можно внедрить методы машинного обучения для динамической корректировки весов индикаторов.

- Повышение рыночной адаптивности – добавить механизм адаптации к рыночной волатильности.

- Улучшение фильтрации сигналов – внедрить дополнительные микроструктурные индикаторы.

- Оптимизация механизма исполнения – добавить интеллектуальное дробление ордеров для снижения затрат на проскальзывание.

- Модернизация контроля рисков – внедрить динамическую систему управления бюджетом риска.

Заключение

Данная стратегия представляет собой целостную торговую систему, объединяющую несколько технических индикаторов и торговых приёмов. Её преимущество заключается в способности адаптироваться к рыночным изменениям при сохранении строгого контроля рисков. Несмотря на определённые возможности для оптимизации, в целом это разумно разработанная количественная торговая стратегия.

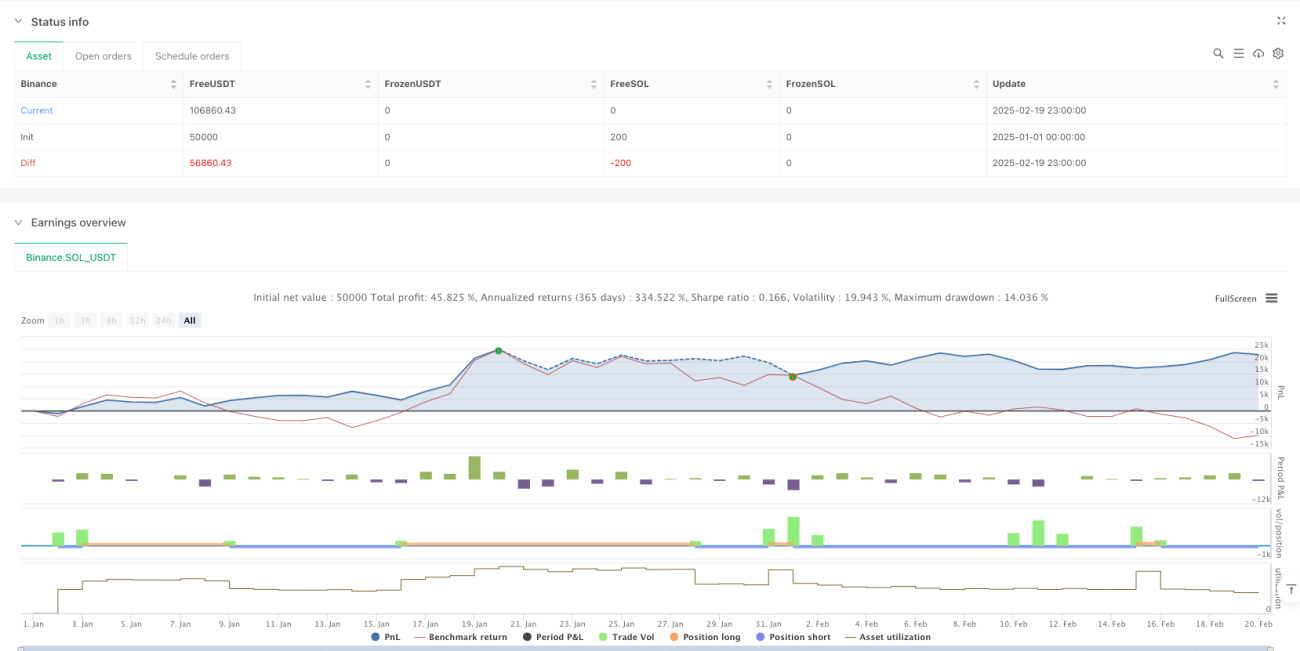

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1