Обзор

Данная торговая стратегия основана на принципе возврата к среднему с использованием полос Боллинджера и реализует частичное получение прибыли с помощью нескольких уровней тейк-профита. Стратегия совершает сделки при прорыве цены за пределы полос Боллинджера и последующем возврате внутрь, устанавливая 5 различных уровней тейк-профита для постепенного сокращения позиции. Также установлен динамический стоп-лосс для контроля рисков. Стратегия может работать в заданные торговые сессии и поддерживает добавление позиций.

Принцип стратегии

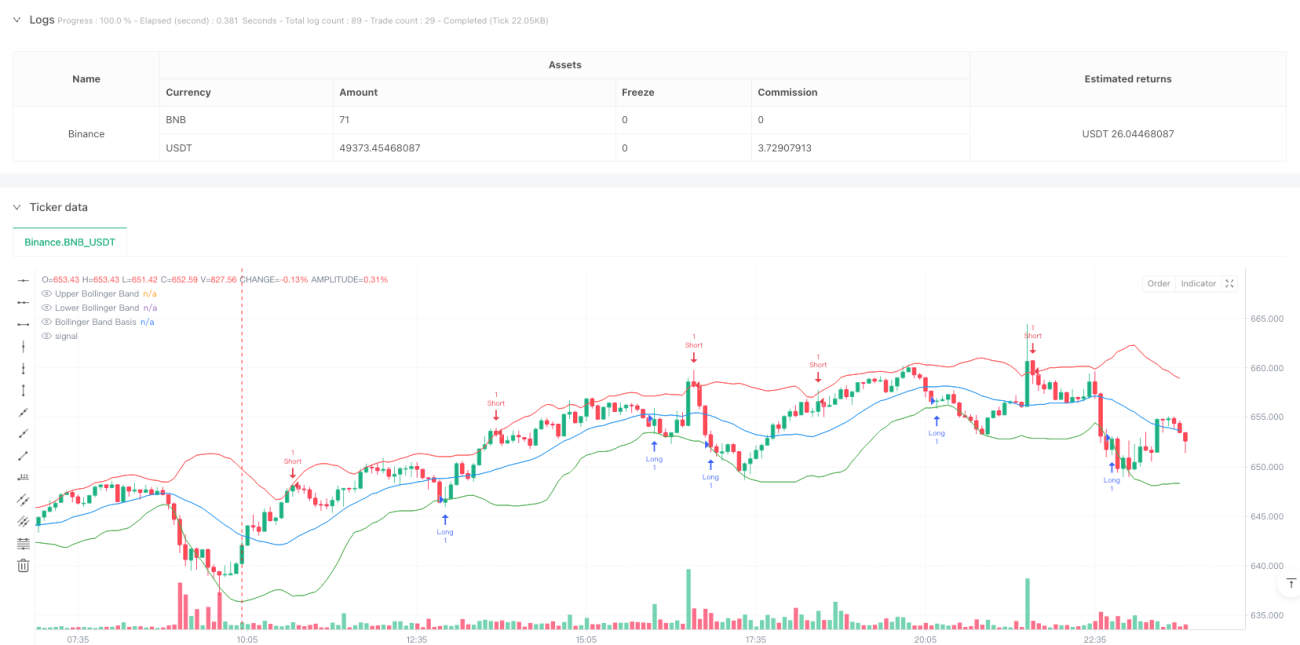

Стратегия использует 20-периодные полосы Боллинджера с коэффициентом 2 для стандартного отклонения в качестве диапазона волатильности. Когда цена пробивает нижнюю полосу снизу и закрывается внутри диапазона, генерируется сигнал на покупку; когда цена пробивает верхнюю полосу сверху и закрывается внутри диапазона, генерируется сигнал на продажу. После входа в позицию стратегия использует 5-уровневый механизм тейк-профита: уровни устанавливаются на 0,5%, 1%, 1,5%, 2% и 2,5%, на каждом из которых закрывается 20% позиции. Последний уровень тейк-профита устанавливается на противоположной полосе Боллинджера. Одновременно установлен стоп-лосс в 1% для контроля рисков.

Преимущества стратегии

- Многоуровневый механизм тейк-профита позволяет получать больше прибыли при продолжении тренда, одновременно фиксируя часть прибыли.

- Поддержка добавления позиций при правильном направлении сделки повышает доходность.

- Использование полос Боллинджера в качестве динамических уровней поддержки и сопротивления позволяет адаптироваться к рыночной волатильности.

- Возможность настройки торговых сессий позволяет избежать помех вне торгового времени.

- Наличие механизма стоп-лосса эффективно ограничивает риски.

Риски стратегии

- На высоковолатильных рынках могут часто возникать ложные сигналы прорыва.

- При быстрых трендах стратегия может упустить более значительные возможности получения прибыли.

- Механизм добавления позиций при развороте рынка может привести к большим убыткам.

- Множество ордеров тейк-профита могут не быть полностью исполнены из-за недостаточной ликвидности.

Рекомендуется адаптировать стратегию к различным рыночным условиям путем настройки параметров полос Боллинджера и соотношения тейк-профита и стоп-лосса.

Направления оптимизации стратегии

- Внедрение индикатора объема в качестве фильтра сигналов для повышения надежности прорывов.

- Динамическая корректировка уровней тейк-профита и стоп-лосса в зависимости от волатильности.

- Добавление индикатора фильтрации тренда, чтобы избежать контртрендовой торговли при сильных трендах.

- Оптимизация логики добавления позиций с установкой ограничения на максимальный размер позиции.

- Рассмотреть возможность добавления функции скользящего стоп-лосса для лучшей защиты прибыли.

Заключение

Данная стратегия использует полосы Боллинджера для выявления возможностей возврата к среднему, применяя многоуровневый тейк-профит и динамический стоп-лосс для управления рисками. Её преимущества заключаются в гибком управлении позициями и механизме контроля рисков, однако при использовании необходимо учитывать адаптацию к рыночным условиям. Добавление дополнительных фильтров и оптимизация параметров тейк-профита и стоп-лосса могут进一步提高 стабильность и доходность стратегии.

- 1