Обзор стратегии

Адаптивная количественная торговая стратегия на основе пересечения скользящих средних с отслеживанием волатильности представляет собой систематический подход, специально разработанный для высокочастотной и краткосрочной торговли. В основе стратегии лежит использование пересечения быстрой скользящей средней (MA) с медленной скользящей средней в качестве основного триггерного сигнала, в сочетании с несколькими ключевыми фильтрами и точными инструментами управления рисками для захвата небольших, но быстрых ценовых движений. Стратегия обладает высокой степенью настраиваемости: пользователь может гибко выбирать тип скользящей средней (EMA, SMA, WMA, HMA, VWMA) и её период, адаптируясь к различным рыночным ритмам. Кроме того, стратегия готова к интеграции с API, что позволяет легко встроить её в автоматизированные торговые системы для быстрого исполнения сигналов, что делает её особенно подходящей для краткосрочных трейдеров, стремящихся к получению высокой частоты небольших прибылей.

Принцип работы стратегии

Логика стратегии состоит из нескольких ключевых частей:

-

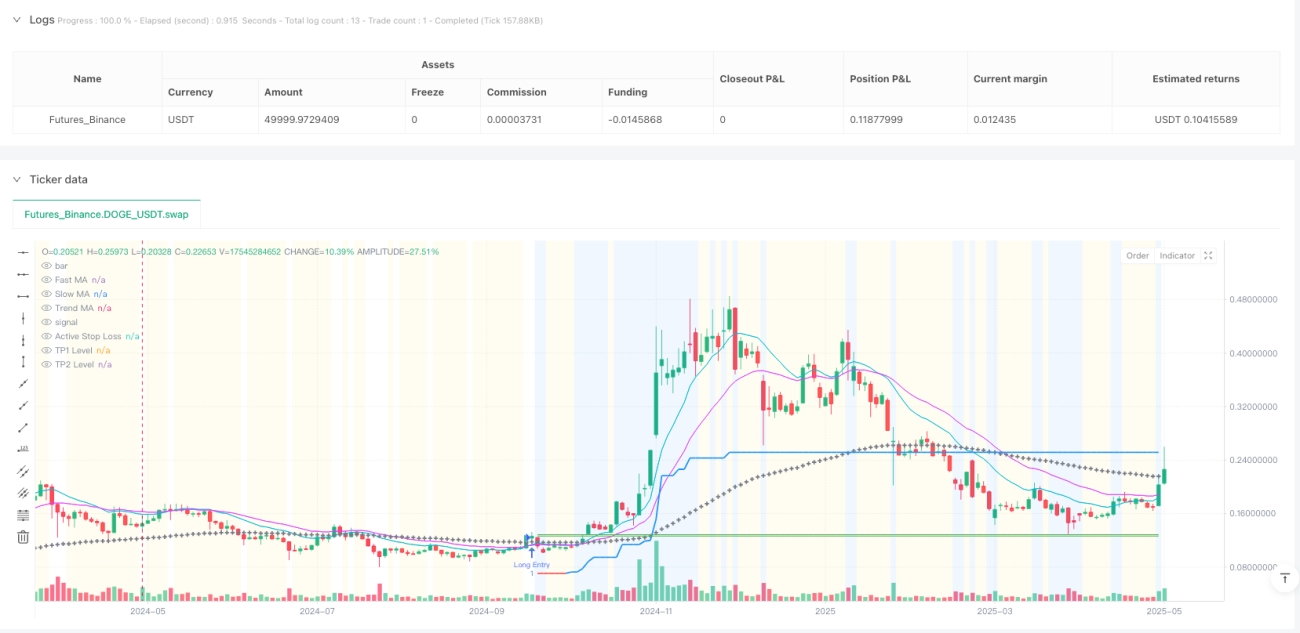

Сигнал на вход: Основным триггером входа служит пересечение быстрой скользящей средней с медленной. Пользователь может гибко настраивать тип скользящей средней (EMA, SMA, WMA, HMA, VWMA) и длину периода для изменения чувствительности сигнала и адаптации к различным рыночным условиям.

