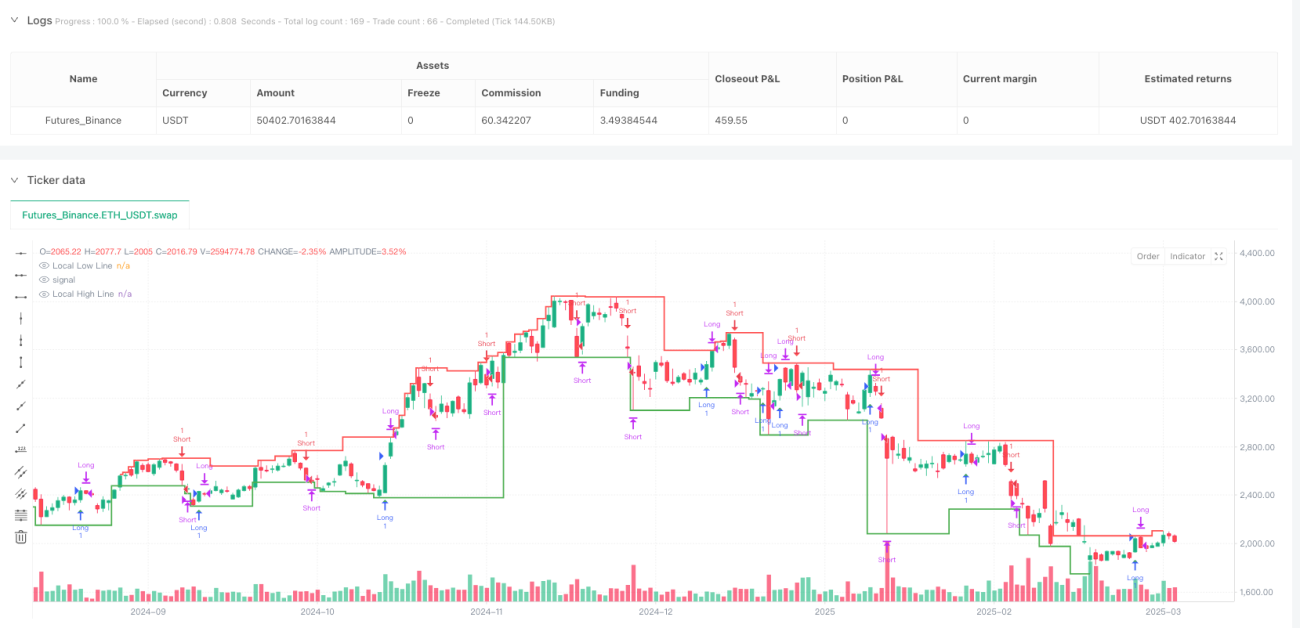

Обзор

Это инновационная торговая стратегия, сочетающая анализ зон ликвидности и внутреннюю динамику рыночной структуры, направленная на выявление точек входа с высокой вероятностью успеха. Стратегия отслеживает взаимодействие цены с ключевыми рыночными уровнями и использует смену внутренней структуры рынка для инициирования сделок, предоставляя трейдеру гибкий и точный метод входа в рынок.

Принцип стратегии

Основная логика стратегии базируется на двух ключевых компонентах: идентификации зон ликвидности и смене внутренней структуры рынка. Зоны ликвидности определяются динамически на основе анализа локальных максимумов и минимумов, а смена внутренней структуры рынка оценивается по пробою ценой предыдущих бычьих или медвежьих уровней, указывая на изменение направления рынка.

Стратегия обладает следующими ключевыми особенностями:

- Логика смены внутренней структуры: не зависит от традиционных свечных паттернов, а основана на пробое ключевых уровней ценой.

- Отслеживание зон ликвидности: динамическое определение ключевых зон ликвидности, предотвращающее торговлю в условиях слабого рынка.

- Гибкость режимов: предлагает три режима торговли: «Both», «Bullish Only» и «Bearish Only».

- Управление рисками: возможность настройки уровней стоп-лосса и тейк-профита.

- Контроль временного диапазона: точная настройка временных интервалов для торговли.

Преимущества стратегии

- Динамическая адаптивность: стратегия быстро реагирует на изменения рыночной структуры.

- Точный вход: сочетание зон ликвидности и смены внутренней структуры повышает точность входа.

- Контролируемый риск: встроенные механизмы стоп-лосса и тейк-профита.

- Высокая гибкость: возможность выбора режима торговли в зависимости от рыночных условий.

- Многомерный анализ: одновременный учет ценового действия, ликвидности и рыночной структуры.

Риски стратегии

- Резкие колебания рынка могут привести к срабатыванию стоп-лосса.

- На боковом рынке частые сигналы могут увеличить торговые издержки.

- Неправильная настройка параметров может повлиять на производительность стратегии.

- Результаты бэктестинга могут отличаться от реальной торговли.

Направления оптимизации стратегии

- Внедрение алгоритмов машинного обучения для адаптивной оптимизации параметров.

- Добавление дополнительных фильтров, таких как объем торгов, индикаторы волатильности.

- Разработка механизма подтверждения на нескольких таймфреймах.

- Оптимизация алгоритмов стоп-лосса и тейк-профита с учетом динамической волатильности рынка.

Заключение

Это инновационная торговая стратегия, объединяющая анализ ликвидности и динамику рыночной структуры. Благодаря гибкой логике смены внутренней структуры и точному отслеживанию зон ликвидности, она предоставляет трейдеру мощный торговый инструмент. Ключевым преимуществом стратегии являются её адаптивность и способность к многомерному анализу, что позволяет сохранять высокую эффективность исполнения в различных рыночных условиях.

- 1