ٹریکنگ بریک آؤٹ حکمت عملی

خلاصہ

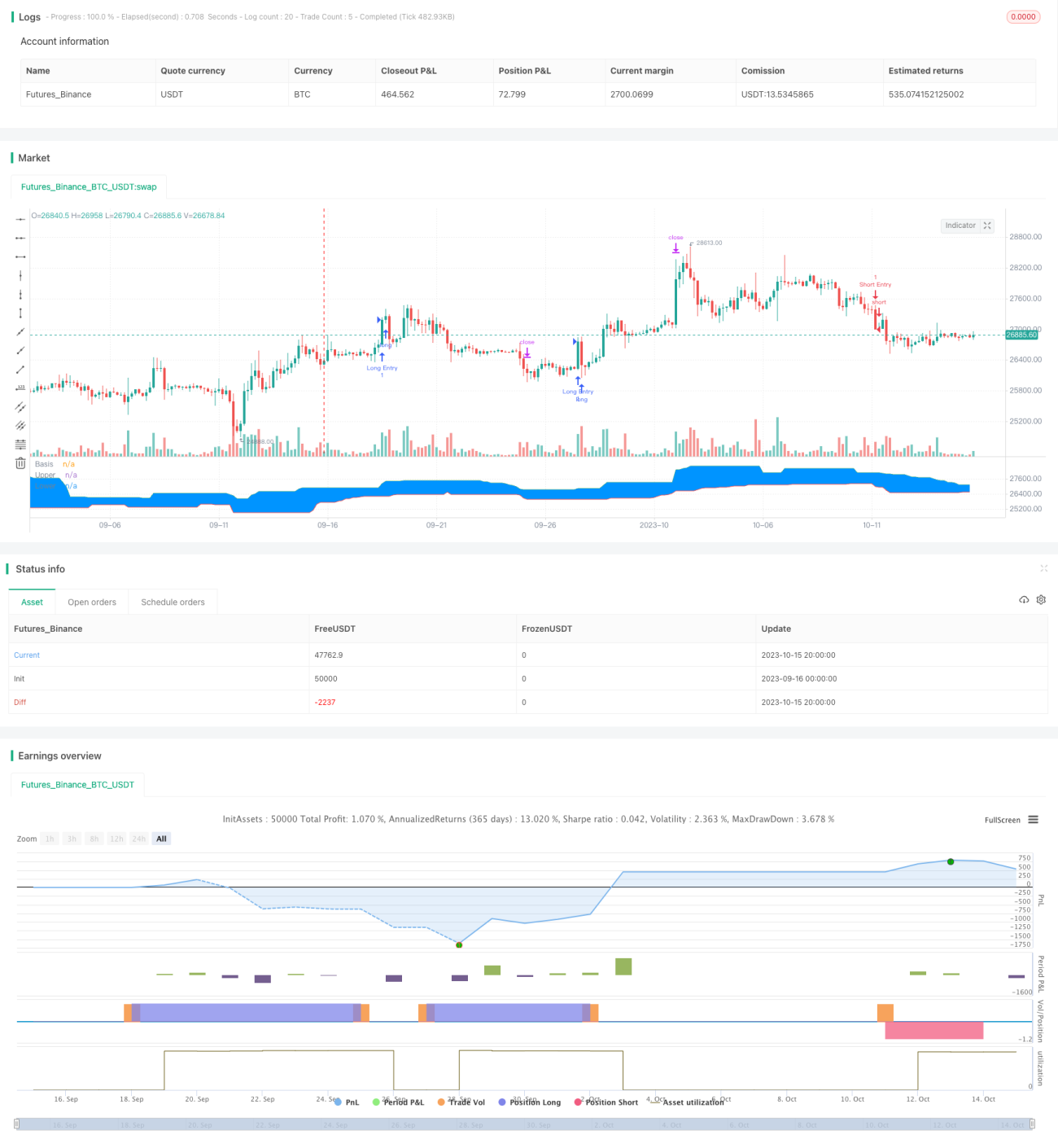

یہ حکمت عملی بنیادی طور پر "ڈونچین چینل" انڈیکیٹر کے ذریعے ایک فالو اپ بریک آؤٹ ٹریڈنگ حکمت عملی کو نافذ کرتی ہے۔ یہ حکمت عملی رجحان اور بریک آؤٹ دونوں تجارتی خیالات کو یکجا کرتی ہے، طویل مدتی رجحان کے تعین کی بنیاد پر، مختصر مدت کے بریک آؤٹ پوائنٹس تلاش کرکے اندراجات کرتی ہے، اور رجحان والی مارکیٹ میں ہم آہنگ تجارت کو ممکن بناتی ہے۔ اس کے علاوہ، حکمت عملی میں سٹاپ لاس اور ٹیک پرافٹ کی سطحیں مقرر کی گئی ہیں تاکہ ہر ٹریڈ کے خطرے اور منافع کے تناسب کو کنٹرول کیا جا سکے۔ مجموعی طور پر، اس حکمت عملی میں رجحان کی پیروی کرنے کا فائدہ ہے، جس سے ہم آہنگ ہو کر طویل مدتی رجحان کے مواقع سے فائدہ اٹھایا جا سکتا ہے۔

حکمت عملی کا اصول

- "ڈونچین چینل" انڈیکیٹر کے پیرامیٹرز سیٹ کریں، ڈیفالٹ مدت 20۔

- EMA سموتھڈ موونگ ایوریج سیٹ کریں، ڈیفالٹ مدت 200۔

- رسک-ریوارڈ ریشو سیٹ کریں، ڈیفالٹ 1.5۔

- بریک آؤٹ واپسی کے پیرامیٹرز سیٹ کریں، بالترتیب لمبی اور چھوٹی پوزیشنوں کے لیے۔

- ریکارڈ کریں کہ پچھلا بریک آؤٹ اونچائی تھا یا نیچی۔

