Стратегия ступенчатого усреднения тренда: как элегантно «лечь» при боковом рынке?

Почему традиционные стратегии следования за трендом часто «терпят крах» на боковике?

Будучи практикующим количественным трейдером, я часто слышу вопрос: почему стратегии, отлично работающие на трендовых рынках, начинают сильно проседать, как только рынок переходит в боковик?

Ответ на самом деле прост: большинство трендовых стратегий страдают «трендовым неврозом» — они постоянно пытаются совершать частые сделки в любых рыночных условиях, игнорируя простой факт: 70% времени рынок находится в боковом движении.

Анализируемая сегодня стратегия «Лестничное усреднение тренда» предлагает интересное решение этой проблемы: активно следовать за трендом на трендовом рынке и «изящно отдыхать» на боковике.

Что такое «лестничное усреднение»? Как эта концепция переосмысливает следование за трендом?

У традиционных стратегий на скользящих средних есть фатальный недостаток: они постоянно меняются. Независимо от того, сильный тренд или боковик, средняя линия постоянно подстраивается под колебания цены, что порождает множество ложных сигналов.

Ключевая идея «лестничного усреднения»: «заморозить» скользящую среднюю при определённых условиях.

Конкретная логика реализации:

-

Определение состояния тренда: оценка силы тренда с помощью индикатора ADX

- ADX > 25: сильный тренд

- Наклон MA < 0.3%: боковик

-

Динамическое переключение скользящей средней:

- При сильном тренде: нормальное отслеживание EMA(21)

- При боковике: скользящая средняя «замораживается» на горизонтальном уровне, образуя поддержку/сопротивление

Гениальность этого подхода в том, что стратегия проявляет разный «характер» в разных рыночных условиях — чувствительна на тренде, стабильна в боковике.

Как реализовать систему «захвата тренда»?

Помимо базового механизма лестничного усреднения, стратегия включает модуль «захват тренда», который я считаю наиболее инновационным:

Механизм быстрого разворота:

- При появлении противоположного сильного тренда сразу после закрытия позиции

- Быстрое открытие новой позиции в течение 3 периодов

- Условия: ADX > 30 и разница между DI+ и DI- > 10

Этот механизм решает важную проблему традиционных стратегий: как быстро изменить позицию при развороте тренда.

Представьте сценарий: вы только что закрыли длинную позицию по стоп-лоссу, и рынок сразу начинает сильное нисходящее движение. Традиционные стратегии ждали бы нового подтверждения сигнала, но эта система «захвата тренда» может быстро открыть короткую позицию в течение 3 периодов.

Управление рисками: зачем различать состояния рынка?

Наиболее поучительная особенность данной стратегии — дифференцированный механизм управления рисками:

Контроль рисков на боковике:

- Стоп-лосс переносится ближе к лестничной средней

- Уменьшение множителя ATR, ужесточение стопа

- Более консервативные цели

Контроль рисков на тренде:

- Стандартный множитель ATR для стопа

- Лестничный трейлинг-стоп

- Допуск большего ценового диапазона

Такая структура отражает важную торговую философию: разные рыночные условия требуют разной склонности к риску. На боковике нужно быть осторожнее, на тренде — давать прибыли больше места.

Лестничный трейлинг-стоп: как сбалансировать защиту прибыли и следование за трендом?

Традиционные трейлинг-стопы часто слишком механистичны: либо слишком жёсткие, вызывая преждевременный выход, либо слишком свободные, не защищая прибыль. Лестничный трейлинг-стоп данной стратегии предлагает более разумное решение:

Логика настройки ступеней:

- Динамический расчёт шага на основе ATR

- Максимум 5 уровней ступеней

- При пробитии каждой ступени стоп-лосс поднимается соответственно

Преимущество этой конструкции: она позволяет защитить прибыль, одновременно давая тренду достаточно пространства для развития.

Что следует учитывать при практическом применении?

Исходя из моего опыта реальной торговли, при использовании таких стратегий нужно обратить внимание на следующее:

-

Ловушка оптимизации параметров: не переоптимизируйте порог ADX; значения от 25 до 30 стабильно работают на большинстве рынков.

