رجحان کی پیروی کے چار عناصر کی حکمت عملی

خلاصہ

یہ حکمت عملی SAR اشارے، RSI اشارے، VOL اشارے اور MA متحرک اوسط کے چار عناصر کو استعمال کرتے ہوئے رجحان کی شناخت کرتی ہے اور مضبوط رسک مینجمنٹ کے اقدامات کے ساتھ رجحان کی پیروی کرکے منافع کماتی ہے۔ حکمت عملی میں SAR اشارے کو مرکزی حیثیت حاصل ہے، جس کے ساتھ RSI کے زیادہ خرید/زیادہ فروخت کی حدوں کے ذریعے الٹنے کے سگنلز کی شناخت کی جاتی ہے، VOL اشارے سے حجم کی خصوصیات کا تعین کیا جاتا ہے، اور MA متحرک اوسط سے اہم اور ذیلی رجحان کی سمت کا فیصلہ کیا جاتا ہے۔ مختلف اشاروں کے امتزاج سے جھوٹے سگنلز کو فلٹر کیا جا سکتا ہے اور حقیقی رجحان کی سمت کی نشاندہی کی جا سکتی ہے۔ رسک مینجمنٹ میں سٹاپ لاس اور ٹیک پروفٹ کا تعین کیا گیا ہے، جو ایک تجارت میں ہونے والے نقصان اور مجموعی منافع کو مؤثر طریقے سے کنٹرول کرتا ہے۔ یہ حکمت عملی درمیانی سے طویل مدتی سرمایہ کاروں کے لیے موزوں ہے اور مرکزی رجحان کے مطابق مستحکم منافع فراہم کر سکتی ہے۔

حکمت عملی کا اصول

اس حکمت عملی میں چار اہم تکنیکی اشارے استعمال کیے گئے ہیں:

-

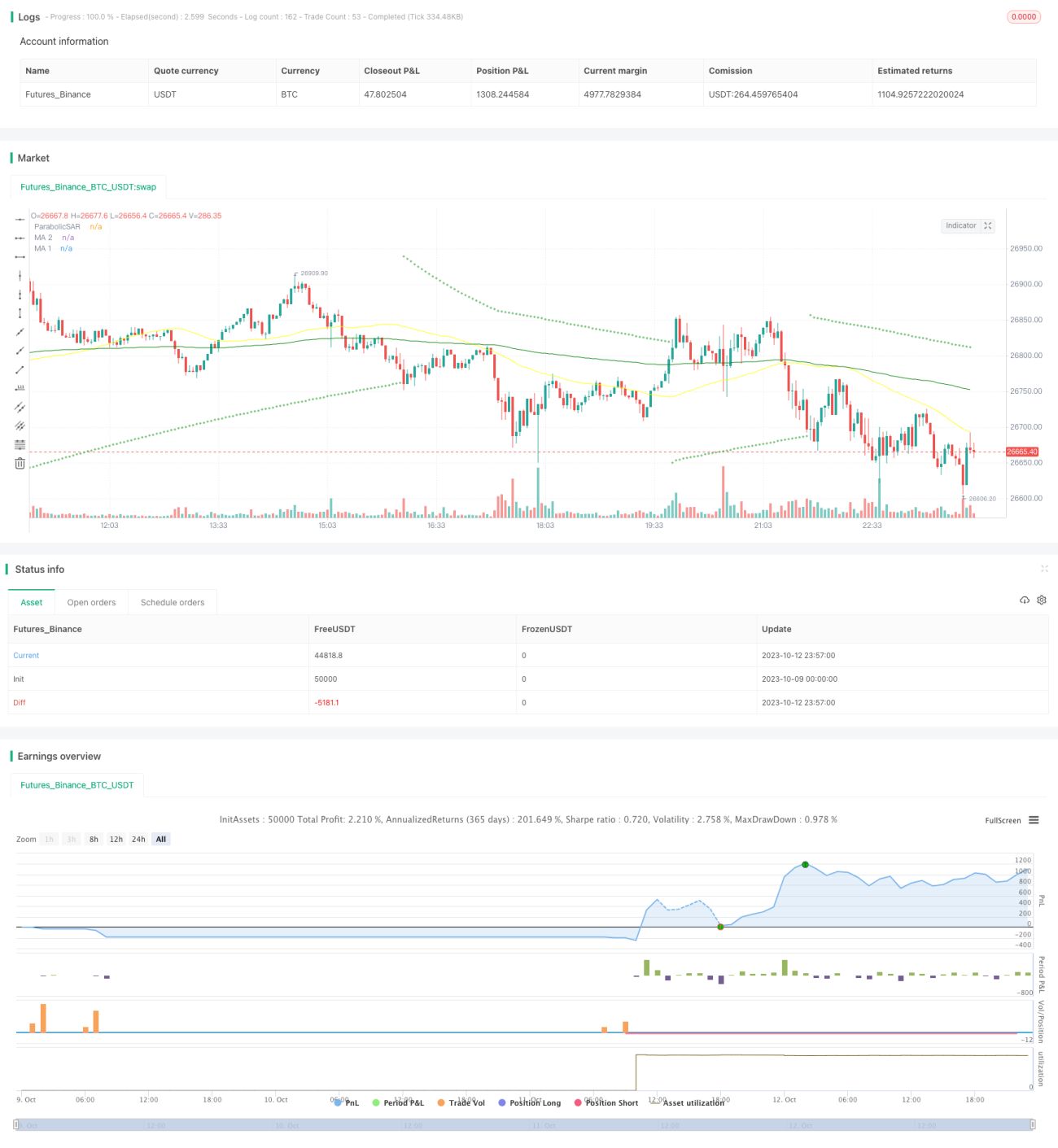

Parabolic SAR: یہ اشارہ نقطوں اور رجحان کے درمیان تعلق کا استعمال کرتے ہوئے رجحان کی سمت اور الٹنے کے مقام کا تعین کرتا ہے۔ جب نقطہ قیمت کے اوپر ہو تو یہ تیزی (bullish) کی علامت ہے، اور جب نقطہ قیمت کے نیچے ہو تو یہ مندی (bearish) کی علامت ہے۔ جب نقطہ قیمت کو عبور کرے تو یہ رجحان کے الٹنے کی نشاندہی کرتا ہے۔ حکمت عملی SAR کو مرکزی اشارے کے طور پر استعمال کرتی ہے تاکہ رجحان کی سمت کا تعین کیا جا سکے۔

-

RSI: نسبتاً طاقت کا اشارہ (Relative Strength Index)۔ یہ اشارہ 0-100 کے درمیان اتار چڑھاؤ کے ذریعے مارکیٹ میں زیادہ خرید/زیادہ فروخت کی صورت حال کا تعین کرتا ہے۔ RSI 70 سے اوپر زیادہ خرید کا علاقہ، 30 سے نیچے زیادہ فروخت کا علاقہ، اور 50 کے قریب درمیانی خطہ سمجھا جاتا ہے۔ حکمت عملی RSI کا استعمال زیادہ خرید/زیادہ فروخت کے الٹنے کے سگنلز کی شناخت کے لیے کرتی ہے۔

-

VOL: حجم کا اشارہ (Volume)۔ حکمت عملی VOL کا استعمال حجم میں اضافے کی خصوصیات کو جانچنے کے لیے کرتی ہے تاکہ رجحان کی تصدیق کی جا سکے اور الٹنے کے سگنلز کے معیار کا اندازہ لگایا جا سکے۔

-

MA: متحرک اوسط (Moving Average)۔ حکمت عملی مختصر اور طویل اوسط کا استعمال کرتی ہے تاکہ اہم اور ذیلی رجحان کی سمت کا تعین کیا جا سکے۔ جب مختصر اوسط طویل اوسط کو نیچے سے اوپر کرتی ہے تو یہ تیزی کا سگنل ہے، اور جب مختصر اوسط طویل اوسط کو اوپر سے نیچے کرتی ہے تو یہ مندی کا سگنل ہے۔

ٹریڈنگ سگنلز کی تخلیق کے قواعد:

طویل (Long) شرائط: SAR نقطہ کینڈل کے نیچے منتقل ہو جائے، RSI نیچے سے اوپر اٹھ کر درمیانی خطے میں داخل ہو، VOL میں واضح اضافہ ہو، اور مختصر متحرک اوسط نیچے سے اوپر طویل متحرک اوسط کو عبور کرے۔

مختصر (Short) شرائط: SAR نقطہ کینڈل کے اوپر منتقل ہو جائے، RSI اوپر سے نیچے آ کر درمیانی خطے میں داخل ہو، VOL میں واضح اضافہ ہو، اور مختصر متحرک اوسط اوپر سے نیچے طویل متحرک اوسط کو عبور کرے۔

اس حکمت عملی میں ٹیک پروفٹ اور سٹاپ لاس کے رسک مینجمنٹ کے قواعد بھی شامل ہیں۔ ٹیک پروفٹ کا ہدف داخلے کی قیمت کا 2 گنا ہے، جبکہ سٹاپ لاس کی قیمت داخلے کی قیمت کا 0.8 گنا ہے، جو منافع کو محفوظ کرنے اور خطرے کو کنٹرول کرنے میں مؤثر ثابت ہوتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- متعدد اشاروں کا امتزاج جھوٹے سگنلز سے بچاتا ہے اور حقیقی رجحان کی تبدیلی کو پکڑتا ہے۔

- رسک مینجمنٹ میں سٹاپ لاس اور ٹیک پروفٹ کی موجودگی خطرے پر مؤثر کنٹرول فراہم کرتی ہے۔