-

Трендовый фильтр: Стратегия может опционально использовать долгосрочную скользящую среднюю в качестве фильтра общего тренда, чтобы гарантировать, что сделки открываются только в направлении основного тренда, избегая контртрендовой краткосрочной торговли в сильно направленных рынках.

-

Подтверждающие фильтры:

- ATR-фильтр волатильности: Предназначен для приостановки входа на крайне плоских или «мёртвых» рынках, где волатильность ниже динамического порога (на основе среднего ATR). Это помогает избежать ложных движений в бестрендовых условиях с низкой энергией.

- Фильтр объёма: Проверяет минимальный уровень рыночного участия (сравнение объёма с его скользящей средней) для подтверждения сигнала входа, предотвращая сделки на основе низколиквидных всплесков или несущественного ценового поведения.

-

Комплект управления рисками:

- Начальный стоп-лосс по волатильности: Начальный стоп-лосс на основе ATR обеспечивает объективную отправную точку для определения риска каждой сделки, адаптируясь к недавней волатильности.

- Трейлинг-стоп по ATR: Критически важен для динамических рынков; линия трейлинг-стопа перемещается за благоприятным движением цены, чтобы защитить прибыль успешных краткосрочных сделок, одновременно позволяя относительно быстро сократить убытки при развороте.

- Стоп на уровне безубыточности (опционально): После достижения TP1 или движения цены на определённое расстояние в ATR стоп автоматически перемещается к цене входа (с буфером) для быстрой нейтрализации риска по сделкам, которые уже показали начальный успех.

- Двойные уровни тейк-профита: Установлены две цели TP1 и TP2. TP1 предназначен для быстрого частичного закрытия (например, 50%), а TP2 – для получения большей прибыли от оставшейся позиции.

-

Управление позицией: Используется фиксированный размер позиции, что обеспечивает точный контроль размера каждой сделки. Это критически важно для последовательного применения риска и генерации API-команд в высокочастотной среде.

Преимущества стратегии

При глубоком анализе кода стратегии можно выделить следующие явные преимущества:

-

Высокая степень настраиваемости: Пользователь может гибко регулировать различные параметры, включая тип и период скользящих средних, настройки фильтров и параметры управления рисками, что позволяет адаптировать стратегию к широкому спектру рыночных условий и торговых стилей.

-

Многоуровневый механизм фильтрации: Сочетание фильтров тренда, волатильности и объёма эффективно снижает количество ложных сигналов и рыночного шума, повышая качество сделок.

-

Полноценное управление рисками: Встроенные множественные механизмы стоп-лосса (начальный, трейлинг, безубыточность) и двойные цели тейк-профита обеспечивают детальный контроль рисков и защиту прибыли.

-

Удобство интеграции с API: Четкая и однозначная логика входа и выхода генерирует недвусмысленные сигналы, упрощая интеграцию с внешними торговыми системами для почти мгновенного исполнения ордеров.

-

Точный контроль позиции: Фиксированный размер позиции упрощает нагрузку на конечные точки API, делая автоматическое исполнение более надёжным.

-

Адаптивность: За счёт настройки параметров стратегия может трансформироваться из высокочастотной краткосрочной модели в более долгосрочную модель следования за трендом, адаптируясь к различным рыночным условиям и личным предпочтениям трейдера.

Риски стратегии

Несмотря на продуманный дизайн, стратегия содержит потенциальные риски и вызовы:

-

Риск оптимизации параметров: Из-за множества настраиваемых параметров чрезмерная оптимизация может привести к отличным результатам на исторических данных, но плохой реальной эффективности (переобучение). Инвесторам следует проверять стратегию на данных вне выборки или проводить форвард-тестирование, чтобы избежать этого риска.