- لمبی سگنل: اگر پچھلا بریک آؤٹ نیچی تھا، اور قیمت ڈونچین چینل کے اوپری بینڈ سے زیادہ اور EMA اوسط سے زیادہ ہے، تو لمبی سگنل پیدا ہوتا ہے۔

- چھوٹی سگنل: اگر پچھلا بریک آؤٹ اونچائی تھا، اور قیمت ڈونچین چینل کے نچلے بینڈ سے کم اور EMA اوسط سے کم ہے، تو چھوٹی سگنل پیدا ہوتا ہے۔

- لمبی پوزیشن میں داخل ہونے کے بعد، سٹاپ لاس ڈونچین چینل کے نچلے بینڈ سے 5 پوائنٹس پیچھے رکھیں، اور ٹیک پرافٹ رسک-ریوارڈ ریشو کو سٹاپ لاس فاصلے سے ضرب دے کر مقرر کریں۔

- چھوٹی پوزیشن میں داخل ہونے کے بعد، سٹاپ لاس ڈونچین چینل کے اوپری بینڈ سے 5 پوائنٹس پیچھے رکھیں، اور ٹیک پرافٹ رسک-ریوارڈ ریشو کو سٹاپ لاس فاصلے سے ضرب دے کر مقرر کریں۔

اس طریقے سے، حکمت عملی رجحان کے تعین اور بریک آؤٹ آپریشن کو یکجا کرتی ہے، ہم آہنگ ہو کر طویل مدتی رجحان میں مختصر مدت کے مواقع کو پکڑ سکتی ہے۔ ایک ہی وقت میں، سٹاپ لاس اور ٹیک پرافٹ کی ترتیب ہر ٹریڈ کے خطرے اور منافع کی صورتحال کو کنٹرول کر سکتی ہے۔

فوائد کا تجزیہ

- طویل مدتی رجحان کی پیروی، ہم آہنگ ہو کر تجارت، مخالف رجحان کی تجارت سے گریز۔

- ڈونچین چینل ایک طویل مدتی انڈیکیٹر کے طور پر، EMA اوسط کے ساتھ مل کر فلٹر کرنے سے رجحان کی سمت کا اچھی طرح تعین کر سکتا ہے۔

