Обзор

Многоцикловая стратегия отслеживания динамической волатильности представляет собой краткосрочную торговую систему, объединяющую пересечение быстрой/медленной экспоненциальной скользящей средней (EMA) с фильтром на основе индекса относительной силы (RSI). Стратегия фокусируется на поиске возможностей для входа в коррекциях внутри доминирующего краткосрочного тренда, снижая количество шумовых сделок с помощью механизма множественного подтверждения. Её ключевые особенности включают контроль риска на основе среднего истинного диапазона (ATR), адаптивный трейлинг-стоп, корректировку стоп-лосса на основе объёма и трехуровневую систему частичного взятия прибыли. Кроме того, стратегия использует проверку RSI на старшем таймфрейме в качестве механизма раннего выхода, чтобы избегать чрезмерного пребывания в неблагоприятном тренде.

Принцип работы стратегии

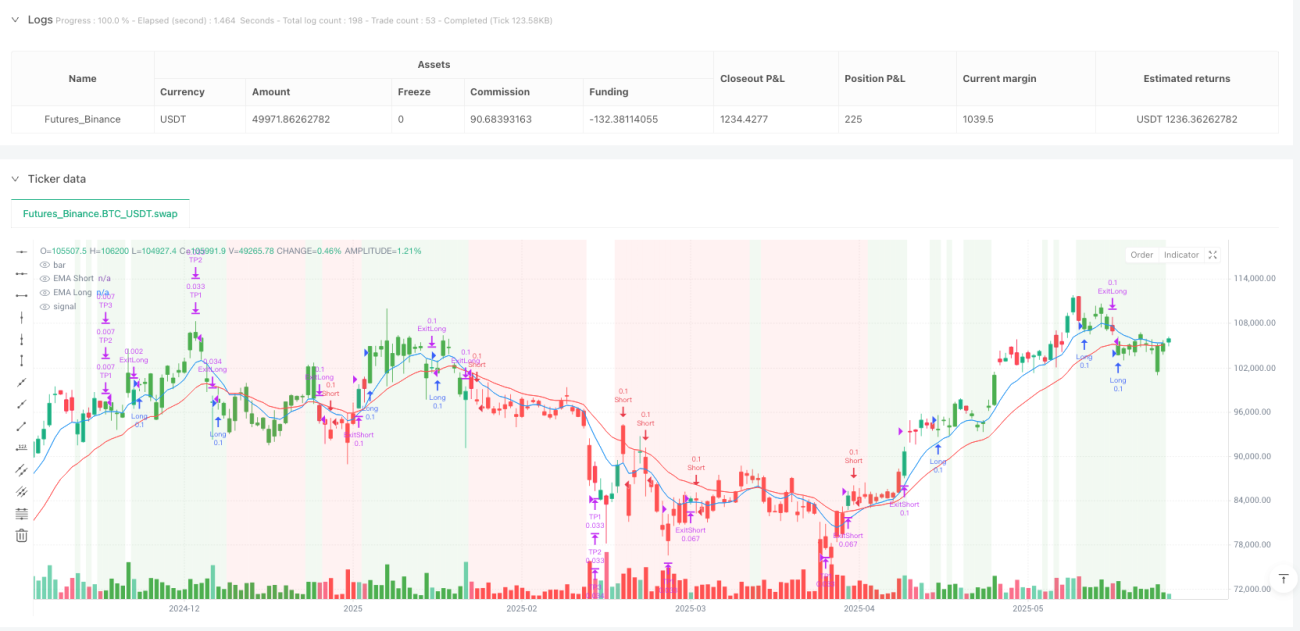

Стратегия работает на основе многоуровневой архитектуры сигналов:

- Определение тренда: Микротренд определяется пересечением быстрой и медленной EMA. Когда быстрая EMA находится выше медленной, тренд считается восходящим; ниже – нисходящим.

- Фильтр здоровья импульса: Предотвращает погоню за перегретым движением. Открытие длинной позиции разрешено только когда RSI ниже уровня перекупленности; короткой – выше уровня перепроданности.

- Механизм подтверждения свечой: Требует, чтобы сигнальные условия выполнялись в течение нескольких последовательных свечей, эффективно отфильтровывая рыночный шум.

- Триггер входа: Рыночный ордер выставляется при появлении свечи, завершающей окно подтверждения.

- Начальный стоп-лосс: Основан на волатильности ATR и динамически корректируется в зависимости от относительного объёма.

- Логика трейлинг-стопа: Комбинация опорных точек и базового стопа на ATR для фиксации прибыли.

- Мониторинг RSI старшего таймфрейма: Предоставляет сигнал выхода на основе рыночного контекста, предотвращая торговлю против тренда.

- Уровневые цели по прибыли: Установка трёх целей на основе ATR для постепенного сокращения позиции.

- Ограничитель сделок: Лимит максимального числа сделок в рамках одного этапа тренда для предотвращения избыточной торговли.

Ключевое новшество стратегии – органичное объединение множества технических индикаторов с поведенческими показателями рынка (объём, волатильность), что создаёт адаптивную торговую систему, автоматически подстраивающую параметры под различные рыночные условия.

Преимущества стратегии

- Высокая адаптивность: Стопы и цели, регулируемые ATR, позволяют стратегии подстраиваться под разные уровни волатильности без частой перенастройки параметров.

- Многоуровневое управление риском: Комбинация начального стопа, трейлинг-стопа, частичной фиксации прибыли и фильтра RSI на нескольких таймфреймах образует полную систему контроля рисков.

- Фильтрация шума: Требование подтверждения несколькими последовательными свечами сокращает количество ложных сигналов, повышая качество сделок.