-

Адаптация к рынку: стратегия лучше подходит для рынков с умеренной волатильностью; при экстремальной волатильности может потребоваться корректировка множителя ATR.

-

Управление капиталом: рекомендуется не превышать 10% капитала на одну сделку, особенно при включении функции захвата тренда.

-

Ловушки бэктеста: особое внимание уделяйте проскальзыванию и комиссиям, особенно при частых сделках на боковике.

В чём инновационная ценность этой стратегии?

С точки зрения развития количественных стратегий, эта стратегия представляет важное направление эволюции: переход от единой логики к многорежимной адаптации.

Традиционные стратегии пытаются применять фиксированную логику ко всем рыночным ситуациям, а эта стратегия демонстрирует мудрость «действуй по обстоятельствам»:

- На трендовом рынке она ведёт себя как агрессивный последователь тренда

- На боковике — как консервативный диапазонный трейдер

Такой подход даёт разработчикам стратегий важный урок: стратегия должна обладать способностью «чувствовать рынок», а не слепо выполнять фиксированную логику.

Наконец, важно подчеркнуть, что ни одна стратегия не является универсальной. Эта лестничная стратегия усреднения, хотя и элегантна теоретически, на практике требует корректировки с учётом конкретной рыночной среды и личной толерантности к риску. Помните: лучшая стратегия — та, которая подходит именно вам.

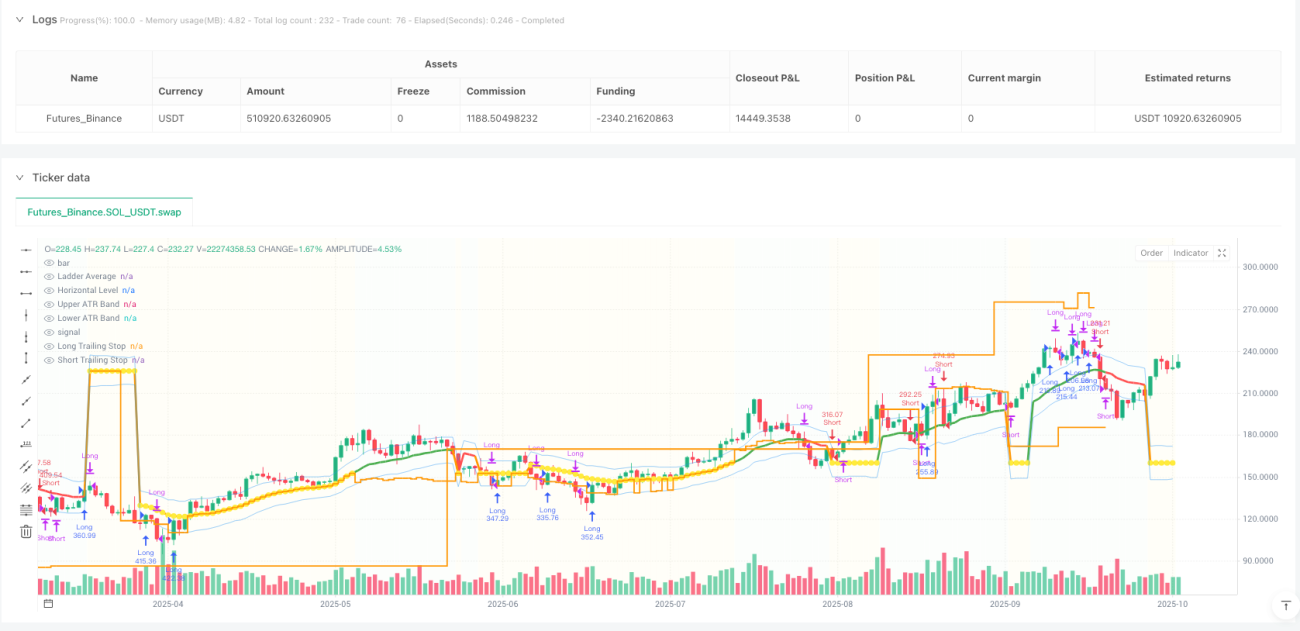

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1