- سٹاپ لاس اور ٹیک پرافٹ کا طریقہ کار ہر ٹریڈ کے خطرے کو کنٹرول کرتا ہے، ممکنہ نقصان کو محدود کر سکتا ہے۔

- رسک-ریوارڈ ریشو کی بہتری منافع-نقصان کے تناسب کو بڑھا سکتی ہے، اضافی منافع حاصل کرنے کے لیے۔

- بیک ٹیسٹ کے پیرامیٹرز کی ترتیب لچکدار ہے، مختلف مارکیٹوں کے لیے بہترین پیرامیٹر مجموعہ کو ایڈجسٹ کیا جا سکتا ہے۔

خطرات کا تجزیہ

- ڈونچین چینل اور EMA اوسط فلٹر انڈیکیٹرز کے طور پر غلط سگنل دے سکتے ہیں۔

- بریک آؤٹ تجارت میں پھنسنے کا خطرہ ہوتا ہے، واضح رجحان کے پس منظر کی ضرورت ہوتی ہے۔

- سٹاپ لاس اور ٹیک پرافٹ کے فاصلے طے شدہ ہیں، مارکیٹ کے اتار چڑھاؤ کے مطابق ایڈجسٹ نہیں ہوتے۔

- پیرامیٹرز کی بہتری کی گنجائش محدود ہے، حقیقی مارکیٹ میں کارکردگی کی ضمانت مشکل ہے۔

- تجارتی نظام بہت زیادہ بے ترتیب واقعات کا سامنا نہیں کر سکتا، بلیک سوان کے واقعات بڑے نقصان کا سبب بن سکتے ہیں۔

بہتری کے راستے

- مزید انڈیکیٹرز جیسے اوسیلیٹر شامل کرنے پر غور کیا جا سکتا ہے تاکہ سگنل کے معیار کو بہتر بنایا جا سکے۔

- ذہین سٹاپ لاس اور ٹیک پرافٹ مقرر کیے جا سکتے ہیں جو مارکیٹ کے اتار چڑھاؤ اور ATR انڈیکیٹر کے مطابق متحرک طور پر منافع-نقصان کی پوزیشنوں کو ایڈجسٹ کریں۔

- مشین لرننگ جیسے طریقوں سے پیرامیٹرز کی جانچ اور بہتری کی جا سکتی ہے تاکہ وہ حقیقی مارکیٹ کے قریب ہوں۔

- داخلے کی منطق کو بہتر بنایا جا سکتا ہے، والیوم یا وولیٹیلیٹی انڈیکیٹر کو معاون شرط کے طور پر استعمال کرتے ہوئے جال سے بچا جا سکتا ہے۔

- رجحان کی پیروی کی حکمت عملی یا مشین لرننگ کے ساتھ ملا کر ایک ہائبرڈ حکمت عملی بنانے پر غور کیا جا سکتا ہے تاکہ استحکام بہتر ہو سکے۔

خلاصہ

یہ حکمت عملی ایک فالو اپ بریک آؤٹ حکمت عملی کے طور پر، بنیادی خیال طویل مدتی رجحان کے تعین کے بعد، بریک آؤٹ کو سگنل کے طور پر استعمال کرتے ہوئے ہم آہنگ تجارت کرنا، اور سٹاپ لاس اور ٹیک پرافٹ مقرر کرکے ہر ٹریڈ کے خطرے کو کنٹرول کرنا ہے۔ اس حکمت عملی میں کچھ فوائد ہیں، لیکن بہتری کی گنجائش بھی موجود ہے۔ مجموعی طور پر، اگر پیرامیٹر کی ترتیب، داخلے کے وقت کا انتخاب وغیرہ کو مناسب طریقے سے سنبھالا جائے، اور دیگر تکنیکوں سے تقویت دی جائے، تو یہ حکمت عملی ایک عملی رجحان کی پیروی کرنے والی حکمت عملی بن سکتی ہے۔ لیکن سرمایہ کاروں کو یاد رکھنا چاہیے کہ کوئی بھی تجارتی نظام مارکیٹ کے خطرے کو مکمل طور پر ختم نہیں کر سکتا، اور رسک مینجمنٹ ضروری ہے۔

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1