- پوزیشن مینجمنٹ میں مرحلہ وار داخلہ اور مرحلہ وار ٹیک پروفٹ سے منافع کو زیادہ سے زیادہ کیا جا سکتا ہے۔

- پیرامیٹرز کو بار بار بہتر اور جانچا گیا ہے، جس سے پیرامیٹرز کی مضبوطی کو یقینی بنایا گیا ہے۔

- تاریخی ڈیٹا کی کافی مقدار موجود ہے، جو حقیقی تجارتی ماحول کی نقل کرتی ہے۔

- آپریشن کی منطق واضح اور سادہ ہے، جسے سمجھنا اور نافذ کرنا آسان ہے۔

خطرے کا تجزیہ

اس حکمت عملی میں درج ذیل خطرات بھی موجود ہیں:

- مارکیٹ میں غیر معمولی اتار چڑھاؤ کی وجہ سے سٹاپ لاس ٹوٹ سکتا ہے۔ سٹاپ لاس کے فاصلے کو مناسب حد تک بڑھانے کی سفارش کی جاتی ہے۔

- تجارتی مصنوعات میں لیکویڈیٹی کی کمی کی وجہ سے سٹاپ لاس نہ لگ سکے۔ ایسی مصنوعات کا انتخاب کریں جن میں لیکویڈیٹی زیادہ ہو۔

- نظامی خطرہ (systemic risk) کی وجہ سے قیمت میں غیر معمولی گیپ ہو سکتا ہے۔ لیوریج کم کریں اور بنیادی طور پر مضبوط اثاثوں میں سرمایہ کاری کریں۔

- پیرامیٹرز کی زیادہ بہتری (overfitting) کی وجہ سے منحنی خطوط بہت خوبصورت ہو سکتے ہیں۔ پیرامیٹرز کو کمزور کر کے مضبوطی بہتر بنائی جا سکتی ہے۔

- زیادہ تعدد پر تجارت کرنے سے سلپیج (slippage) کے اخراجات بڑھ سکتے ہیں۔ سگنلز کے درمیان وقفہ بڑھایا جا سکتا ہے۔

- سگنلز کی کارکردگی کمزور ہونے پر انہیں اپ ڈیٹ کرنے کی ضرورت ہے۔ باقاعدہ بیک ٹیسٹ اور پیرامیٹرز کی بہتری ضروری ہے۔

بہتری کے راستے

اس حکمت عملی کو درج ذیل پہلوؤں سے مزید بہتر بنایا جا سکتا ہے:

- مختلف اشاروں کے امتزاج جیسے MACD، KD وغیرہ کو جانچ کر بہتر مماثلت تلاش کریں۔

- MA کی مدت کے پیرامیٹرز کو بہتر بنائیں تاکہ اہم اور ذیلی رجحان کی واضح شناخت ہو سکے۔

- ٹیک پروفٹ اور سٹاپ لاس کے تناسب کو بہتر بنائیں تاکہ بہترین رسک ریوارڈ تناسب حاصل ہو۔

- مختلف مصنوعات کے لیے پیرامیٹرز کی مضبوطی کو جانچیں اور بہترین مجموعہ تلاش کریں۔

- مشین لرننگ ماڈلز کا اضافہ کریں تاکہ تجارتی سگنلز کی تشخیص میں مدد ملے۔

- ایڈاپٹیو سٹاپ لاس الگورتھم شامل کریں تاکہ سٹاپ لاس حقیقی اتار چڑھاؤ کے قریب ہو۔

- طویل مدت کے پیرامیٹرز کی جانچ کریں اور ٹیک پروفٹ کی حد کو بڑھائیں۔

خلاصہ

یہ حکمت عملی متعدد اشاروں کا استعمال کرتے ہوئے جھوٹے سگنلز کو فلٹر کرتی ہے، رجحان کی سمت کا تعین کرتی ہے، اور سٹاپ لاس اور ٹیک پروفٹ کے ذریعے خطرے کو کنٹرول کرتی ہے۔ پیرامیٹرز کی بہتری اور امتزاج میں تبدیلی کے ذریعے حکمت عملی کی کارکردگی کو مسلسل بہتر بنایا جا سکتا ہے۔ اگرچہ کوئی بھی حکمت عملی مستقبل کی پیش گوئی کرنے میں کامل نہیں ہے، لیکن ایک منظم تجارتی منصوبہ اور بہترین رسک مینجمنٹ منافع کے امکانات کو بہت زیادہ بڑھا سکتا ہے۔ یہ حکمت عملی ایک نسبتاً مضبوط رجحان کی پیروی کا طریقہ فراہم کرتی ہے، جو طویل مدتی مستحکم منافع کے خواہاں عقلی سرمایہ کاروں کے لیے موزوں ہے۔

- 1