- Чувствительность к ликвидности: Уровень стопа корректируется с помощью коэффициента объёма, автоматически ужесточая риск в условиях низкой ликвидности.

- Мониторинг зрелости тренда: По мере развития тренда автоматически уменьшается количество разрешённых сделок, чтобы избежать избыточной торговли в конце движения.

- Гибкий механизм фиксации прибыли: Трехуровневая система частичного взятия прибыли позволяет зафиксировать часть прибыли при благоприятном движении, сохраняя потенциал дальнейшего роста.

- Межцикловой анализ: Мониторинг RSI на старшем таймфрейме даёт более широкий взгляд на рыночный контекст, предотвращая зацикленность на микросигналах при крупном развороте тренда.

- Удобство исполнения: Интеграция через PineConnector позволяет легко автоматизировать стратегию, снижая человеческий фактор и эмоциональное влияние.

Риски стратегии

- Риск просадки: Несмотря на многоуровневый контроль, в экстремальных рыночных условиях (гэпы, флэш-крэши) стратегия может столкнуться с просадкой выше ожидаемой. Метод смягчения: уменьшение размера позиции или увеличение множителя ATR.

- Чувствительность к параметрам: Некоторые ключевые параметры, такие как длины EMA и пороги RSI, существенно влияют на производительность. Чрезмерная оптимизация может привести к переобучению. Рекомендуется пошаговое форвардное тестирование, а не оптимизация на исторических данных.

- Высокие транзакционные издержки: Как краткосрочная стратегия, она имеет повышенную частоту сделок, поэтому накопленные затраты (спред, комиссия) могут значительно повлиять на реальную доходность. В бэктестах следует учитывать реальные торговые издержки.

- Риск задержки: Задержка исполнения PineConnector (около 100–300 мс) в условиях высокой волатильности может увеличить проскальзывание. Не рекомендуется использовать на рынках с крайне высокой волатильностью или низкой ликвидностью.

- Перерисовка опорных точек: На сверхкраткосрочных графиках (ниже минутного) опорные точки могут перерисовываться в процессе формирования текущей свечи, что влияет на точность стопа.

- Запаздывание идентификации тренда: Определение тренда на основе пересечения EMA имеет внутреннее запаздывание, что может привести к пропуску части движения на ранней стадии.

- Риск чрезмерного плеча: Если установлен слишком большой множитель размера позиции, это может привести к чрезмерному риску в одной сделке и быстрому истощению капитала.

Направления оптимизации стратегии

- Оптимизация машинного обучения: Внедрение алгоритмов машинного обучения для динамической настройки параметров EMA и RSI в зависимости от рыночных условий. Это решит проблему недостаточной адаптивности фиксированных параметров на разных фазах рынка.

- Классификация рыночных состояний: Добавление кластерного анализа волатильности для разделения рынка на состояния высокой, средней и низкой волатильности с использованием различных торговых параметров. Это повысит адаптивность на переходных рынках.

- Механизм консенсуса множества индикаторов: Интеграция других индикаторов импульса и тренда (MACD, полосы Боллинджера, KDJ) для формирования системы консенсуса; сигнал генерируется только при согласованном мнении большинства. Это снизит количество ложных сигналов.

- Умный временной фильтр: Добавление анализа торговых сессий и моделей волатильности, чтобы избегать неэффективных периодов и известных событий с высокой волатильностью (публикации важных экономических данных).

- Динамические пропорции частичного взятия прибыли: Автоматическая корректировка процента частичного взятия прибыли и расстояния до целей в зависимости от текущей волатильности и силы тренда – больше позиции сохраняется в сильном тренде, более агрессивная фиксация в слабом.

- Усиление контроля просадок: Внедрение адаптивного механизма на основе исторических паттернов просадок – при обнаружении предвестников крупной просадки, схожей с исторической, автоматически снижается частота сделок или увеличивается расстояние стопа.

- Использование тиковых данных: При возможности интеграция данных на уровне тиков для улучшения цены входа и снижения проскальзывания.

- Межрыночный корреляционный анализ: Добавление анализа корреляции со смежными рынками для использования соотношений лидер-опаздывающий для усиления качества сигналов.

Заключение

Многоцикловая стратегия отслеживания динамической волатильности – это краткосрочная торговая система, объединяющая классические инструменты технического анализа с современными методами количественного управления рисками. Благодаря многоуровневой архитектуре сигналов, сочетающей идентификацию тренда с помощью EMA, импульсный фильтр RSI, подтверждение последовательными свечами, регулировку ATR и мультицикловой анализ, она формирует всестороннюю систему принятия решений. Наиболее заметная особенность – её адаптивность: способность автоматически корректировать торговые параметры и меры контроля рисков в зависимости от волатильности, объёма и зрелости тренда.

Несмотря на некоторые внутренние риски, такие как чувствительность к параметрам, высокие транзакционные издержки и задержки, их можно эффективно контролировать с помощью разумного управления капиталом и постоянной оптимизации. Будущие направления оптимизации сосредоточены на машинном обучении для подбора параметров, классификации рыночных состояний, механизме консенсуса нескольких индикаторов и динамическом управлении рисками.

Для трейдеров, стремящихся ловить коррекционные движения внутри краткосрочных трендов, данная стратегия предоставляет структурированный фреймворк, балансирующий между возможностями входа и контролем риска. Однако, как и для любой торговой системы, перед реальным применением рекомендуется тщательное тестирование на демо-счете и корректировка параметров в соответствии с толерантностью к риску и размером капитала.

- 1