-

Влияние торговых издержек: Высокочастотная торговля означает большое количество сделок, поэтому накопленные комиссии и проскальзывания могут существенно повлиять на чистую прибыльность. Перед использованием необходимо точно учитывать эти издержки в настройках и бэктестах.

-

Колебания качества сигналов: В разных рыночных условиях надёжность сигналов пересечения скользящих средних может меняться, особенно на боковых рынках или при высокой волатильности.

-

Технологическая зависимость: Будучи готовой к API, эффективность стратегии частично зависит от скорости исполнения и стабильности технологии. Задержки или сбои системы могут привести к потере возможностей или отклонениям в исполнении.

-

Ограничение по размеру капитала: Фиксированный размер позиции может не подходить для всех размеров счетов: на небольших счетах может возникнуть чрезмерный риск, а на крупных – неполное использование капитала.

Направления оптимизации стратегии

Исходя из конструкции и потенциальных рисков, можно выделить несколько возможных направлений оптимизации:

-

Адаптивные параметры: Сделать ключевые параметры (например, множитель ATR и периоды скользящих средних) самонастраивающимися в зависимости от рыночных условий, чтобы повысить адаптивность стратегии к разным фазам рынка.

-

Улучшенная интеллектуальная фильтрация: Включить дополнительные индикаторы состояния рынка (например, структуру рынка, распознавание паттернов волатильности или корреляцию с родственными активами), чтобы ещё больше повысить точность фильтров.

-

Динамическое управление позицией: Заменить фиксированный размер позиции на динамический расчёт, основанный на размере счёта, текущей волатильности и недавней производительности стратегии, что позволит реализовать более разумное управление капиталом.

-

Подтверждение на нескольких таймфреймах: Проверять сигналы на разных временных интервалах, чтобы убедиться, что направление сделки согласуется с более широкой рыночной структурой, сокращая количество ненужных сделок.

-

Интеграция машинного обучения: Использовать алгоритмы машинного обучения для анализа исторической эффективности сигналов, прогнозирования вероятности успеха будущих сигналов и приоритетного исполнения сделок с высокой вероятностью выигрыша.

-

Управление торговыми сессиями: Добавить фильтр времени торговли, чтобы избегать периодов низкой ликвидности или высокой волатильности, фокусируясь на наиболее эффективных торговых окнах.

-

Фильтр корреляции: Для мультиактивной торговли добавить анализ корреляции с родственными рынками, чтобы избежать избыточной экспозиции к определённым факторам риска.

Заключение

Адаптивная количественная торговая стратегия на основе пересечения скользящих средних с отслеживанием волатильности представляет собой полнофункциональную высокочастотную торговую систему, которая генерирует сигналы на пересечении скользящих средних и дополняет их множеством ключевых фильтров и точных инструментов управления рисками, специально предназначенных для захвата небольших, но быстрых ценовых движений. Сильной стороной стратегии является её высокая степень настраиваемости и полноценная система управления рисками, позволяющая трейдерам тонко настраивать торговые параметры в соответствии с индивидуальной толерантностью к риску и рыночными условиями.

Для высокочастотных трейдеров стратегия предлагает чёткую логику входа и выхода, а также возможность бесшовной интеграции с внешними платформами исполнения, что критически важно для быстрого принятия решений в быстро меняющихся рыночных условиях. Однако при использовании данной стратегии следует уделять особое внимание накоплению торговых издержек и риску чрезмерной оптимизации, чтобы сохранить робастность и прибыльность стратегии в реальной торговле.

В конечном итоге эта стратегия представляет собой сбалансированный подход – она использует возможности технических индикаторов и инструментов управления рисками, сохраняя при этом достаточную гибкость для адаптации к постоянно меняющимся рыночным условиям. При тщательной настройке параметров и постоянном мониторинге и улучшении данная стратегия может стать ценным компонентом количественного торгового портфеля.

- 1