Стратегия разворота тренда с двойным импульсом на основе RSI и стохастического RSI

Обзор

Это торговая стратегия разворота тренда, основанная на комбинации индекса относительной силы (RSI) и стохастического RSI. Стратегия выявляет потенциальные точки разворота, определяя состояния перекупленности/перепроданности рынка и изменения импульса, и на их основе совершает сделки. Основная идея заключается в использовании RSI в качестве базового индикатора импульса, а затем на его основе рассчитывается стохастический RSI для дальнейшего подтверждения направления изменения ценового импульса.

Принцип стратегии

Основная логика стратегии включает следующие ключевые шаги:

- Сначала рассчитывается значение RSI для цены закрытия, чтобы определить общее состояние перекупленности/перепроданности.

- На основе значения RSI рассчитываются линии %K и %D стохастического RSI.

- Когда RSI находится в зоне перепроданности (по умолчанию ниже 30) и линия %K стохастического RSI пересекает линию %D снизу вверх, генерируется сигнал на открытие длинной позиции.

- Когда RSI находится в зоне перекупленности (по умолчанию выше 70) и линия %K стохастического RSI пересекает линию %D сверху вниз, генерируется сигнал на открытие короткой позиции.

- При возникновении противоположных условий по RSI или обратном пересечении стохастического RSI позиция закрывается.

Преимущества стратегии

- Механизм двойного подтверждения – использование RSI и стохастического RSI позволяет эффективно снизить риски ложных пробоев.

- Настраиваемые параметры – ключевые параметры стратегии, такие как период RSI и пороги перекупленности/перепроданности, могут быть скорректированы в зависимости от рыночной ситуации.

- Динамическая визуализация – стратегия предоставляет отображение в реальном времени графиков RSI и стохастического RSI для удобства мониторинга трейдерами.

- Встроенное управление рисками – включает полный механизм стоп-лосса и фиксации прибыли.

- Высокая адаптивность – может применяться на различных временных интервалах и в разных рыночных условиях.

Риски стратегии

- Риск бокового рынка – на флэтовом рынке может генерировать частые ложные сигналы.

- Риск запаздывания – из-за множественного сглаживания скользящих средних сигналы могут иметь некоторую задержку.

- Чувствительность к параметрам – разные настройки параметров могут приводить к существенно различающимся результатам торговли.

- Зависимость от рыночных условий – на сильных трендовых рынках можно упустить часть движений.

- Риск управления капиталом – необходимо разумно устанавливать долю позиции для контроля риска.

Направления оптимизации стратегии

- Добавление фильтра тренда – можно добавить долгосрочную скользящую среднюю в качестве фильтра тренда, открывая позиции только по направлению тренда.

- Оптимизация механизма стоп-лосса – можно внедрить динамический стоп-лосс, например, трейлинг-стоп или стоп на основе ATR.

- Включение объемных индикаторов – анализ объёмов может повысить надёжность сигналов.

- Добавление временного фильтра – можно избегать времени выхода важных новостей или периодов низкой ликвидности.

- Разработка адаптивных параметров – автоматическая настройка параметров стратегии в зависимости от волатильности рынка.

Заключение

Это комплексная стратегия, сочетающая импульс и разворот тренда, использующая синергию RSI и стохастического RSI для выявления потенциальных торговых возможностей. Стратегия имеет разумную конструкцию, хорошую настраиваемость и адаптивность. Однако в реальном применении необходимо учитывать выбор рыночных условий и контроль рисков; перед началом реальной торговли рекомендуется провести тщательное бэктестирование и оптимизацию параметров.

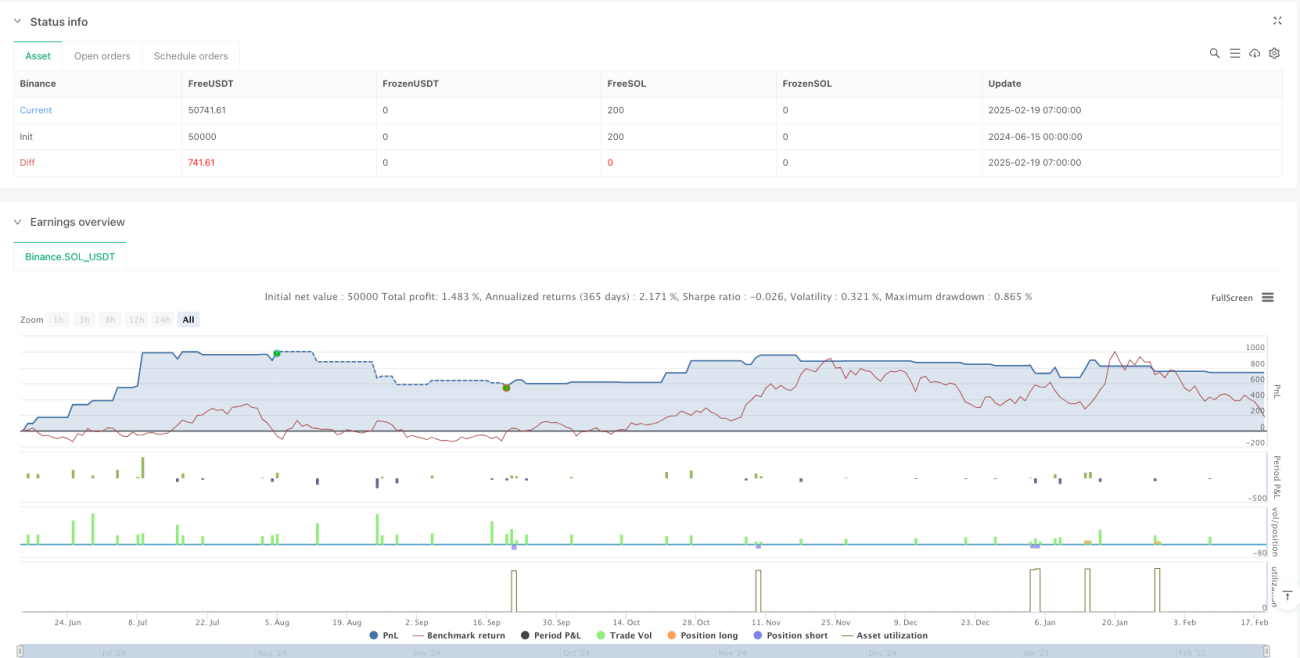

/*backtest

start: 2024-06-15 00:00:00

end: 2025-02-19 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("RSI + Stochastic RSI Strategy", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// INPUTS- 1