Обзор

Данная стратегия представляет собой многомерный метод прогнозирования краткосрочных трендов, ориентированный на использование синергетического эффекта нескольких технических индикаторов для выявления и прогнозирования краткосрочных изменений тренда на финансовых рынках. Стратегия объединяет такие ключевые инструменты технического анализа, как простая скользящая средняя (SMA), индекс относительной силы (RSI), средний направленный индекс (ADX), средний истинный диапазон (ATR), схождение/расхождение скользящих средних (MACD) и стохастический осциллятор (Stochastic), с целью повышения точности и надежности торговых сигналов.

Принцип работы стратегии

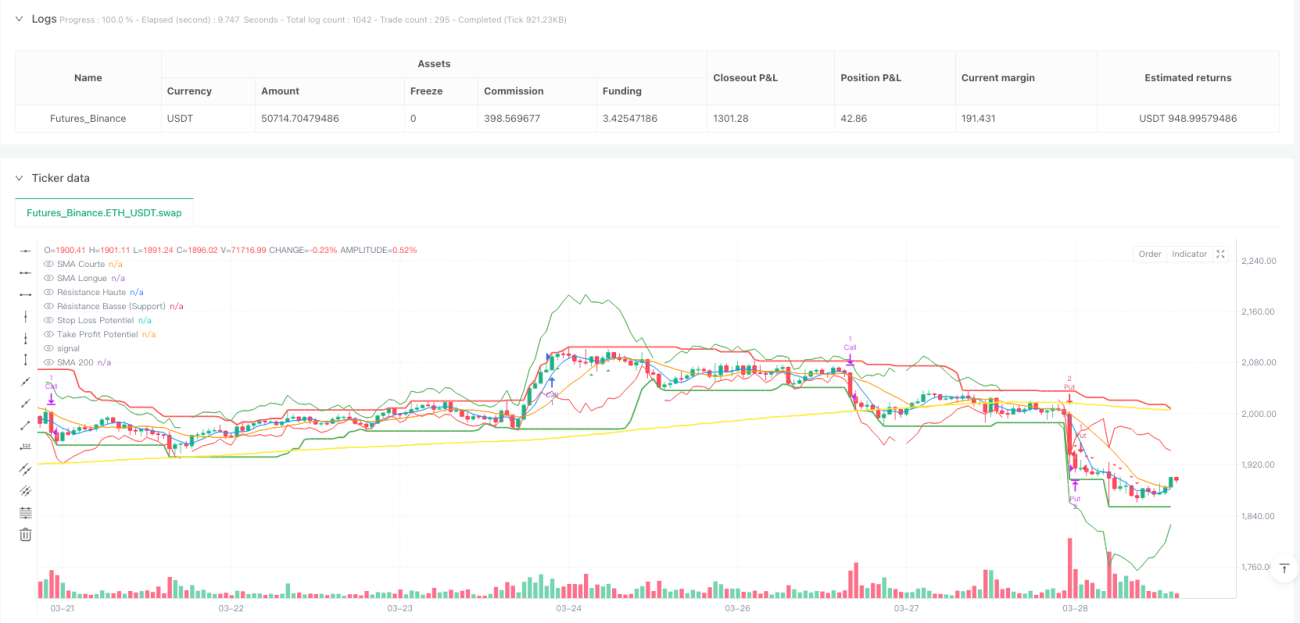

Основной принцип стратегии основан на совместном анализе множества технических индикаторов и механизме подтверждения тренда. Торговые сигналы генерируются с учетом следующих ключевых факторов:

- Пересечение краткосрочной и долгосрочной скользящих средних

- Состояние перекупленности/перепроданности RSI

- Изменения линии MACD и сигнальной линии

- Импульсный индикатор стохастического осциллятора

- Сила тренда по ADX

- Общий рыночный тренд по 200-периодной скользящей средней

- Недавняя волатильность рынка

Стратегия динамически рассчитывает потенциальные точки входа, стоп-лоссы и тейк-профиты, корректируя эти ключевые параметры в соответствии с последней рыночной волатильностью, тем самым реализуя управление рисками и исполнение сделок.

Преимущества стратегии

- Комплексный анализ множества индикаторов: объединение нескольких технических индикаторов снижает риск ложных сигналов от одного индикатора

- Динамическое управление рисками: механизм стоп-лосса и тейк-профита на основе ATR позволяет адаптировать позиции к рыночной волатильности

- Гибкие временные рамки: поддержка различных торговых периодов от 5 минут до 4 часов

- Адаптивный размер позиции: динамическое изменение размера позиции в зависимости от доступного капитала и процента риска на сделку

- Подтверждение силы тренда: использование ADX для подтверждения эффективности тренда, что позволяет избегать частых сделок в боковом рынке

Риски стратегии

- Сложность множества индикаторов может привести к задержке в генерации сигналов

- В условиях высокой нестабильности рынка индикаторы могут давать противоречивые сигналы

- Результаты бэктестинга могут не полностью отражать фактическую торговлю в будущем

- Использование кредитного плеча может значительно увеличить убытки

- Не учитываются фундаментальные факторы и внезапные рыночные события

Направления оптимизации стратегии

- Внедрение алгоритмов машинного обучения для динамической настройки весов индикаторов

- Добавление большего количества фундаментальных и сентиментных индикаторов

- Разработка более умных алгоритмов управления позициями

- Настройка параметров под различные рынки и типы активов

- Интеграция анализа новостей в реальном времени и настроений в социальных сетях

Заключение

Это многомерная, основанная на данных стратегия прогнозирования краткосрочных трендов, которая за счет сложной комбинации технических индикаторов и динамического управления рисками стремится повысить точность и надежность торговых решений. Несмотря на значительные теоретические преимущества, на практике стратегия требует осторожности и постоянного проведения бэктестинга и оптимизации.

- 1